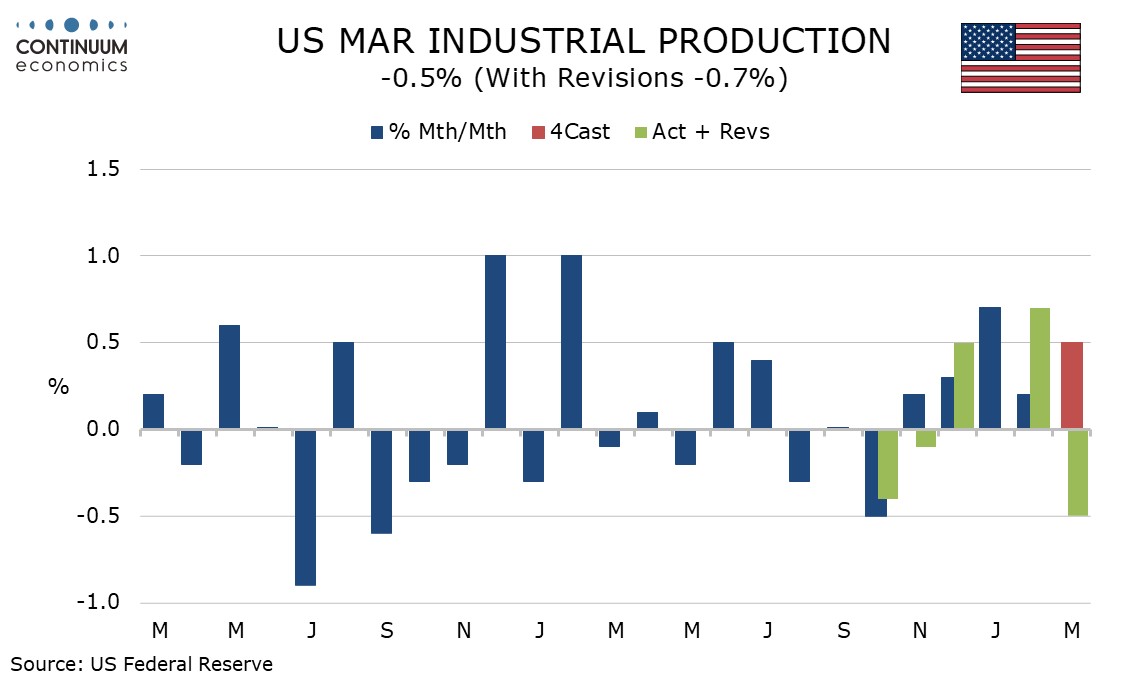

U.S. March Industrial Production - Hit by corrections in mining, utilities and autos

Contrasting resilience in Philly Fed and Empire State manufacturing surveys into April, March industrial production is surprisingly weak, with a 0.5% decline overall and manufacturing down by 0.1%. It is too early to conclude this is a response to the energy shock rather than simply a weak month after two positive ones, but the former is clearly a risk.

Slippage of 1.2% in mining needs to be seen alongside a 2.1% increase in February and mining is likely to be lifted if oil prices remain firm. Utilities fell by 2.3% after a 1.8% February increase. This is likely to reflect improved weather after a February that included a very cold spell.

