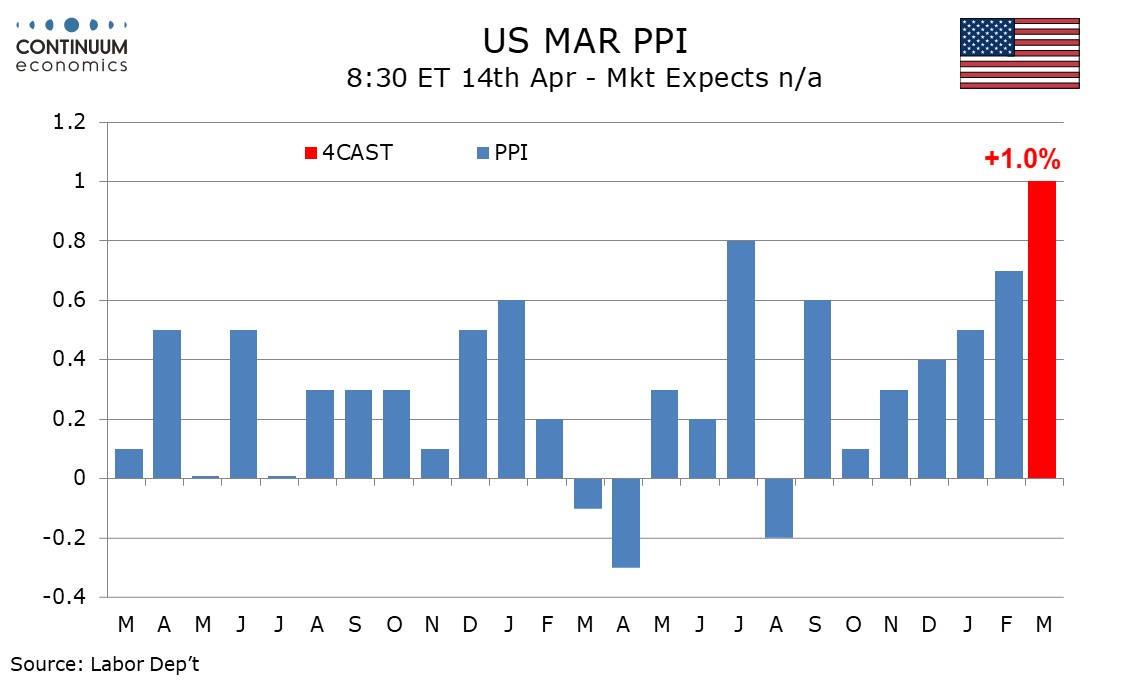

Preview: Due April 14 - U.S. March PPI - Strongest since March 2022

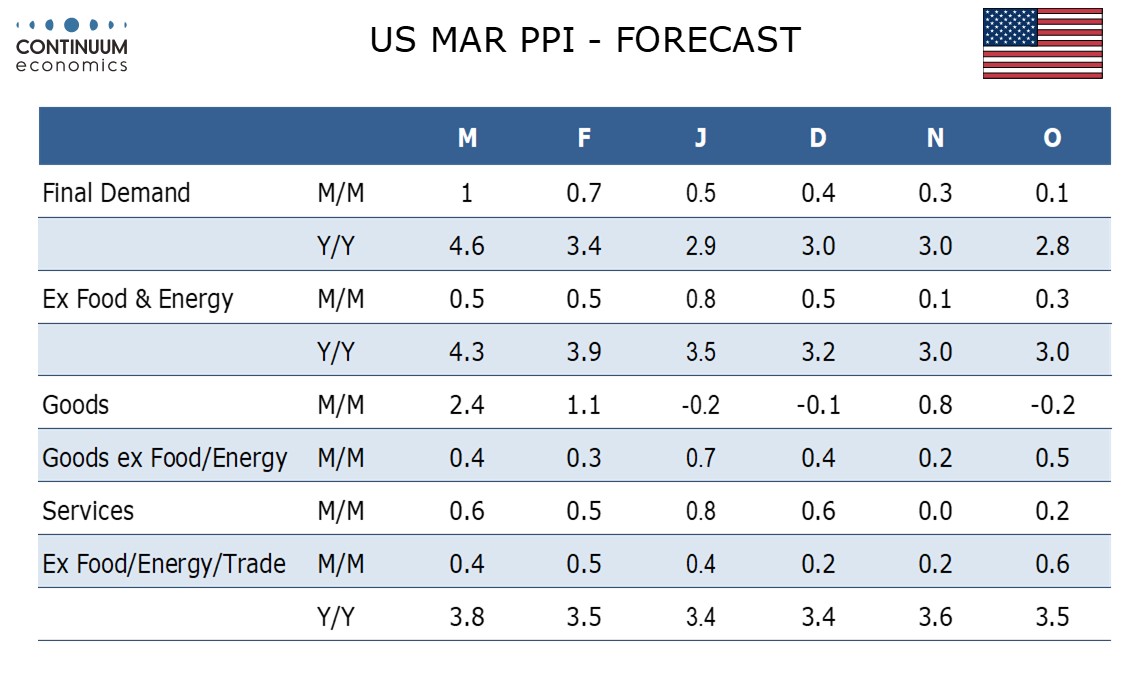

We expect PPI to rise by 1.0% in March, which would be the strongest rise since March 2022. The rise will be led by energy, though the core rates ex food and energy at 0.5% and ex food, energy and trade at 0.4% are likely to maintain a recent acceleration.

We expect a strong 10.0% increase in energy even if price gains late in March are not fully captured. We expect a 0.8% increase in food to follow a strong 2.4% increase in February that reversed weakness seen in Q4 and January. The situation in the Middle East poses upside risks for food as fertilizer supplies are disrupted but impact in March is likely to be limited.

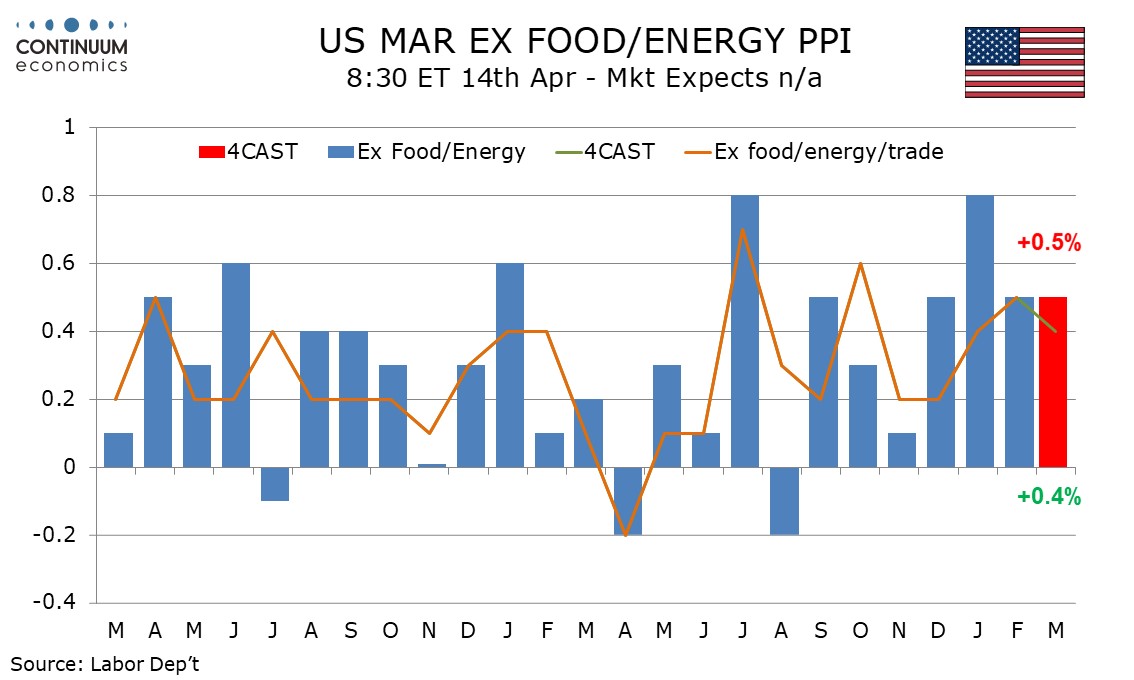

March 2022 after the Russian invasion of Ukraine saw some acceleration in core PPI suggesting upside risk in series that have already been showing worrying signs of acceleration in January and February. We expect PPI ex food and energy to rise by 0.5%, matching gains seen in December and February but slower than January’s 0.8%, while ex food, energy and trade rises by 0.4%, slower than February’s 0.5% but matching January. We expect goods ex food and energy to rise by 0.4% and services to rise by 0.6%, the latter led by transport and warehousing.

Yr/yr growth would then increase to 4.6% overall from 3.4% in February, with the ex food and energy rate at 4.3% from 3.9% and ex food, energy and trade at 3.8% from 3.5%. All three series would be at their strongest pace since February 2023, rates that were still inflated by the impact of the Russian invasion of Ukraine.