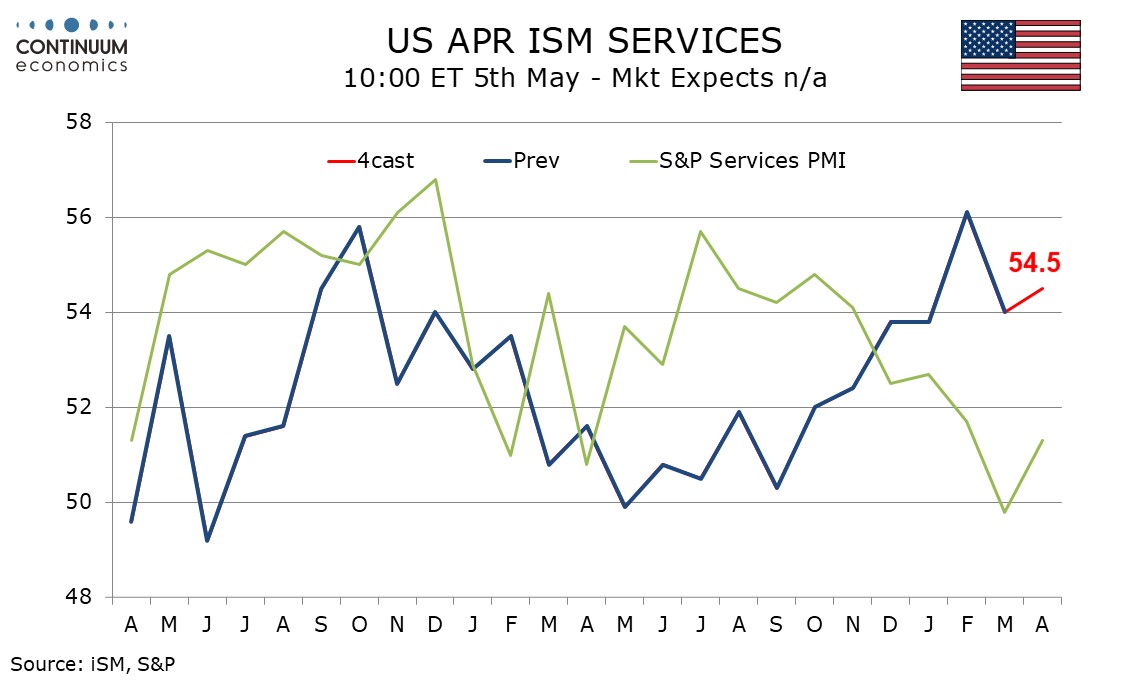

Preview: Due May 5 - U.S. April ISM Services - March new orders imply underlying strength persists

We expect April’s ISM services index to pick up to 54.5 from 54.0 in March, after slipping from February’s 56.1, which was the highest reading since July 2002. April’s S and P Services PMI picked up, but was still quite weak at 51.3 after slipping to 49.8 in March. The two series are not well correlated.

March’s slowing in the ISM services index came despite a rise in new orders to 60.6, the highest level since February 2022 and suggesting underlying strength despite the risks coming from the Middle East.

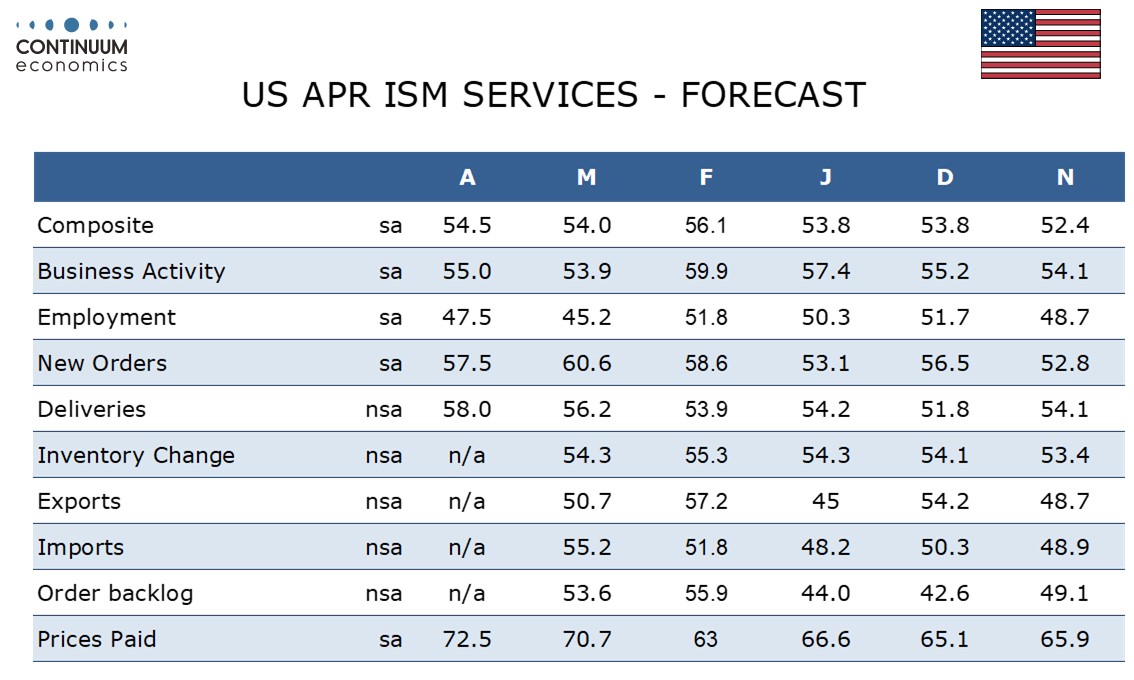

We expect new orders to correct lower to 57.5 in April but the other three components of the composite to improve, business activity to 55.0 from 53.9, employment to 47.5 from March’s very weak 45.2, and delivery times to 58.0 from 56.2. Supply disruptions in the Middle East may lift the latter.

Prices paid do not contribute to the composite and here we see a rise to 72.5 from 70.7, led by energy, extending bounce from February’s 63.0. This will be the highest reading since August 2022.