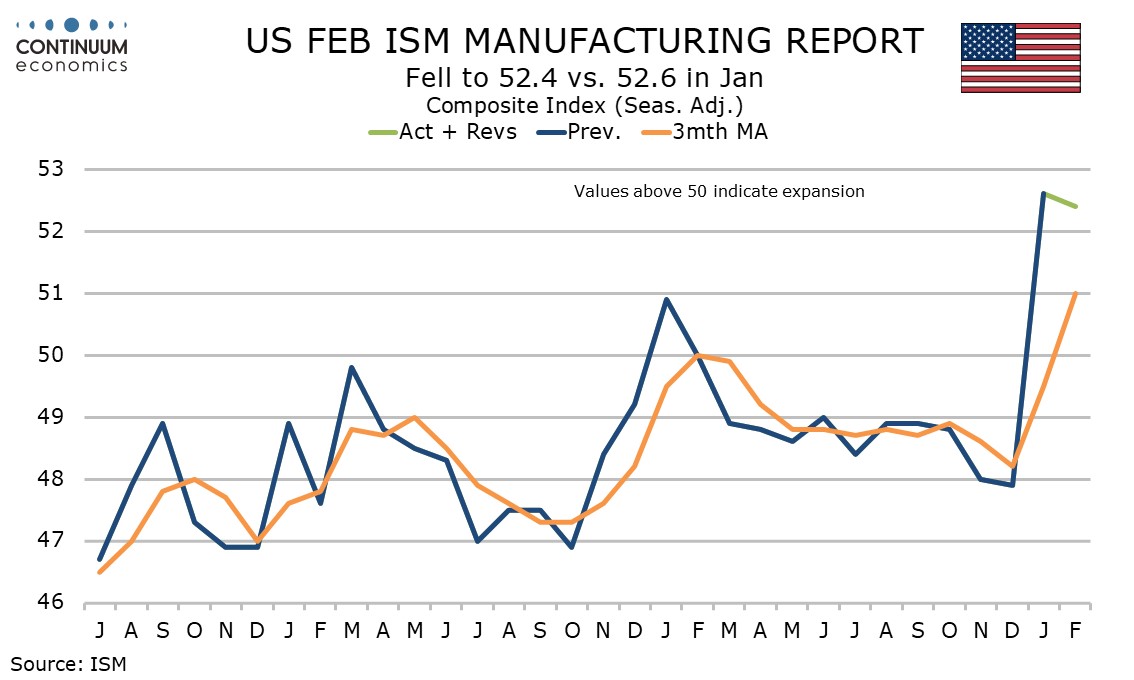

U.S. February ISM Manufacturing - January surge largely sustained, prices bounce

February’s ISM manufacturing index at 52.4 is only marginally down from January’s 54.6 which was the highest August 2022. We now have two straight clearly positive numbers to follow two straight negatives, a sign that manufacturing activity is picking up in early 2026.

