U.S. March Empire State survey weak, Import and Export Prices picking up in early 2024

March’s Empire Sate manufacturing index of -20.9 is very weak and down from -2.4 in February. This index is however more volatile than most manufacturing surveys and does not tell us much about what other surveys will show. Separately February import prices have shown a second straight rise, of 0.3%, and like CPI and PPI have started 2024 stronger than they finished 2023.

The Empire State details are weak across the board in the current month detail apart from the price indices which have not changed much. 6 month expectations however remain positive, at 21.6 from 21.5, with the components showing a similar message. 6 month price details are also slightly firmer.

Most manufacturing surveys have been modestly negative in recent months though the S and P’s has turned positive. The Empire State data argues against other surveys turning positive, but is not a conclusive signal for weakness give its exceptional volatility. Weak as March data is, January’s was weaker still.

Most manufacturing surveys have been modestly negative in recent months though the S and P’s has turned positive. The Empire State data argues against other surveys turning positive, but is not a conclusive signal for weakness give its exceptional volatility. Weak as March data is, January’s was weaker still.

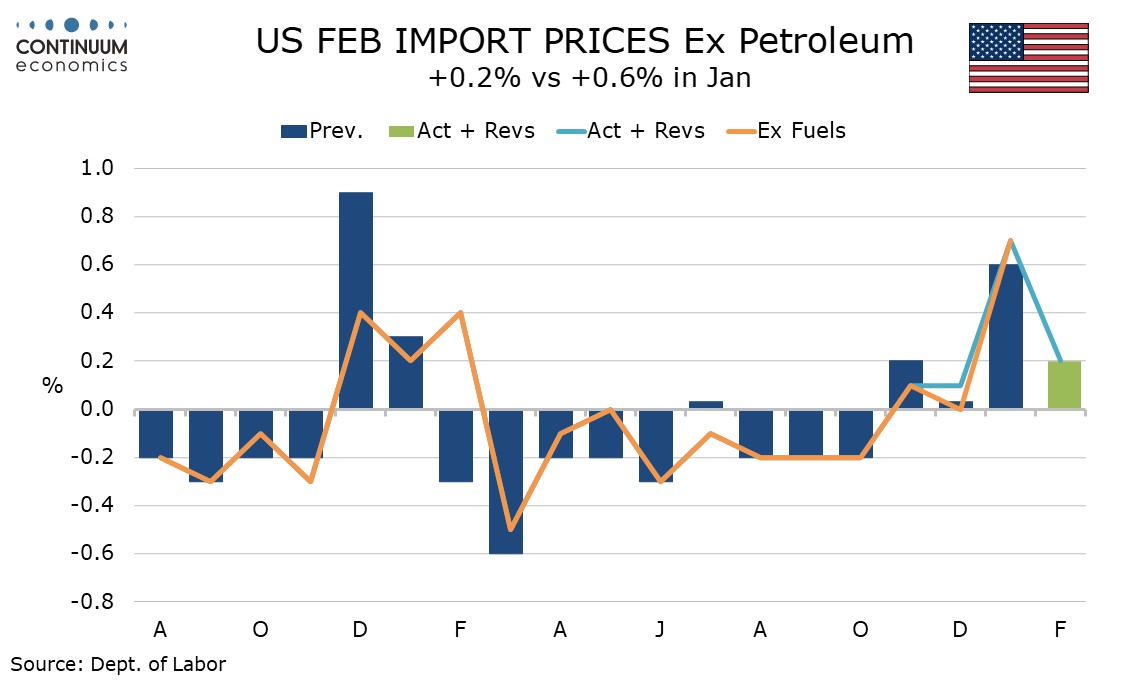

Import prices fell in each month of Q4 but ruse by 0.8% in January and 0.3% in February. Ex petroleum import prices trended lower through most of 2023 before rising by 0.2% in November. After a flat December a 0.6% rise in January was followed by a 0.2% gain in February.

Export prices also fell in each month of Q4 before gains of 0.9% in January and 08% in February. This is consistent with PPI and CPI which both came in above the late 2023 trend in both January and February of 2024.

Export prices also fell in each month of Q4 before gains of 0.9% in January and 08% in February. This is consistent with PPI and CPI which both came in above the late 2023 trend in both January and February of 2024.