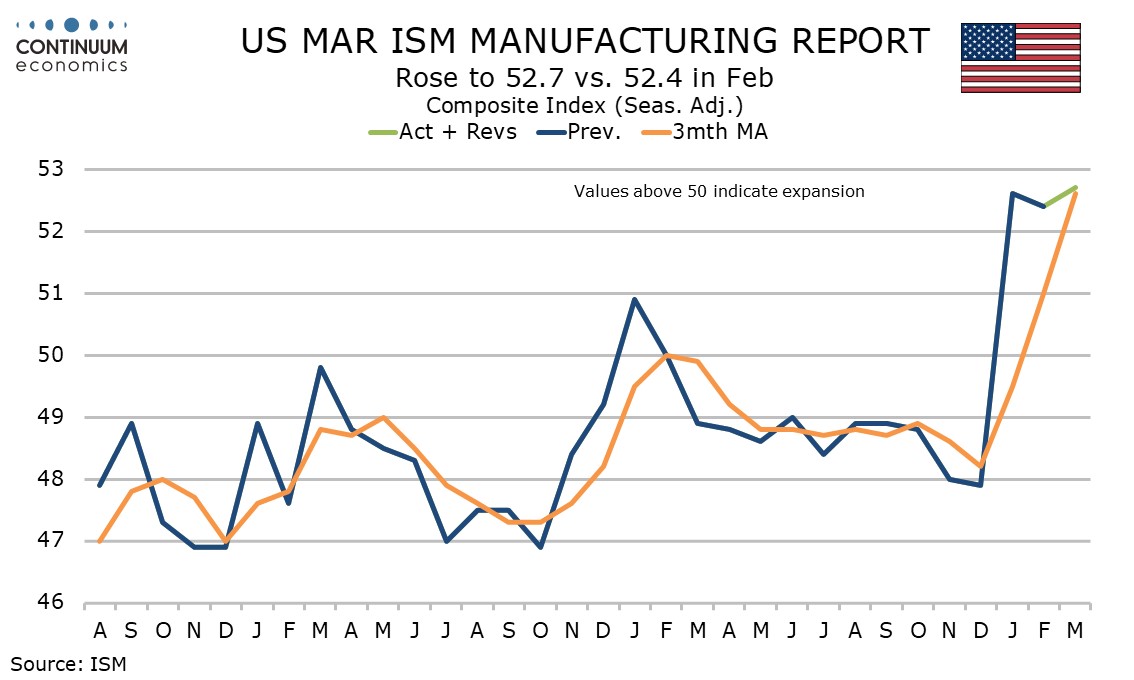

U.S. March ISM Manufacturing - Composite firm but new orders slower and prices strong

