U.S. May Empire State Manufacturing Survey - Strength in both activity and prices

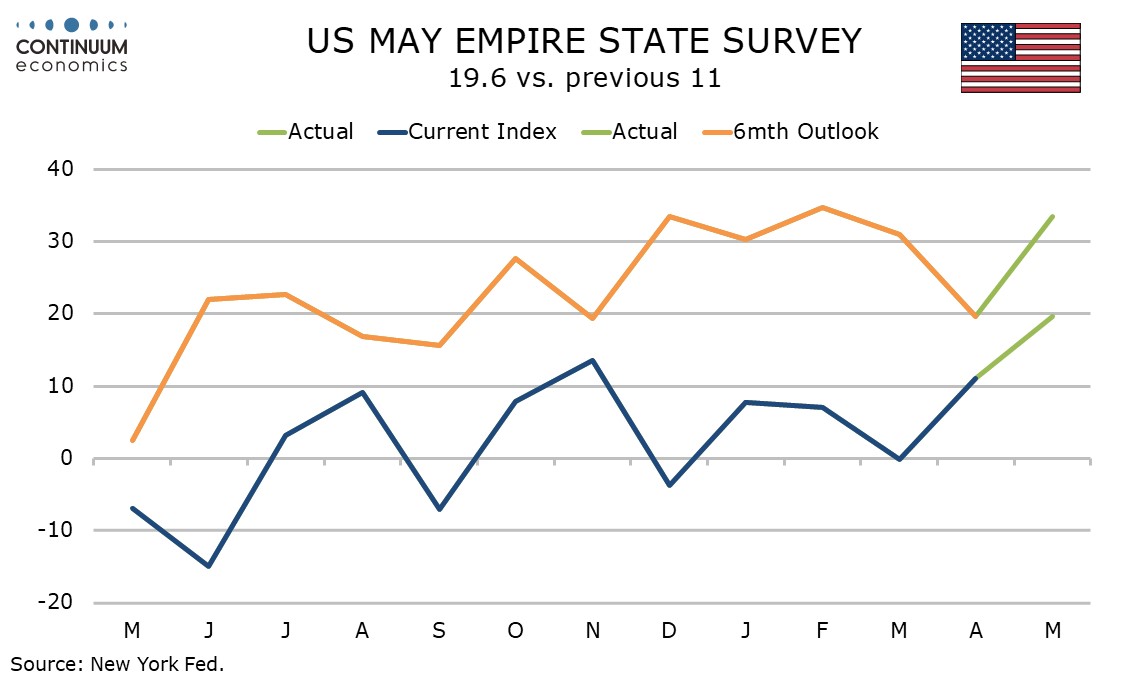

May’s Empire State manufacturing index at 19.6, up from 11.0 in April, is the highest since April 2022, giving further evidence that the manufacturing sector is holding up well despite the Middle east conflict.

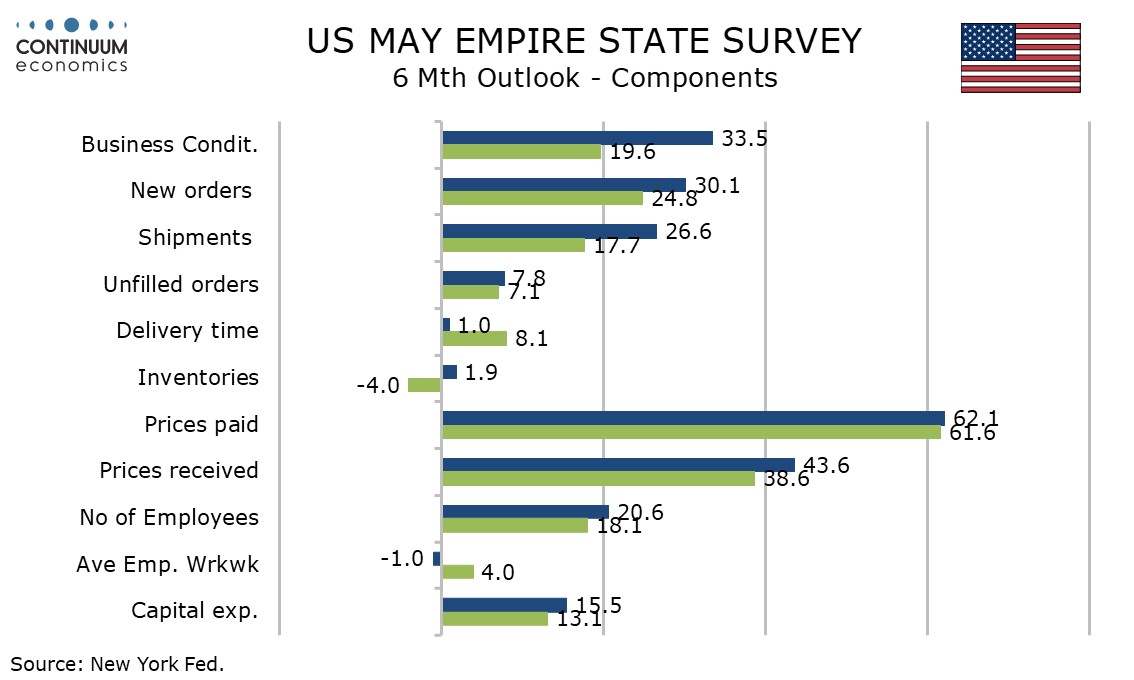

Even 6-month expectations are firm at 33.5, more than fully reversing a dip in April to 19.6, and back near levels seen ahead of the war.

