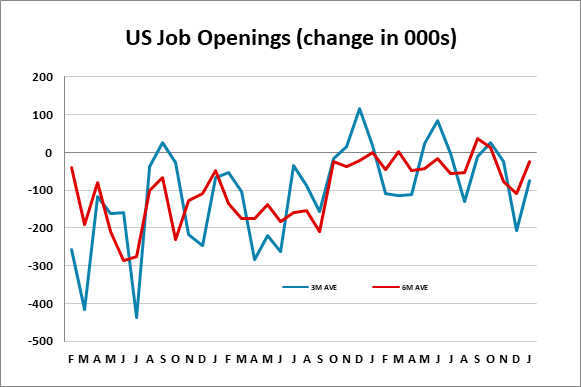

U.S. March Preliminary Michigan CSI - Limited impact from Iran, January Job Openings correct higher

The preliminary March Michigan CSI does not suggest much impact from the Middle East conflict yet, but the final March report may be a different story. A rise in January job openings looks corrective from two straight declines.

The Michigan CSI at 55.5 from 56.6 is slightly weaker though still stronger than each month in Q4 2025.

The present situation increased to 57.8 from 56.6 but expectations slipped to 54.1 from 56.6. This mix hints at worries over the future but if it was due to Iran, one would expect price expectations to bounce. In fact the 1-year view was unchanged at 3.4% and the 5-10 year view slipped to 3.2% from 3.3%.

January job openings increased by 396k to 6.946m. This looks corrective from declines of 296k in December and 324k in November. The 3-month average is -65k and the 6-month average -24k, both suggesting only a modest labor market weakening.

Hirings rose by 22k but separations fell by 98k, showing the strong January payroll was due more to fewer separations than stronger hirings. The fall in separations was led by a fall of 88k in quits, which is not a positive sign. January’s stronger payroll was followed by a weaker one in February.