FX Daily Strategy: Europe, April 11th

Tariff Man's Words Remain Key

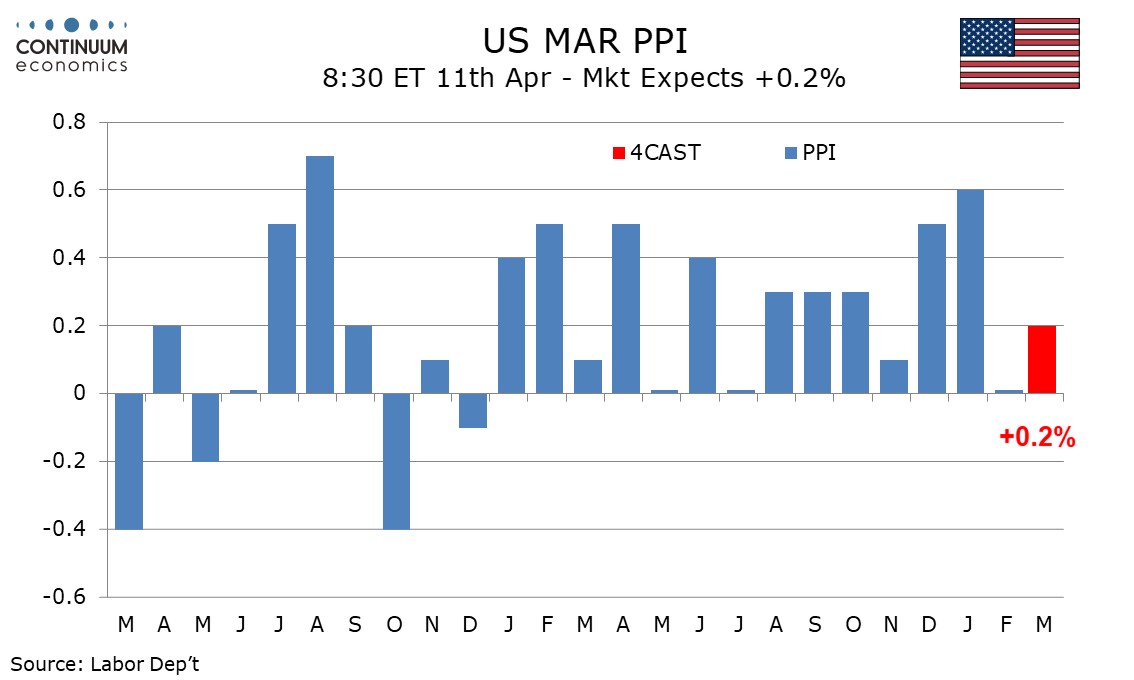

U.S. March PPI to bounce from a weak February

Resilience for UK GDP in Spite of Soft(er) Surveys

USD/JPY Not off the Hook

The tariff man continues to rock the market with his policy. Trump has announced another 90 day delay for his latest reciprocal tariff, except China. He doubled up the pressure on China by another 50%, citing currency manipulation, forced transfer of trade secret and a basket of reasons. While China did not back down and indicates little chance of a positive development from the two biggest economy in the world, market participants are cheering on any positive headlines. The internal pressure from U.S. also seems to be a trigger for Trump's move. On Friday, any remark from Trump will dominate market sentiment. Surprises will likely on the upside with most bad news out in the light, unless the tariff man strike with another round of tariffs. Market participants are looking for any reason to buy after the slaughter last week.

We expect March PPI to increase by a moderate 0.2% overall, restrained by dips in food and energy, but we expect a 0.4% bounce ex food and energy after a 0.1% dip in February. Ex food, energy and trade, we expect a rise of 0.3%. Gasoline prices have slipped, and seasonal adjustments are likely to exaggerate the decline. Food also looks due for a modest correction from recent strength led by eggs. February’s soft ex food and energy rate came despite a 0.4% rise in goods ex food and energy, which we expect to be repeated as tariff risks build. February saw service prices slip by 0.2% after a 0.6% rise in January. We expect a 0.4% rise in March, led by a rebound in trade, which slipped in February. We expect yr/yr growth to rise to 3.3% from 3.2% overall, and to 3.8% from 3.4% ex food and energy, reversing a February dip. Ex food, energy and trade, we expect yr/yr growth to be unchanged at 3.3%.

