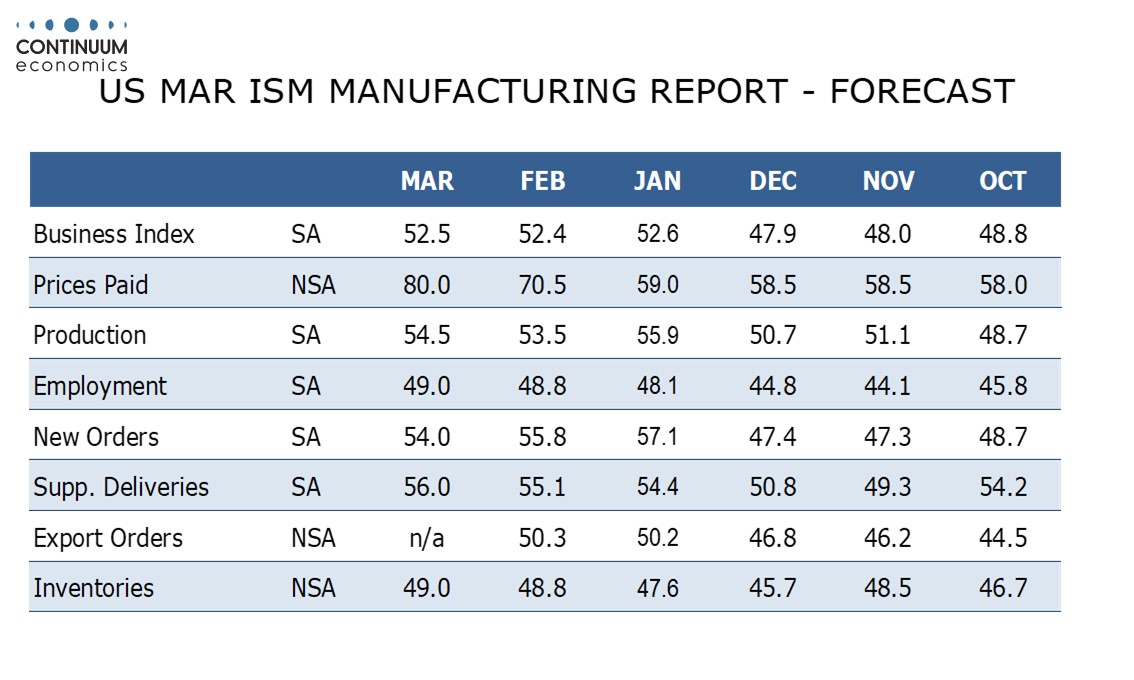

Preview: Due April 1 - U.S. March ISM Manufacturing - Sustaining recent improvement

