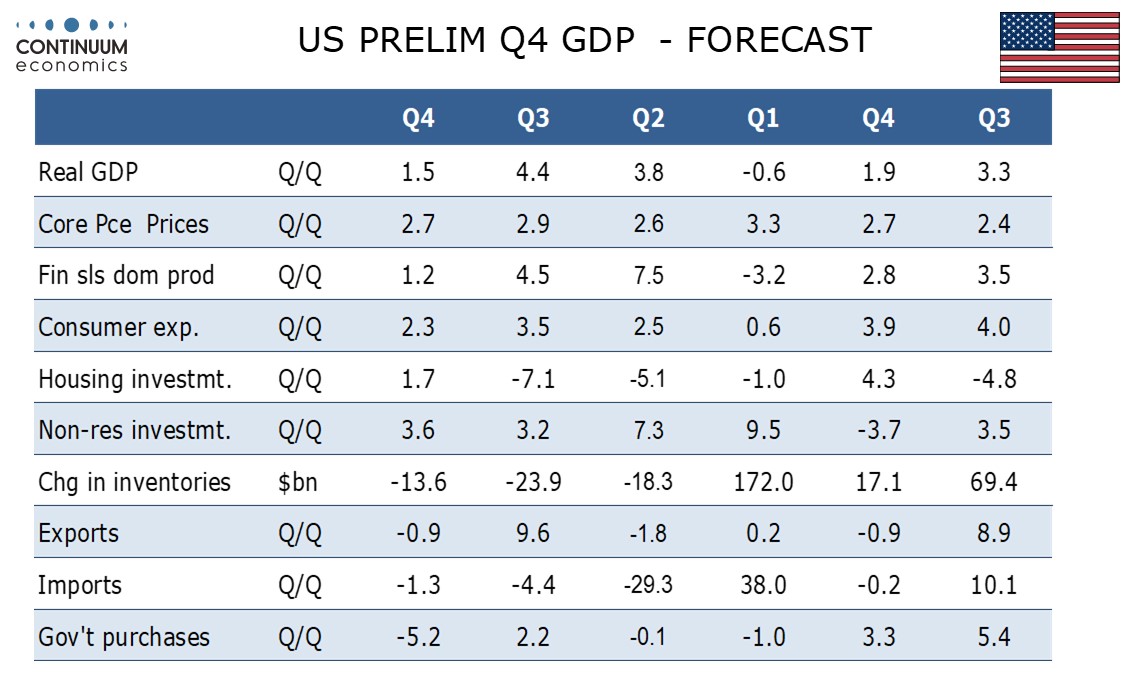

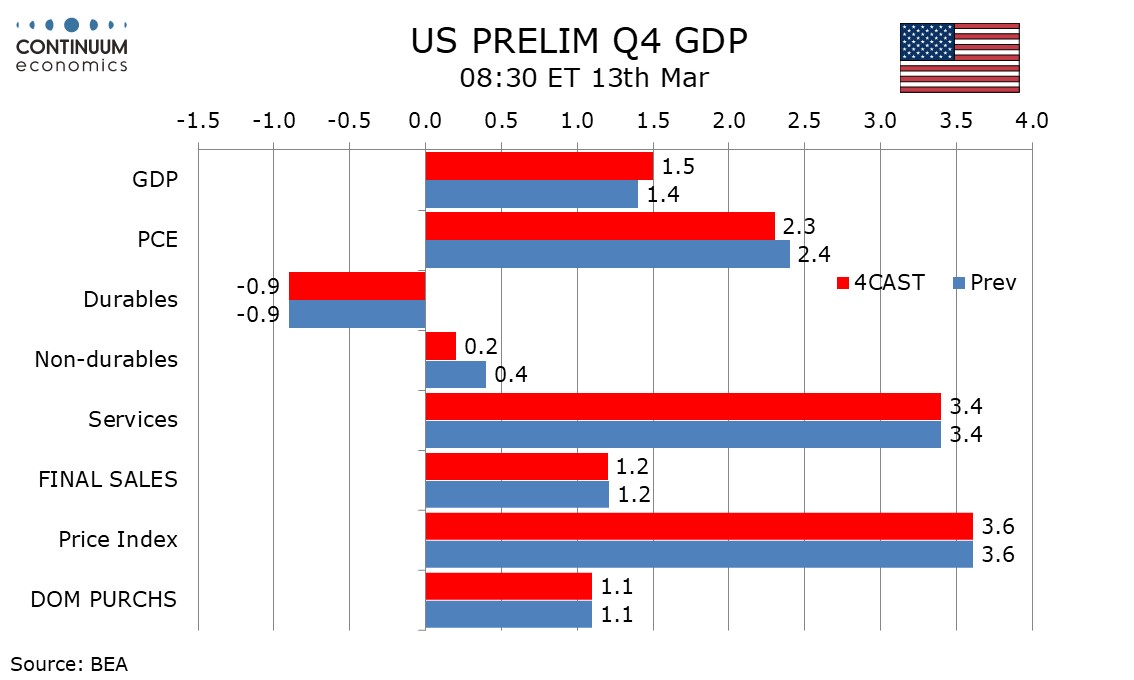

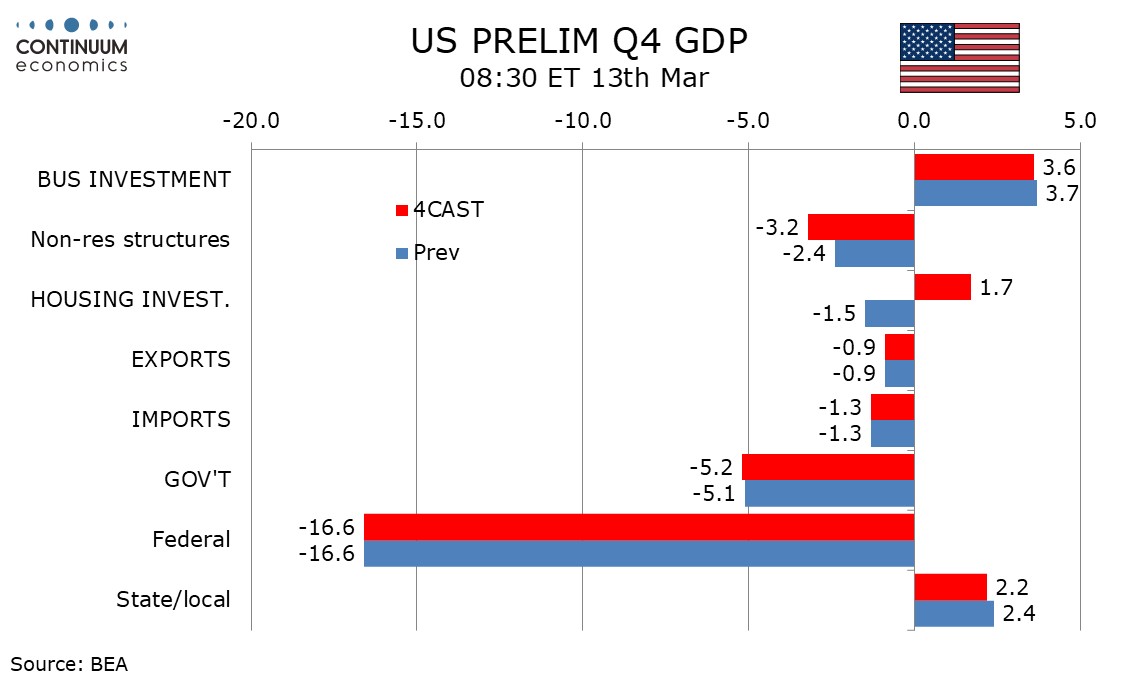

Preview: Due March 13 - U.S. Preliminary (Second) Estimate Q4 GDP - Marginally stronger on housing

We expect a marginal upward revision to Q4 GDP to 1.5% in the preliminary (second) estimate from 1.4% in the advance (first) release, led by an upward revision to housing investment to a 1.7% rise from a 1.5% decline.

The upward revision to housing investment is implied by November and December construction spending data, which was released after the advance GDP data. This will outweigh implied marginal downward revisions to non-residential construction, both private and public, and retail sales.

While we expect the USD revision to both final sales and final sales to domestic buyers to match that seen for GDP, the annualized percentage changes to the former two are likely to be unrevised, at 1.2% and 1.1% respectively. We do however expect final sales to private domestic buyers to be revised up to 2.5% from 2.4%. Government was restrained by the shutdown.

We do not expect any revisions to the price indices, of 3.6% for GDP, 2.9% for PCE and 2.7% for core PCE. The overall price index was led higher by government, which may have been impacted by the shutdown.