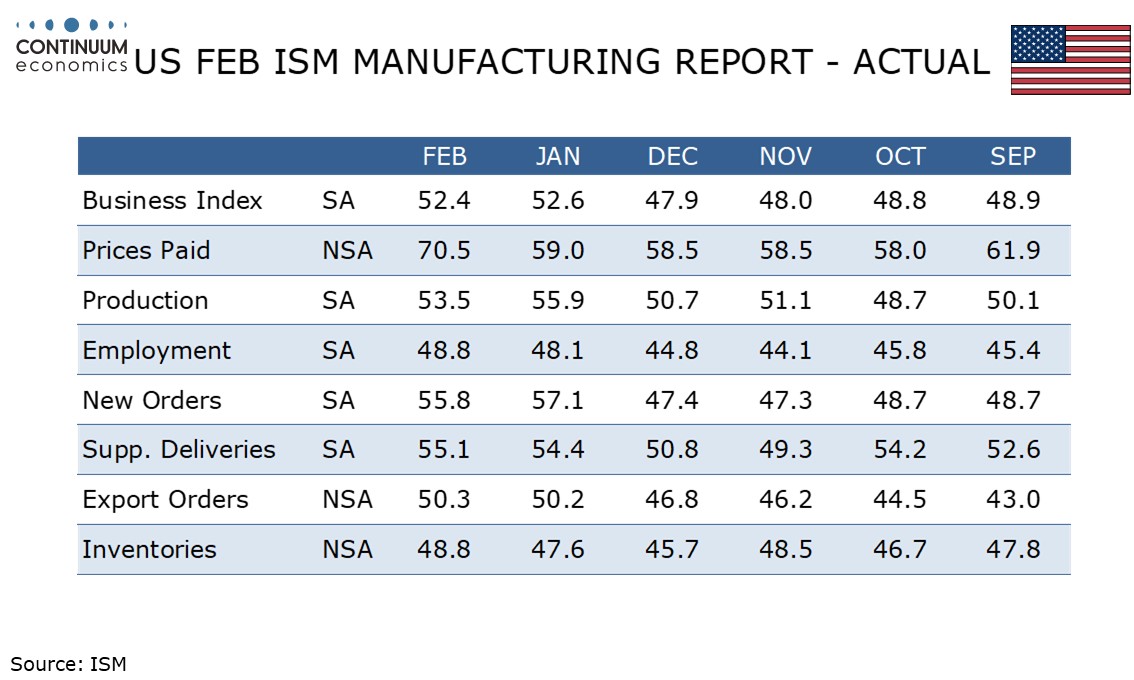

Detail of the composite shows slowing in production (to 53.5 from 55.9) and new orders (to 55.8 from 57.1) after strong January gains though levels remain positive and well above December’s.

Employment at 48.8 from 48.1 is still negative though the highest since January 2025. The final components of the composite, inventories at 48.8 from 47.6 and deliveries at 55.1 from 54.4 also contributed positively, deliveries the highest since May and a hint of inflationary risk. A rise in orders backlogs (not a contributor to the composite) to 56.6 from 51.6 is too.

