U.S. March Durable Goods Orders, Advance Goods Trade, Housing Starts and Permits - More positives than negatives

The latest US data is mixed though with more positives than negatives, implying the economy entered the oil shock with solid momentum. The data does not suggest any major revisions to expectations for tomorrow’s Q1 GDP release are needed, though any revisions are likely to be modestly upwards.

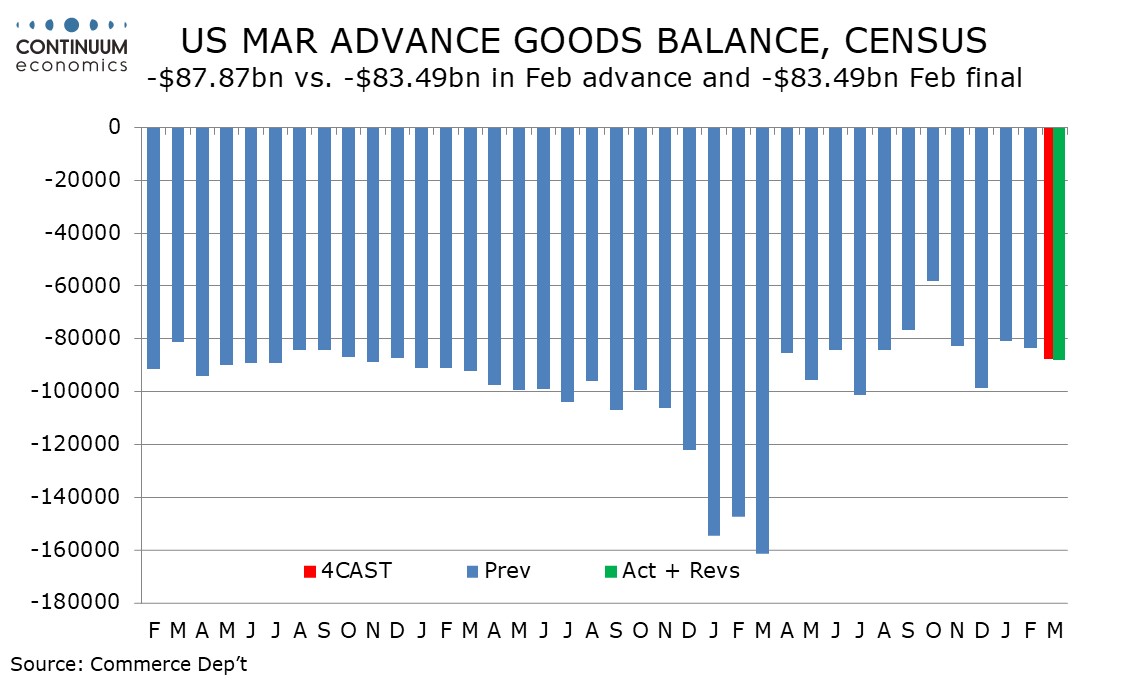

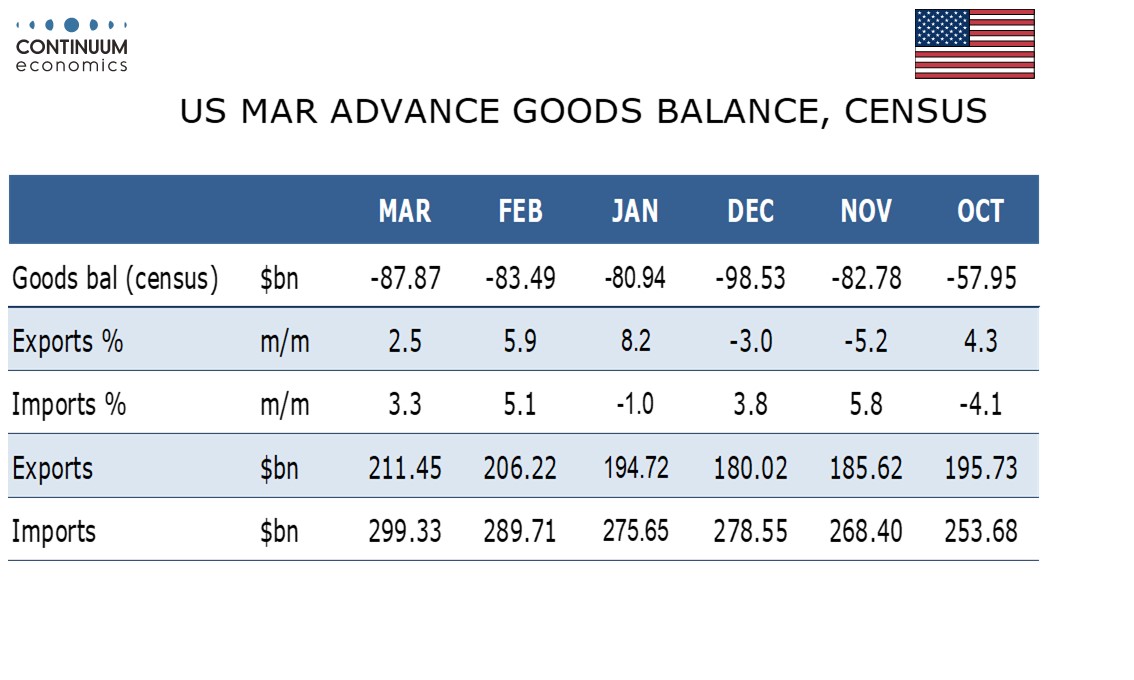

The advance goods trade deficit of $87.9bn is up from $83.5bn in February but only marginally wider than the market consensus. The average deficit in Q1 is $84.1bn, a modest deterioration from Q4’s $79.8bn.

Detail is positive with exports up by 2.5% and imports up by 3.3%, both extending gains in excess of 5.0% in February. Exports were strong in most categories with a notable exception from consumer goods. Autos were particularly strong in a broad based imports increase.

Advance March inventory data was strong, wholesale up by 1.4% and retail up by 0.7% though prices will have exaggerated the gains, particularly wholesale. Retail saw strength in autos. Advance March durable manufacturing goods inventories were however subdued, up only 0.2%.

