Preview: Due August 5 - U.S. July ISM Services - Unlikely to match strong S&P Services PMI

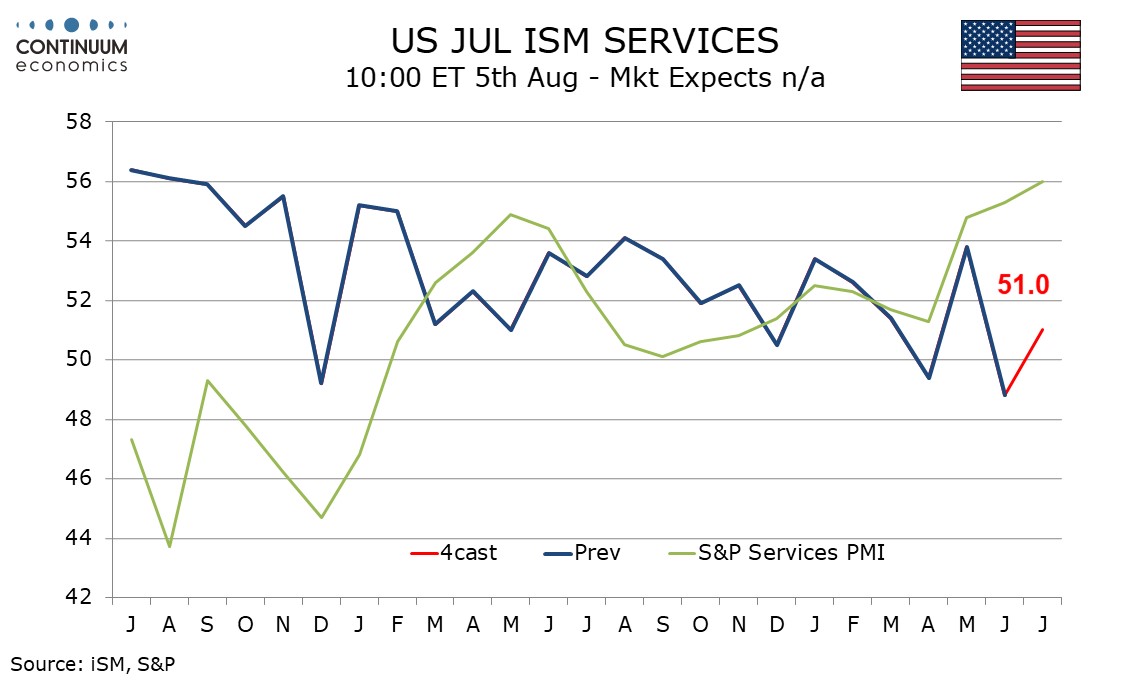

We expect July’s ISM services index to correct higher to 51.0 after slipping to 48.2, its lowest since the pandemic in May 2020. However the index will remain a lot weaker than the S and P services PMI, which in July saw a third straight rise to 56.0, to its highest since March 2022.

The ISM services index does not have a good relationship with that of the S and P. In fact the ISM index has been trending marginally lower, albeit with plenty of volatility, over the last two years while the S and P index has been trending higher. We believe the S and P index is more sensitive to bond yields and interest rate expectations, helping to explain its recent outperformance. Regional Fed service sector surveys have mostly remained subdued.

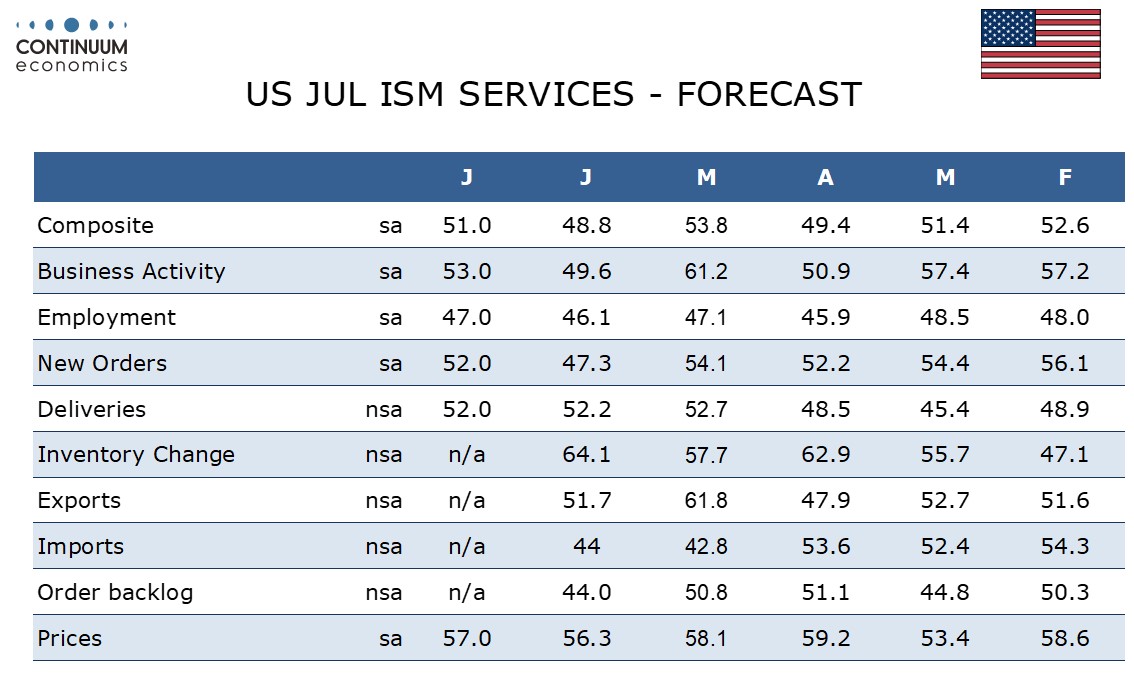

We expect the ISM services bounce to be led by new orders and business activity, both of which saw sharp dips below neutral in June. Employment may also improve a touch but we expect a sixth straight sub-neutral reading. For deliveries risks lean to the downside. Prices paid do not contribute to the composite. Here we expect an index of 57.0, up from 56.3 in June but below May’s 58.1, leaving trend with little direction.

We expect the ISM services bounce to be led by new orders and business activity, both of which saw sharp dips below neutral in June. Employment may also improve a touch but we expect a sixth straight sub-neutral reading. For deliveries risks lean to the downside. Prices paid do not contribute to the composite. Here we expect an index of 57.0, up from 56.3 in June but below May’s 58.1, leaving trend with little direction.