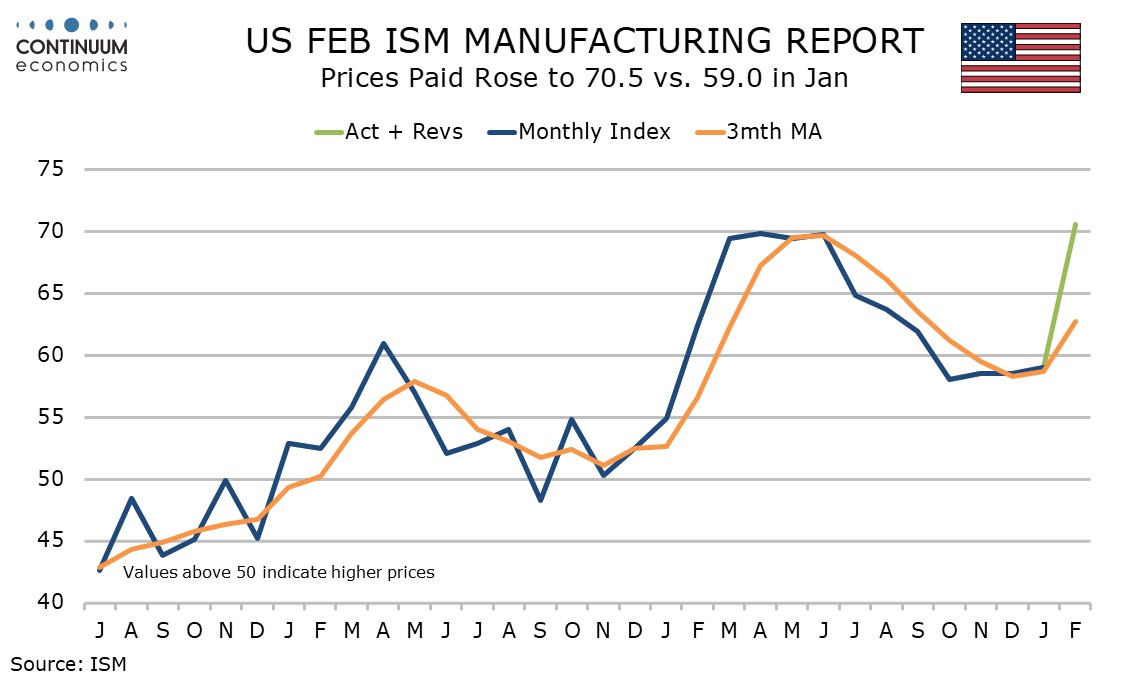

Prices paid do not contribute to the composite but at 70.5 from 59.0 provided a significant upside shock reaching the highest since June 2022 and marginally beating the highs seen in the aftermath of the tariff announcement. This is worrying coming before the fresh conflict in the Middle East but there may be temporary weather-related issues behind the rise.

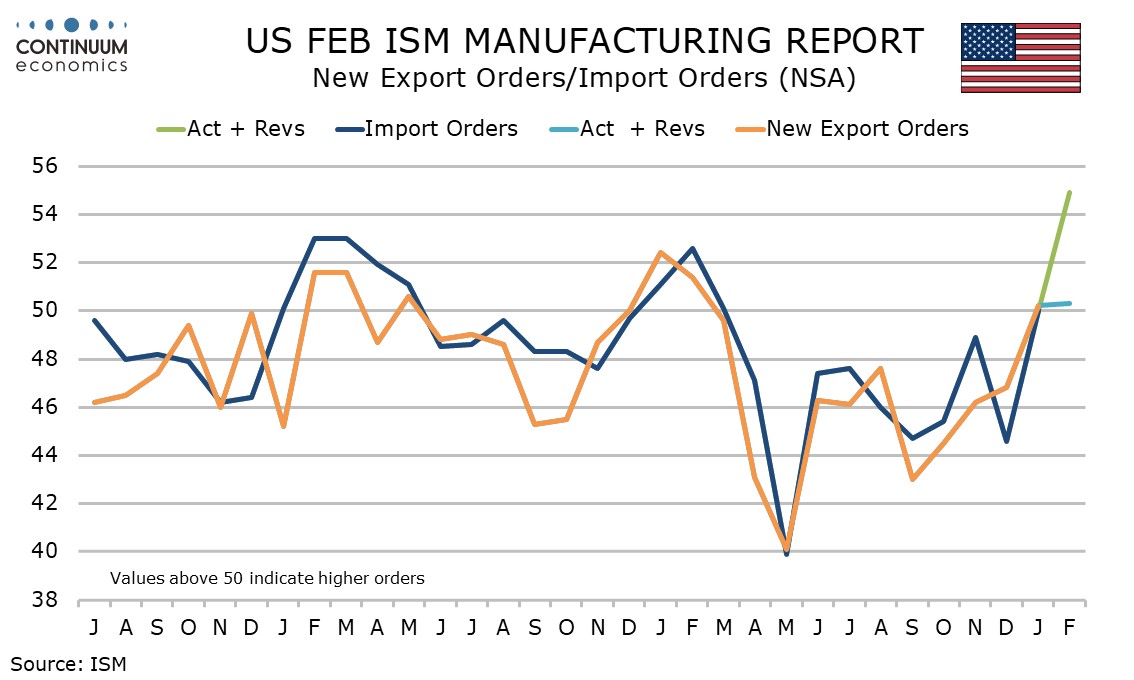

Also not contributing to the composite are the exports and imports indices. Exports remain near neutral at 50.3 from 50.2 but imports saw a bounce to 54.9 from 50.0 to reach their highest level since February 2022. The Supreme Court ruling against the tariffs may have played a part in this but we doubt it is the full story.