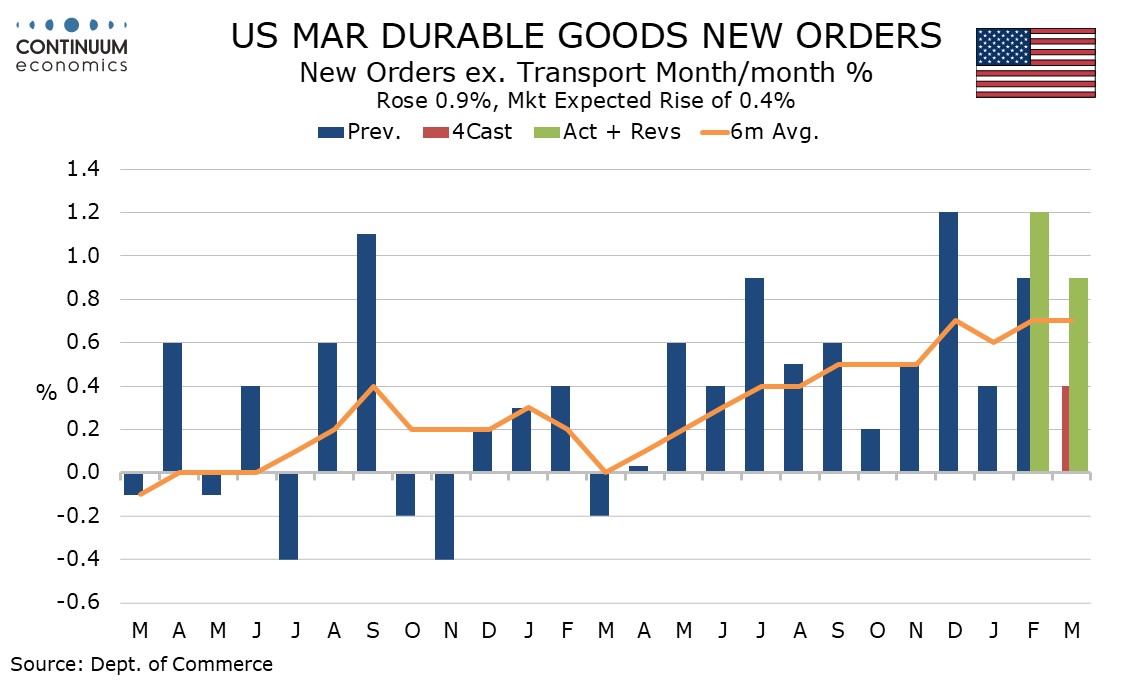

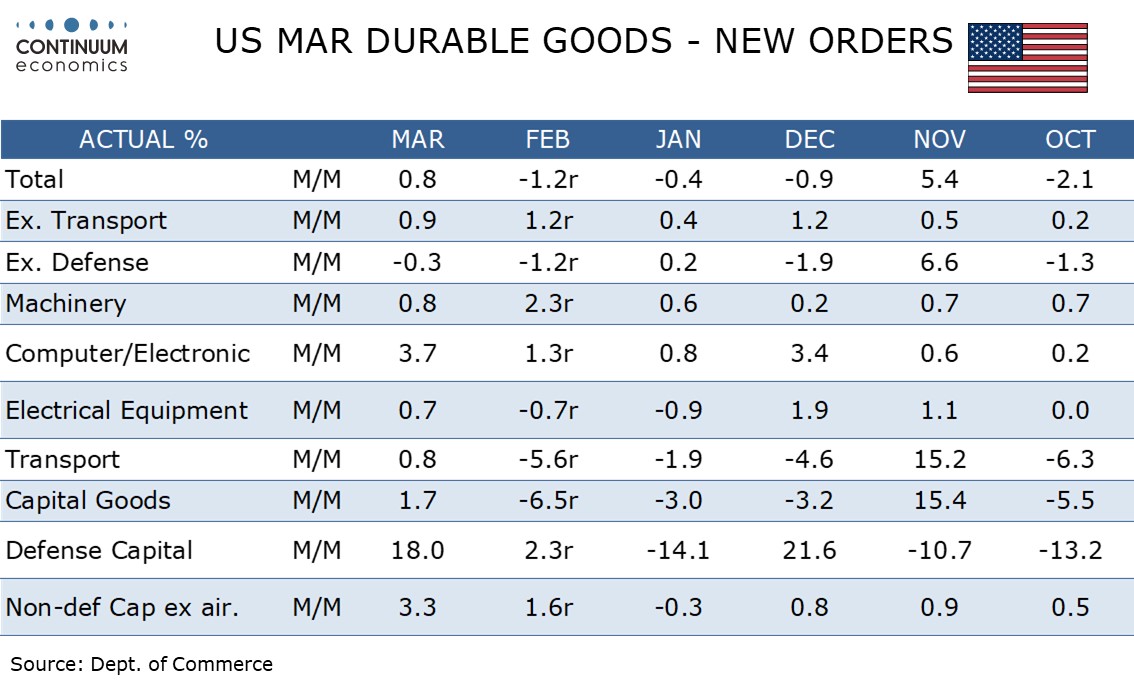

March durable goods orders with gains of 0.8% overall and 0.9% ex transport were on the firm side of ex[actins but ex defense an unexpected decline of 0.3% was seen. Depletion of ammunition in the Middle East conflict will continue to support defense orders.