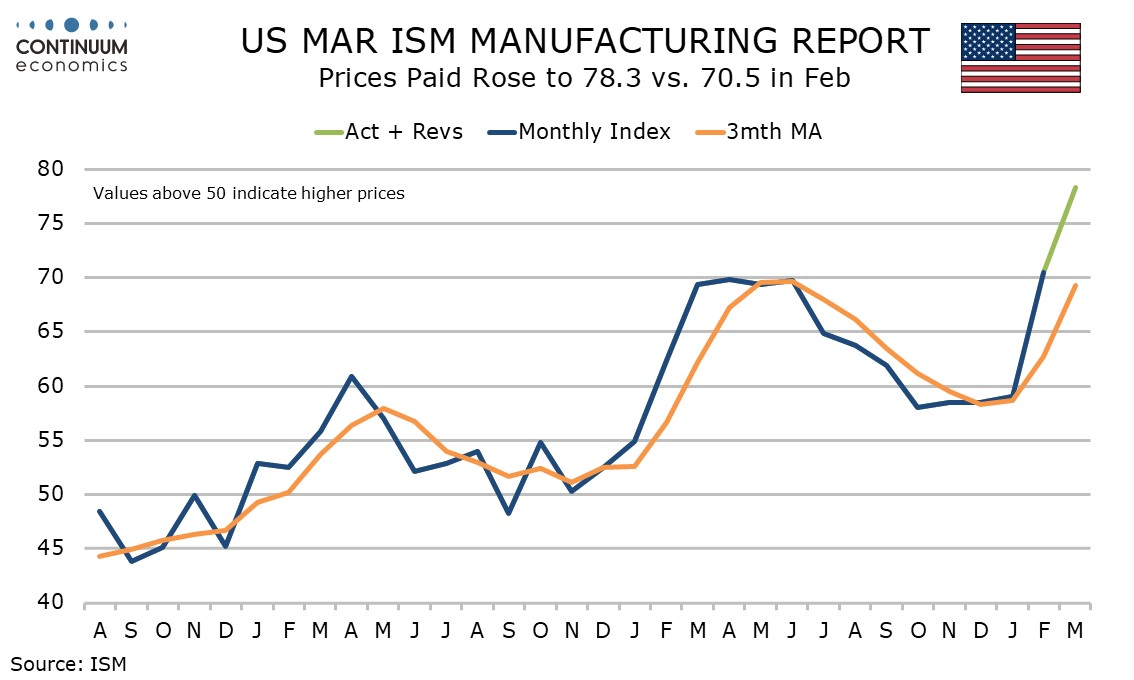

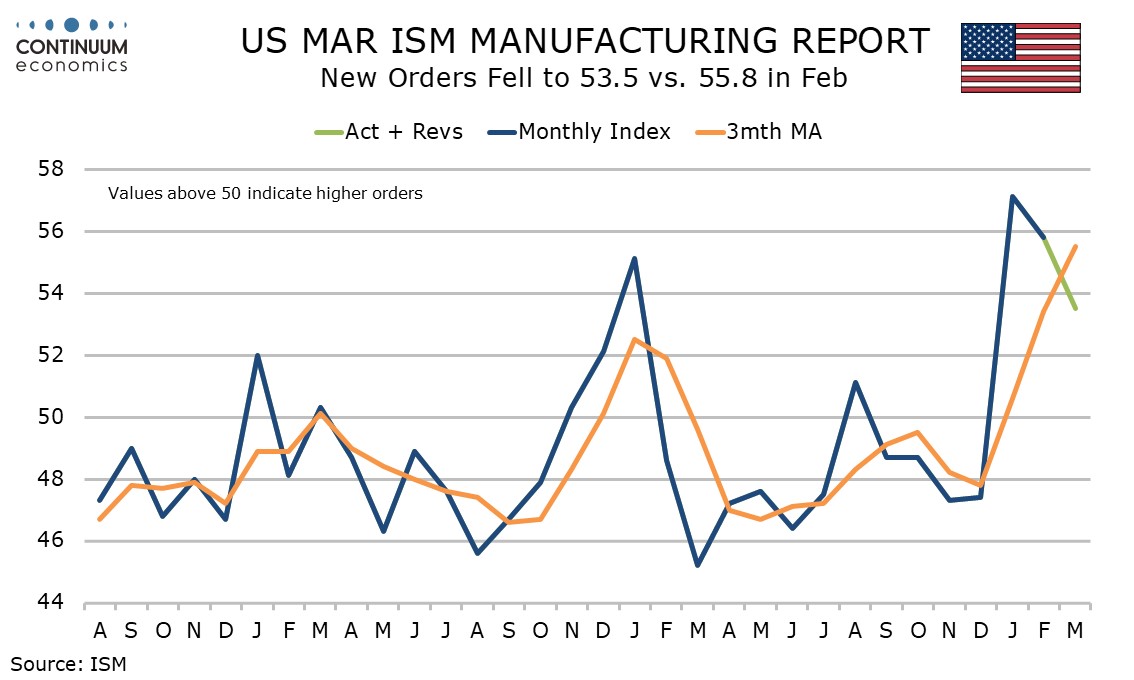

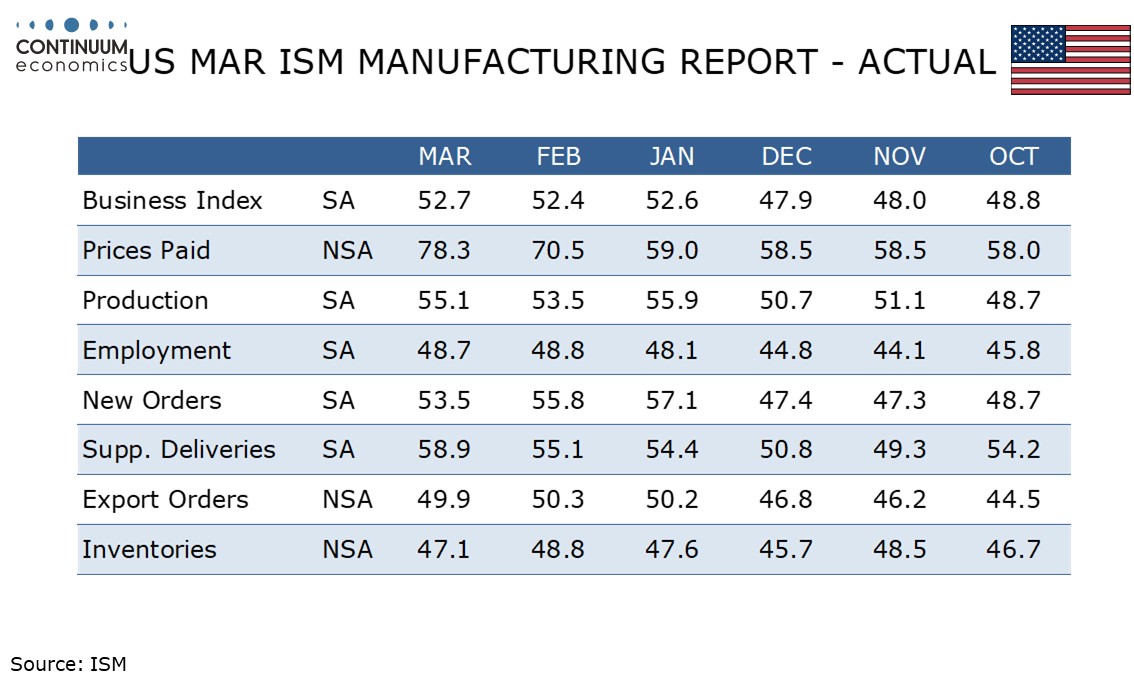

March’s ISM manufacturing index at 52.7 is slightly improved from February’s 52.4 and maintains a sharp improvement into positive territory in Q1. However rising prices paid and slowing new orders provide some warnings that surging energy prices could have adverse effects.

Prices paid are not a contributor to the composite but at 78.3 from 70.5 in February and 59.0 in January have reached their highest level since June 2022.