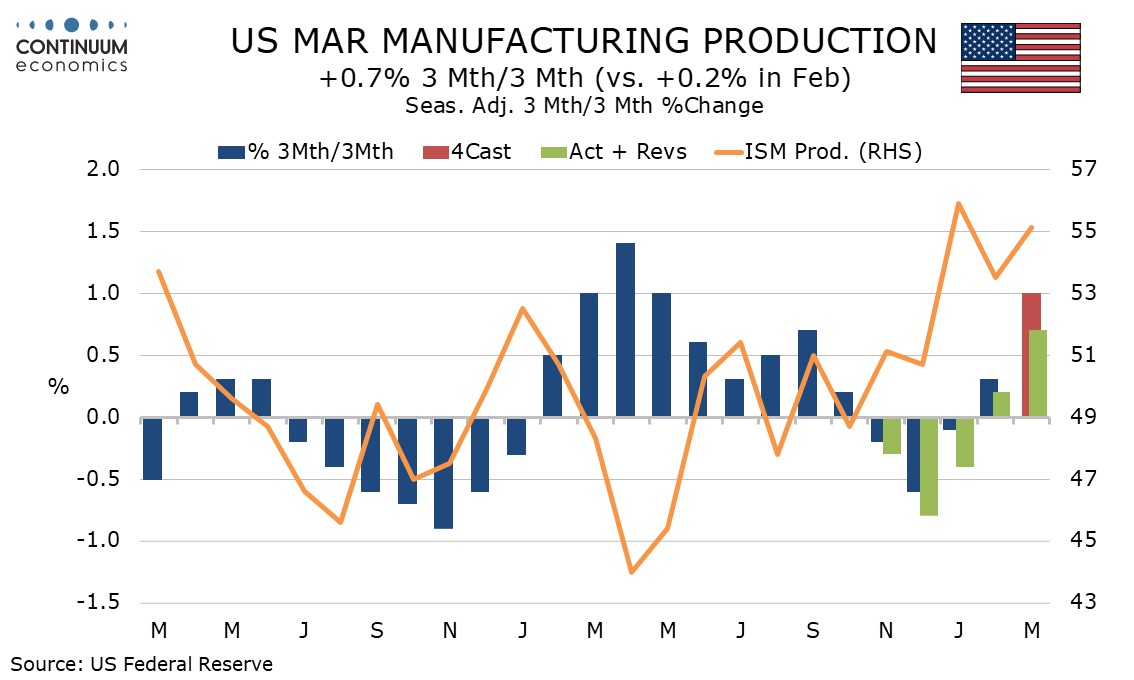

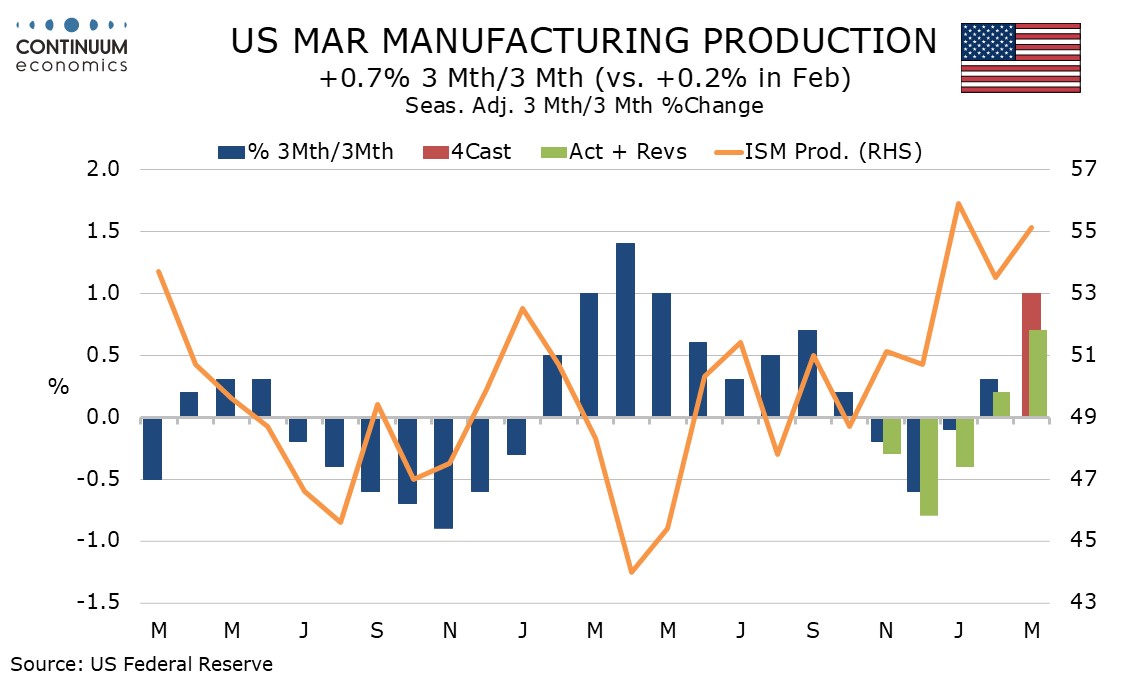

Manufacturing was hit by a sharp decline in autos after three straight gains. Manufacturing ex autos rose by 0.1% after gains of 0.2% in February and 0.5% in January.

Manufacturing output increased by 3.0% annualized in Q1 after a 3.2% decline in Q4 which was the only negative quarter in 2025. Overall industrial production rose by 2.5% after a 1.7% decline in Q1. Quarterly data gives some backing to improved ISM data, but is less improved than the ISM’s.