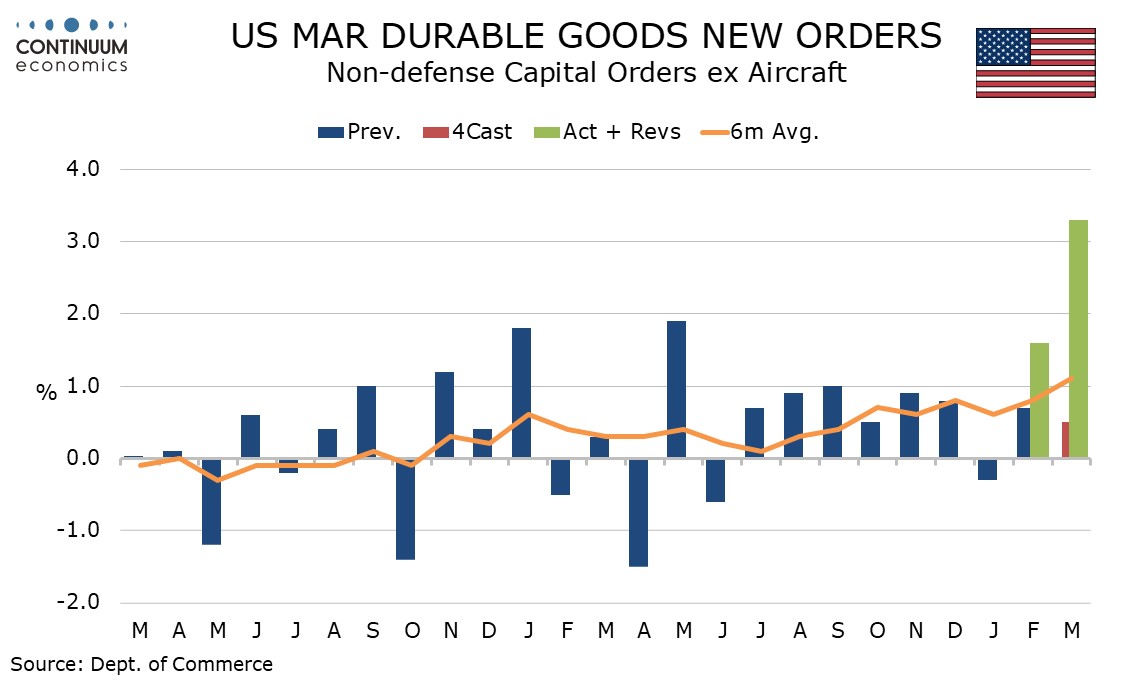

Within the transport breakdown autos and defense aircraft were stronger but non-defense aircraft slipped. Non-defense capital orders ex aircraft were very strong with a rise of 3.3%, suggesting a continued positive business investment outlook. Shipments in the latter sector rose by 1.2%, which is supportive for GDP.

