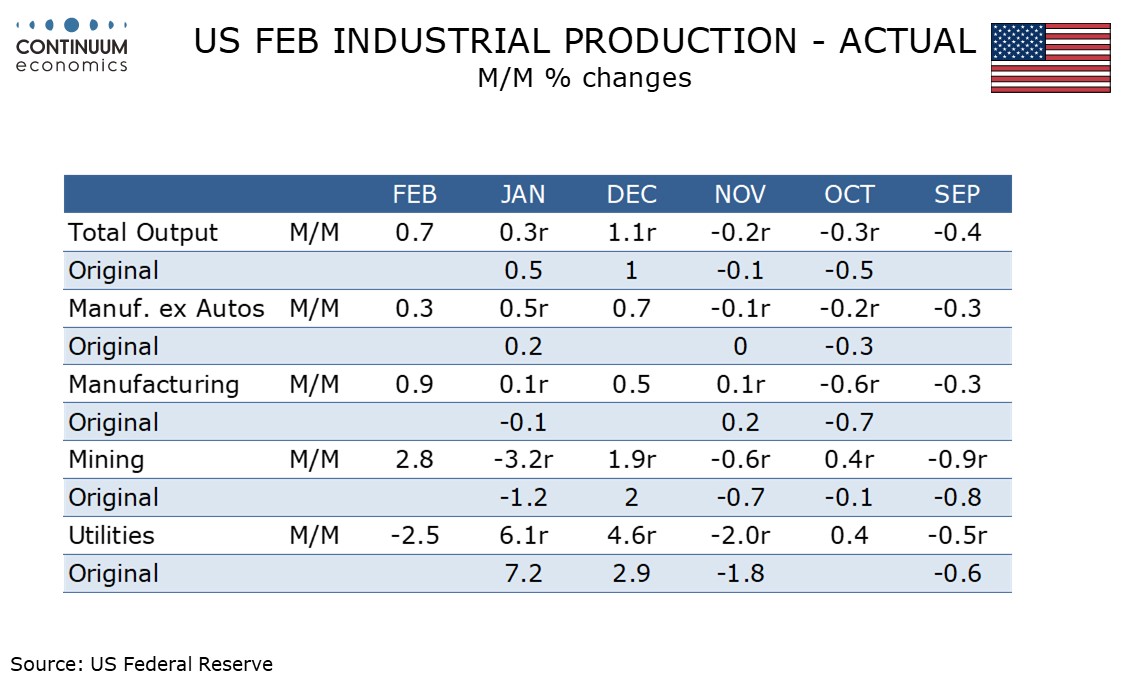

U.S. February Industrial Production - Autos led, but some underlying improvement

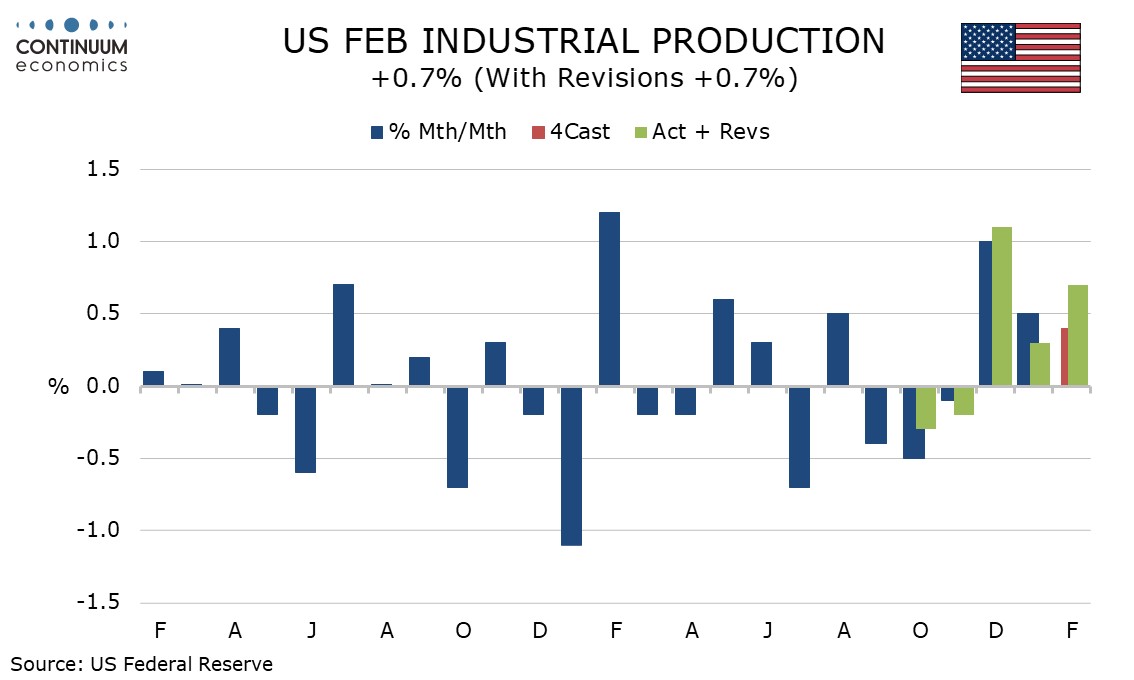

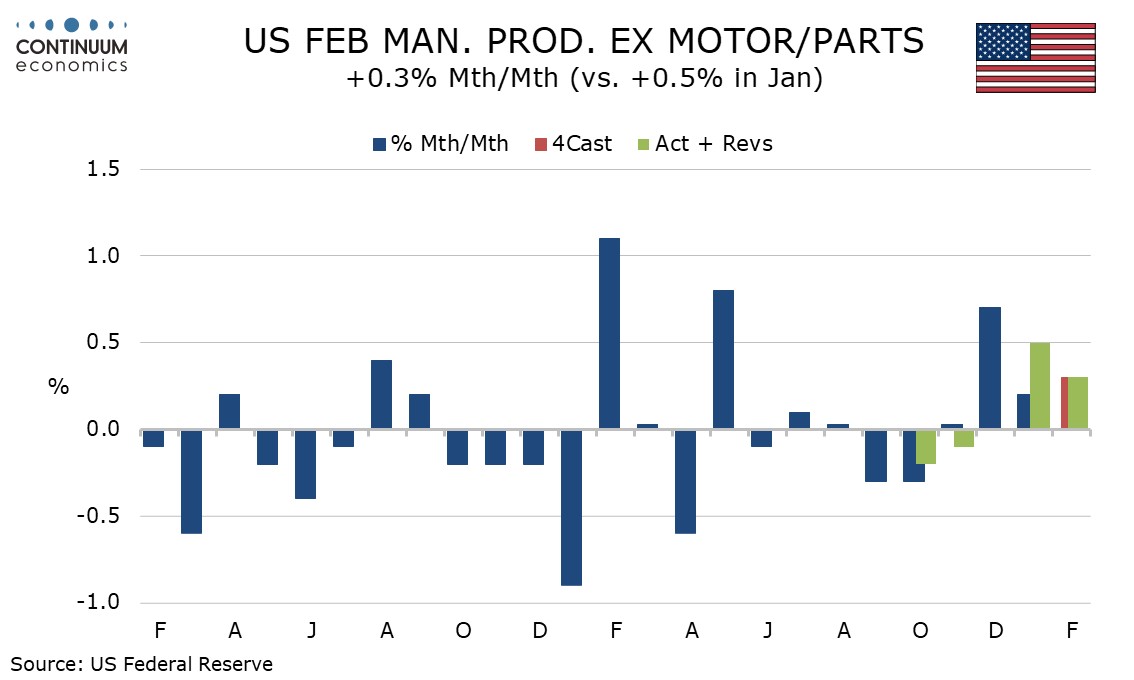

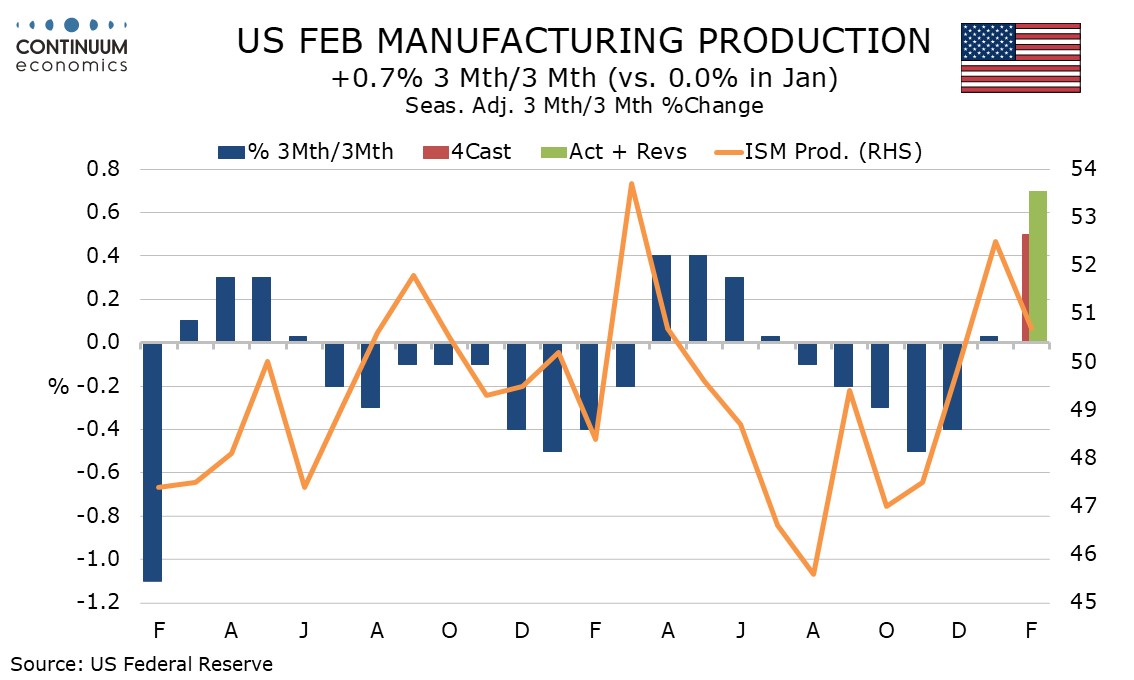

February industrial production has seen a stronger than expected 0.7% rise overall with an even more impressive 0.9% rise in manufacturing. Manufacturing ex autos was less impressive up by 0.3%, though this still means three straight gains.

Mining rose by 2.8% after a 3.2% December decline but utilities slipped by 2.5% after a 6.1% January increase. These numbers reflect more normal weather conditions after January saw weather hurt mining but lift utilities.

Auto output surged by 8.5% after a 5.3% January decline. January’s drop may have been influenced by weather while February’s gain may have been supported by a despite to beat expected tariffs on components coming from Canada and Mexico.

Aerospace and miscellaneous transport rise by 2.1%, a third straight strong gain but less than in December and January with Boeing’s recovery from a stroke largely complete.

There has been some improvement in underlying trend recently which has coincided with improvements in most manufacturing surveys, with the ISM manufacturing index moving above 50 in January and February. Still, February’s data was less strong that January’s and the net impact of a trade war is likely to be negative in the coming months.