New orders at 53.5 are down from 55.8 in February and 57.1 in January but remain well above December’s 47.4. Seasonal adjustments provided some restraint, though a modest slowing was seen even before seasonal adjustment.

Production was improved at 55.1 from 53.5 and employment almost unchanged at 48.7 from 48.8. Inventories slowed to 47.1 from 48.8.

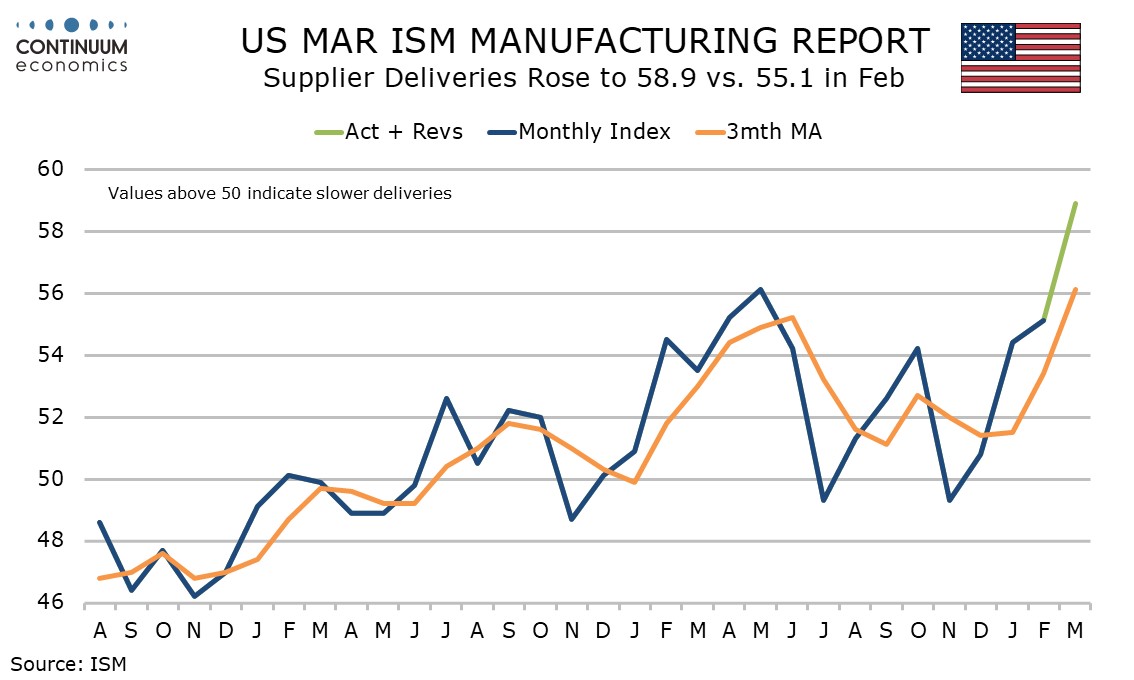

The main positive in the composite was delivery times, at 58.9 from 55.1. Supply disruptions related to the conflict in the Middle east may be behind this, which adds to inflationary risks.

Imports and exports do not contribute to the composite. Both are modestly slower, imports at 52.6 from 54.9 and exports at 49.9 from 50.3.