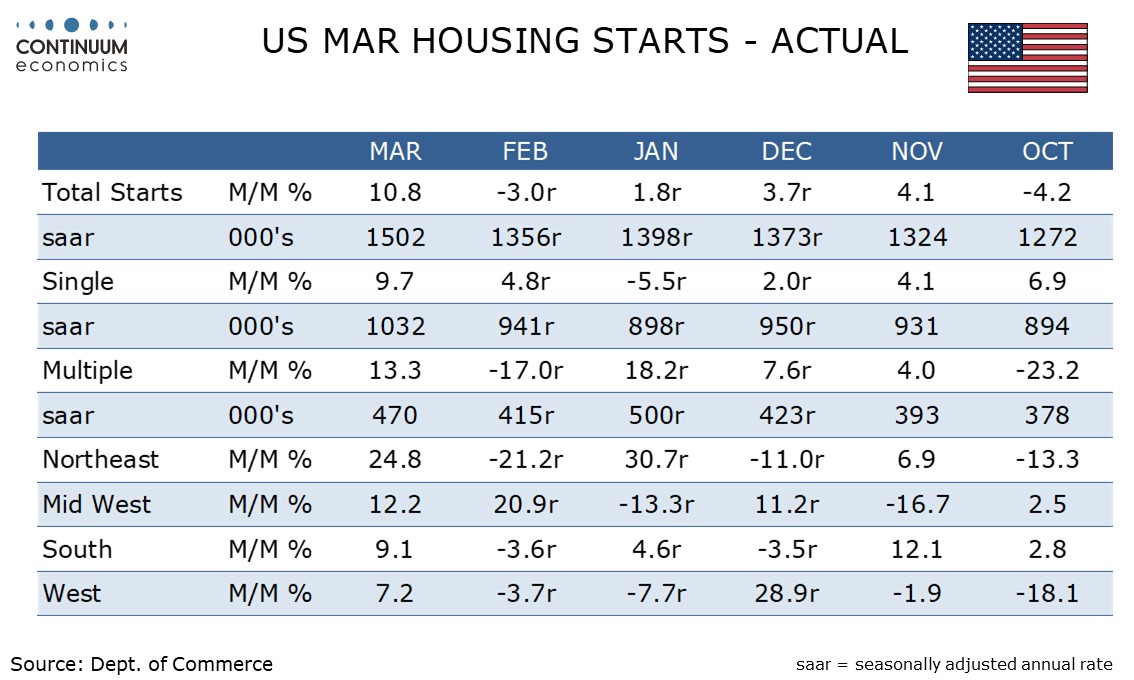

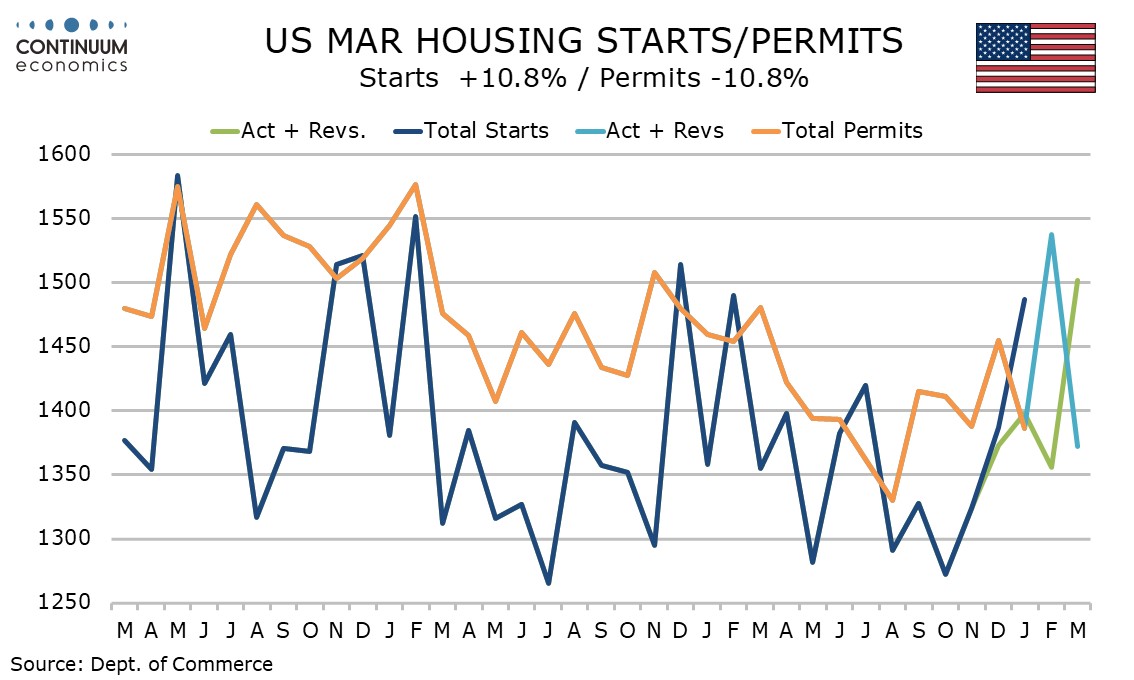

Housing starts and permits were released for both February and March, starts saw a modest 3.0% decline in February but rebounded by 10.8% in March to 1.502m, the highest since December 2024. The strength in starts was led by the single family sector, with February’s dip entirely due to multiples.

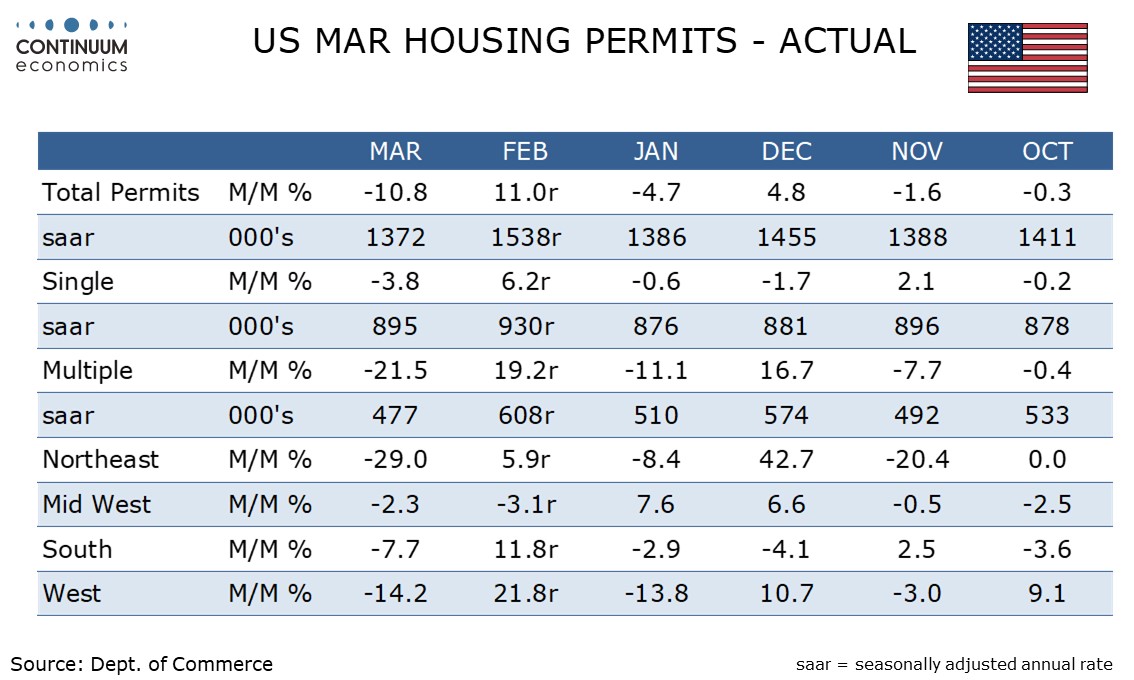

Permits saw a strong 11.0% increase in February to 1.538m, the highest since February 2024, before a 10.8% reversal in March to 1.372m. Multiples led the February gain but more than fully reversed in March, while singles saw only a partial reversal, falling by 3.8% in March after a 6.2% February rise.

The housing sector data is on balance positive but the March reversal in permits suggest March’s strength in starts will be difficult to sustain. Some housing sector surveys, notably the NAHB’s, have been losing what had been positive momentum entering 2026 in recent releases, as Fed easing hopes get pushed back.