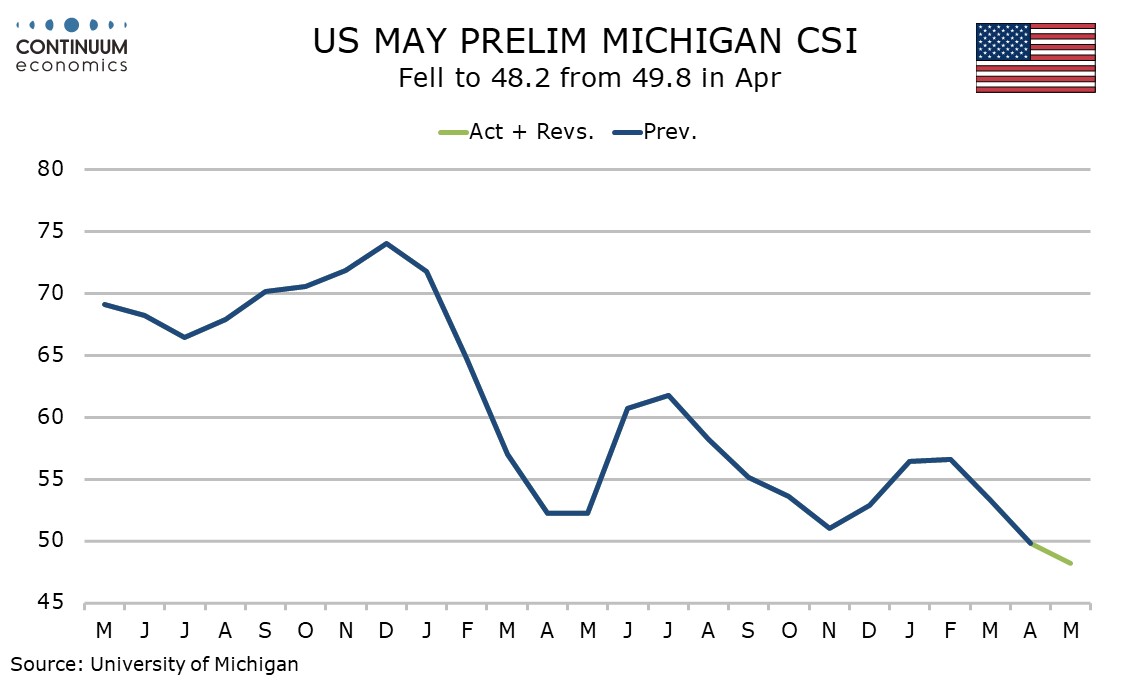

U.S. Preliminary May Michigan CSI - Dip on current conditions, expectations slightly improved