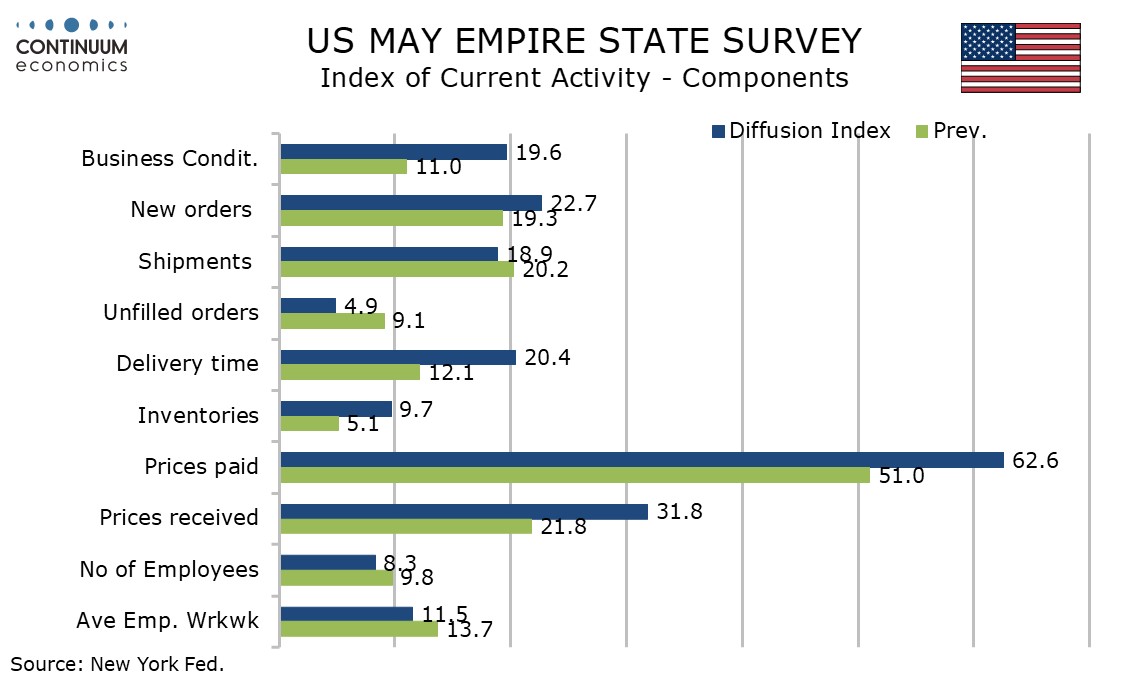

Current month data shows new orders up to 22.7 from 19.3, reaching their highest since December 2021, though employment at 8.3 from 9.8 and the workweek at 11.5 from 13.7 are slightly less strong than in March.

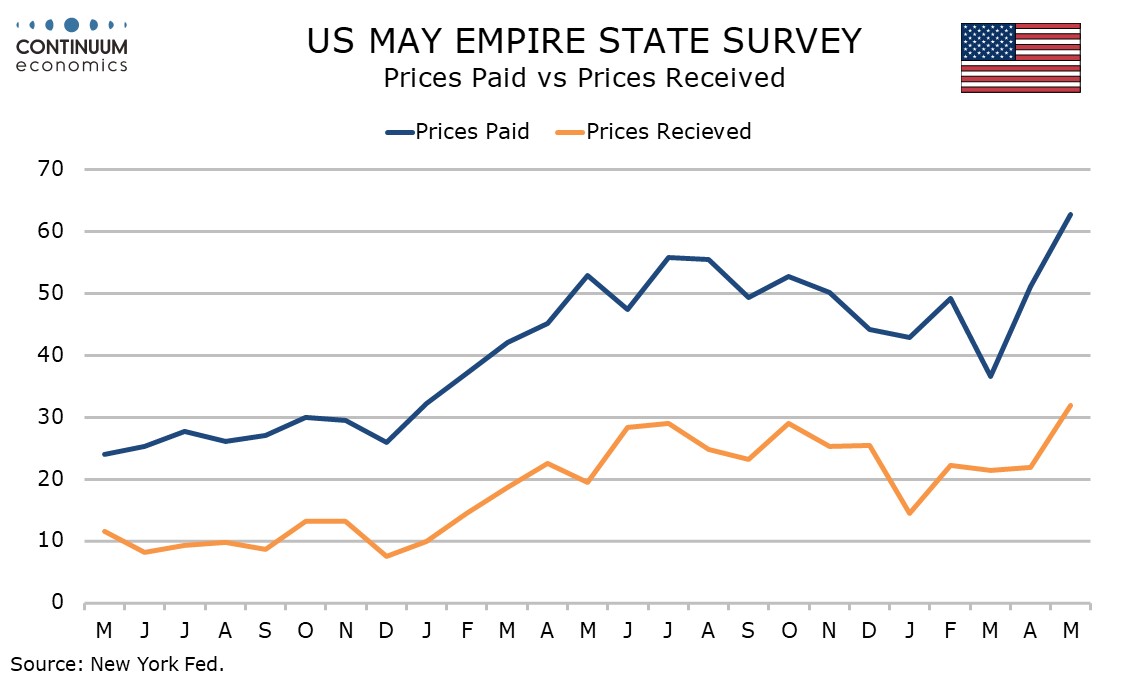

Price data is firm, with prices paid at 62.6 from 51.0 the highest since July 2022 and prices received at 31.8 from 21.8 the highest since August 2022.

6-month price expectations are also higher, paid at 62.1 from 61.6 and received at 43.6 from 38.6, though these indices were respectively higher more recently, in October and November of 2025 respectively. Then tariffs rather than the energy shock was the primary concern.