Preview: Due May 13 - U.S. April PPI - Core rates to pick up from below trend March

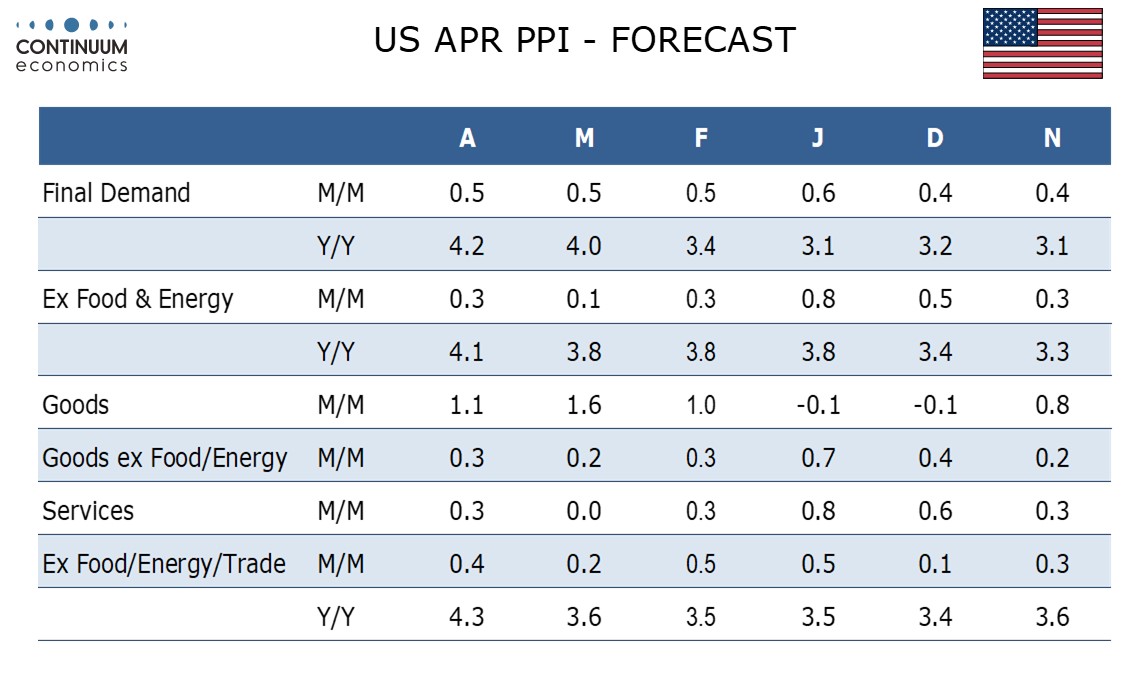

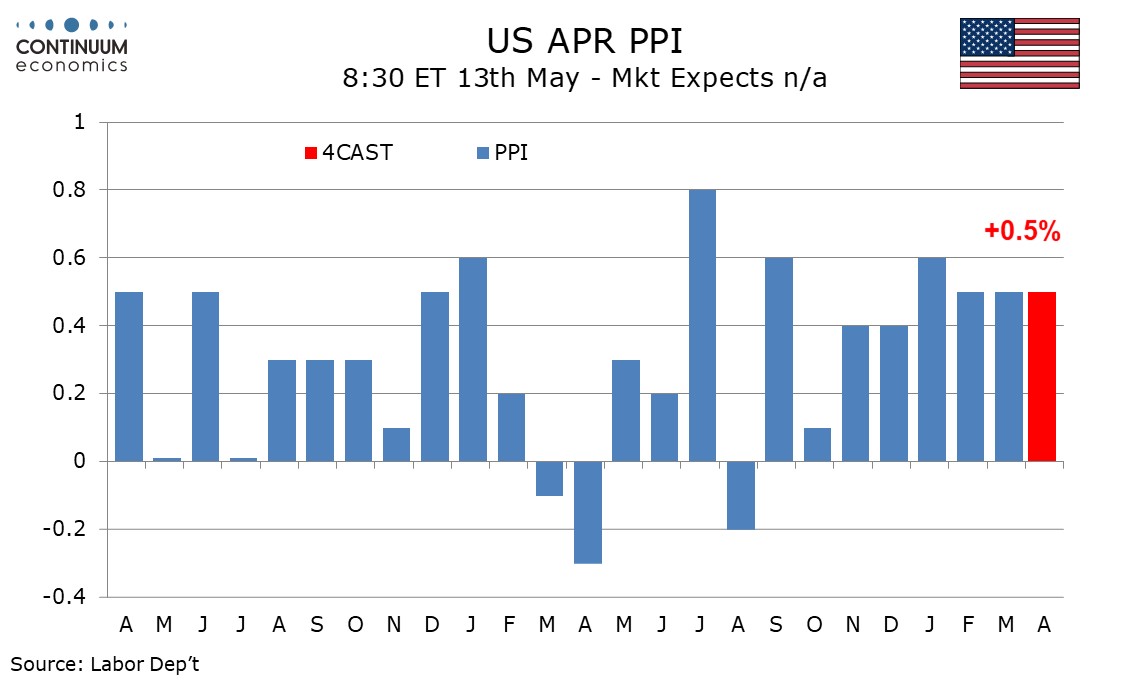

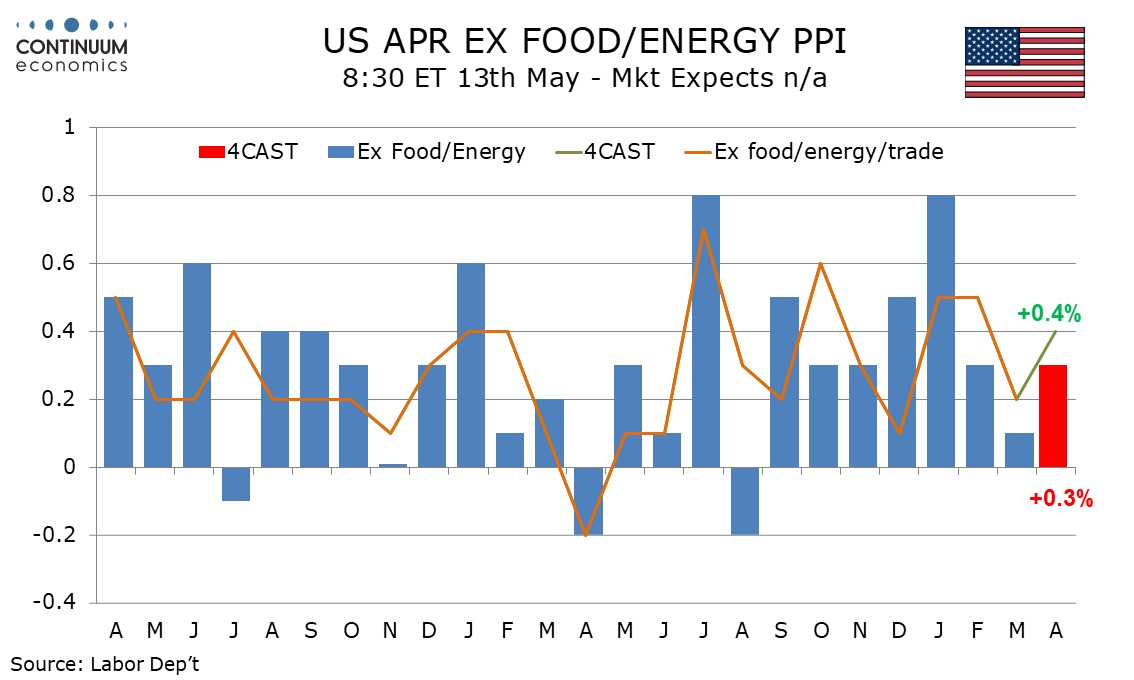

We expect PPI to rise by 0.5% overall in April for a third straight month. We expect the lift from energy to be less sharp than in March, but the core rates to pick up from below trend March gains, ex food and energy to 0.3% from 0.1%, and ex food, energy and trade to 0.4% from 0.2%.

The core rates would be similar to February’s when ex food and energy rose by 0.3% and ex food, energy and trade rose by 0.5%, and less strong than in January, when respective gains of 0.8% and 0.5% were seen. We expect a 4.0% increase in energy after a rise of 8.4% in March and food to rebound by 0.6% after a 0.3% decline in March.

We expect goods ex food and energy to rise by 0.3% after March’s 4-month low of 0.2%, but this series has probably peaked as the impact of tariffs starts to fade. We expect services to rise by 0.3% after a flat March, with continued strength in transport and utilities, which rose by 1.3% in March, but a third straight moderate decline in trade, extending a correction from strong gains in December and January. Other services are likely to pick up after a below trend 0.1% increase in March.

We see yr/yr growth rising to 4.2% from 4.0% overall, to 4.1% from 3.8% ex food and energy, and to 4.3% from 3.6% ex food, energy and trade. All three rates would be at their strongest since February 2023.