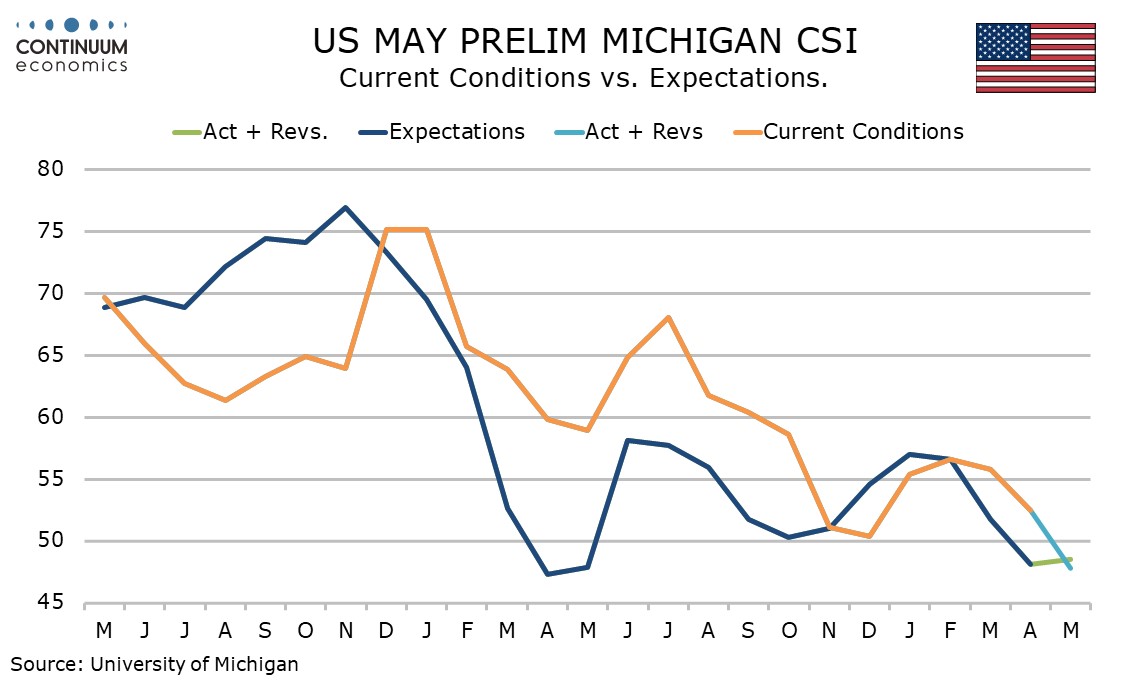

The preliminary May Michigan CSI of 48.2 is down from 49.8 in April and weaker than expected. The details are however more surprising, with the fall due to current conditions not expectations and inflation expectations slightly softer.

The current conditions index fell to 47.8 from 52.5 and hints that strength in energy prices is starting to weigh on activity, though there is no sign of this in recent initial claims data.

The increase in 6-month expectations is marginal, to 48.5 from 48.1, but does follow three straight declines.

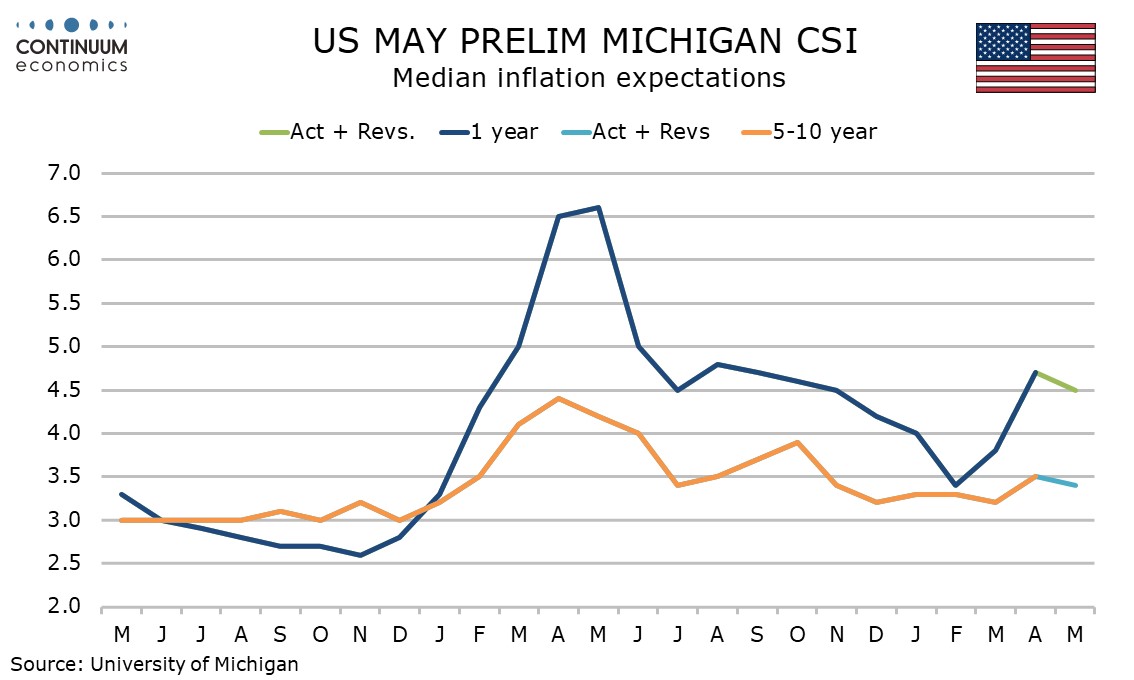

The improvement in 6-month expectations may be on lower inflation expectations, 1-year inflation expectations fell to 4.5% from 4.7% and the 5-10 year view fell to 3.4% from 3.5%.

These are still above February’s respective outcomes of 3.8% and 3.2% though some way off the post-tariff highs above 6.0% for the 1-year view and above 4.0% for the 5-10 year view. Given that the energy shock has not delivered extreme pessimism on inflation, sentiment is notably weak.