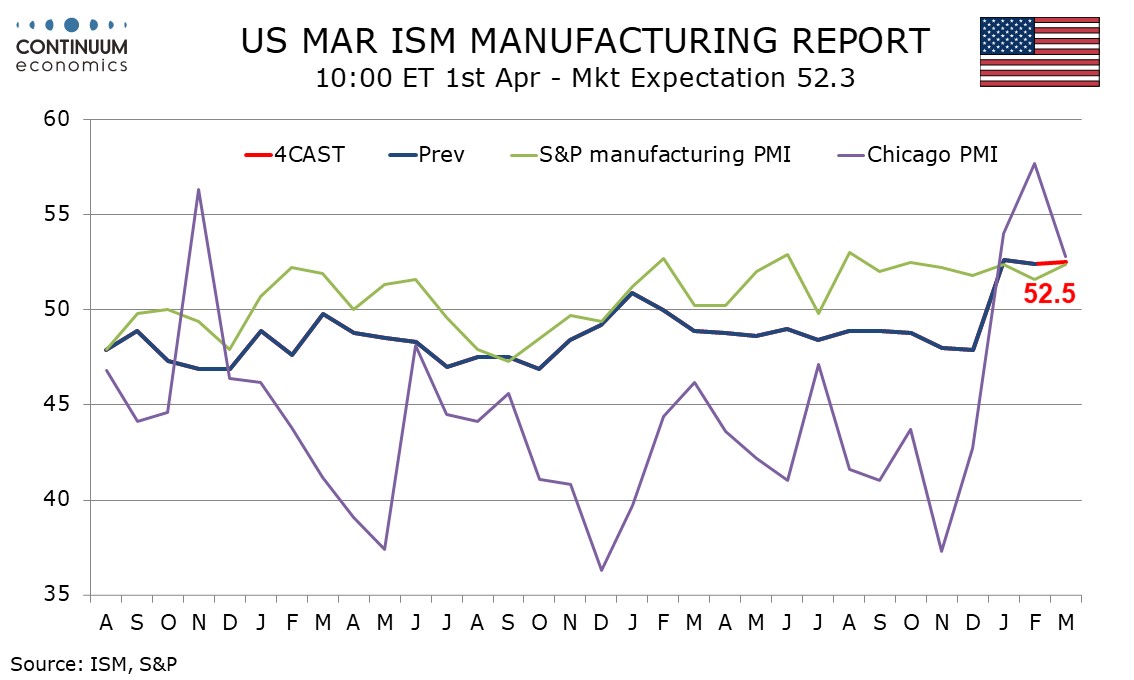

We expect March’s ISM manufacturing index to maintain the significantly improved tone of January and February data, edging marginally higher to 52.5 from 52.4. This would be a third straight positive to follow ten straight negatives.

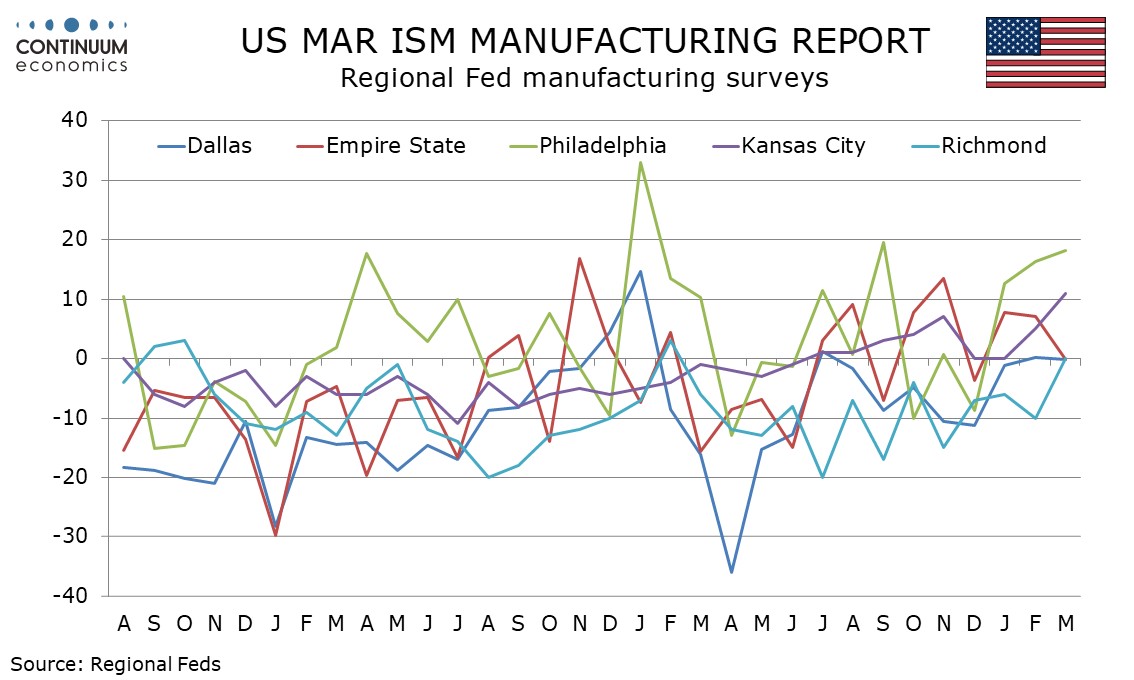

Other March manufacturing surveys have been on balance positive with the S and P’s survey rebounding from a February dip and the Kansas City and Philly Fed’s increasingly strong. Empire State, Richmond and Dallas Fed indices were near neutral, Empire State slipping from February, the Richmond Fed improved and the Dallas Fed little changed. The Chicago PMI was less positive.

In breakdown for the ISM composite, we expect any negative impact from the conflict in the Middle East to be concentrated in new orders, where seasonal adjustments may also contribute to a correction from recent strength. We expect improvement in the other four contributors to the composite, production and employment responding to recent strength in new orders, while the situation in the Middle East poses upside risk to delivery times and inventories.

Prices paid do not contribute to the composite and here we see a significant increase in response to energy prices, to 80.0 from 70.5, reaching the highest level since May 2022.