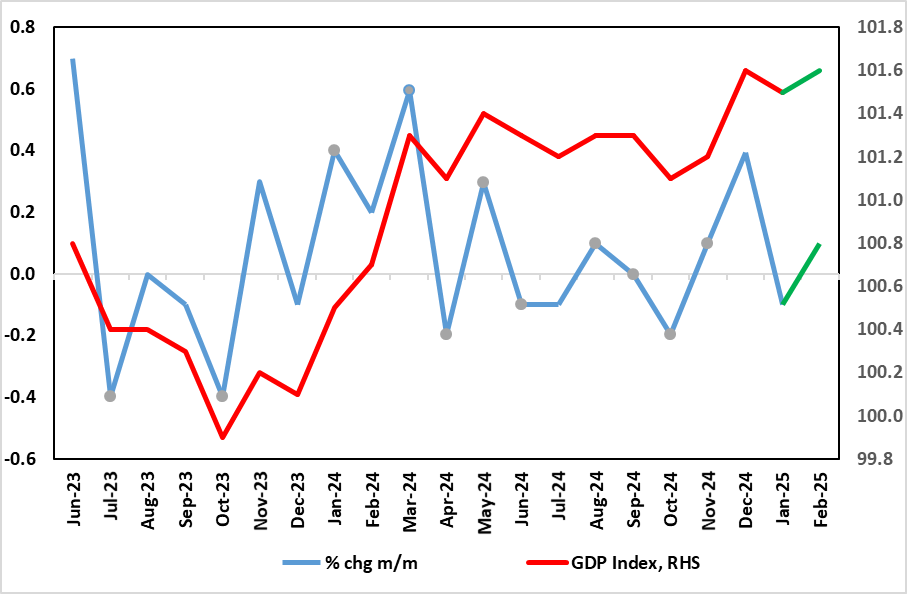

Figure: Actual GDP Looking Better into Early 2025

Despite a fresh downside surprise for January numbers, the odds are increasing that current quarter GDP will be decidedly positive as opposed to the weak(ish) picture we perceive. This is all the more likely given the 0.1% m/m ‘recovery’ we have penciled in for February (Figure 1) and where upside risks arise from higher property transactions (ahead of stamp duty rises) and already released solid retail sales but where warm weather may hamper utility output. Any growth of 0.1% would mean that the BoE estimate for Q2 (0.25%) would be most likely met and would put y/y at a largely unchanged 0.9%. But it is the outlook that will be dominating BoE thinking not least with tariffs coming in higher and wider than expected and where business worries were already fermenting given the weakness in surveys.

Indeed, the upside surprises in December of 0.4% contrasts with a much softer impression from surveys (Figure 1), the latter now showing weakness spreading into hitherto strong construction. Indeed the PMI for the latter suggested the sharpest pace of job shedding in the sector since October 2020. Regardless, despite a clear bounce in retail sales for the month, marked corrections in industry caused a small m/m drop in January of 0.1% m/m – as we expected. The firmness in December still implies a current quarter gain of 0.2% but the January drop probably more accurately underscores actual weakness regardless of what were actual upside risks from cold weather boosting already below-par utility output.

At the moment we still envisage growth of 0.2 q/q this quarter, twice what the BoE envisaged in its February report but where the MPC has since revised its estimate to a rise in Q1 of 0.25%. The question is what markets and the BoE prioritizes in assessing the policy outlook – weak survey data (Figure 2) or apparently resilient official numbers. Perhaps more notably, the data volatility of late suggest what may be changing seasonal factors post pandemic which may mean the UK economy in early 2025 sees similar but short-lived strong growth as seen in in the same period of last year – thus any solid Q1 gain needs to be put into that perspective

While major currencies are seeing significant volatility recently, USD/JPY will always be in the spotlight with its correlation to risk asset. USD/JPY has been on steady decline since the January BoJ hike as market participants are anticipating more tightening from the bank. The latest leg lower came from USD sell off and haven seeking from the bloodbath in equities. However, at the same time the odds of any imminent hike from the BoJ weakens as the impact of global tariffs will be negative towards the Japanese economy, especially for the auto industry. Given the history of BoJ, they are likely to be waiting on the side until the fog of war clears, cutting the legs off any sustainable rally for the JPY.

On the chart, the rebound from the 144.00 low to regain the 146.00 level and 146.54 March low has seen gains to retest the 148.00 congestion. Prices are unwinding oversold intraday and daily studies and break here cannot be ruled out though nearby see strong resistance at the 148.70, December low. Clearance here will open up scope to the 150.00 level but gains remains corrective within the bearish channel from the January high and expected to give way to fresh selling pressure later. Meanwhile, support is raised to the 146.54/146.00 area which should underpin for now.