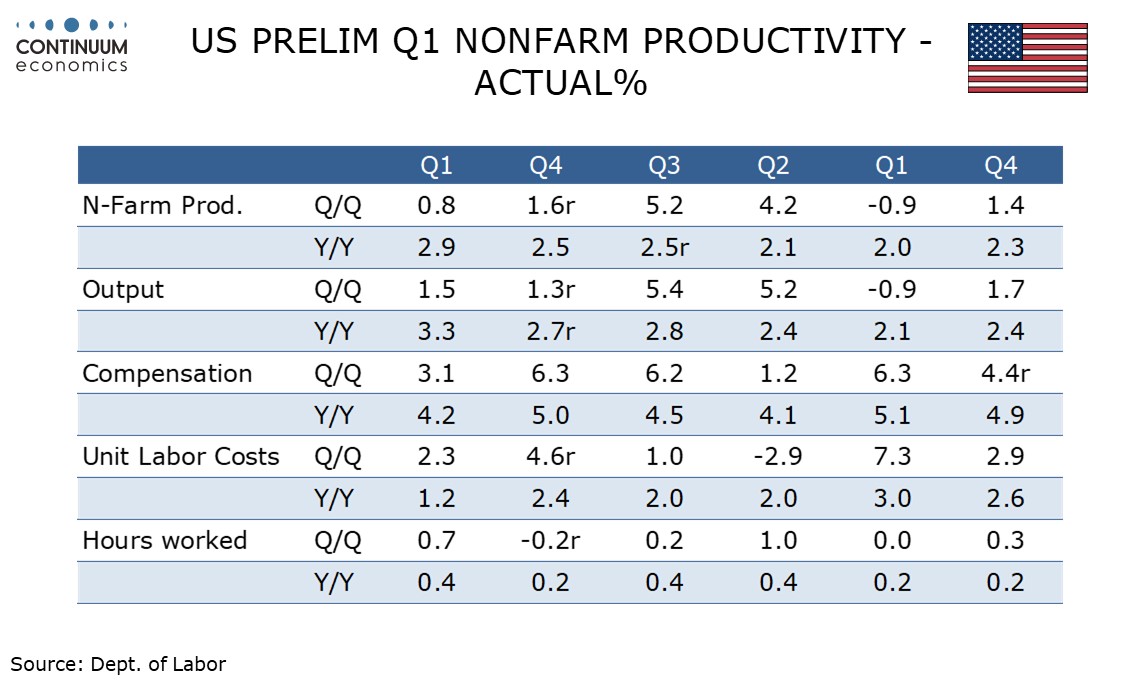

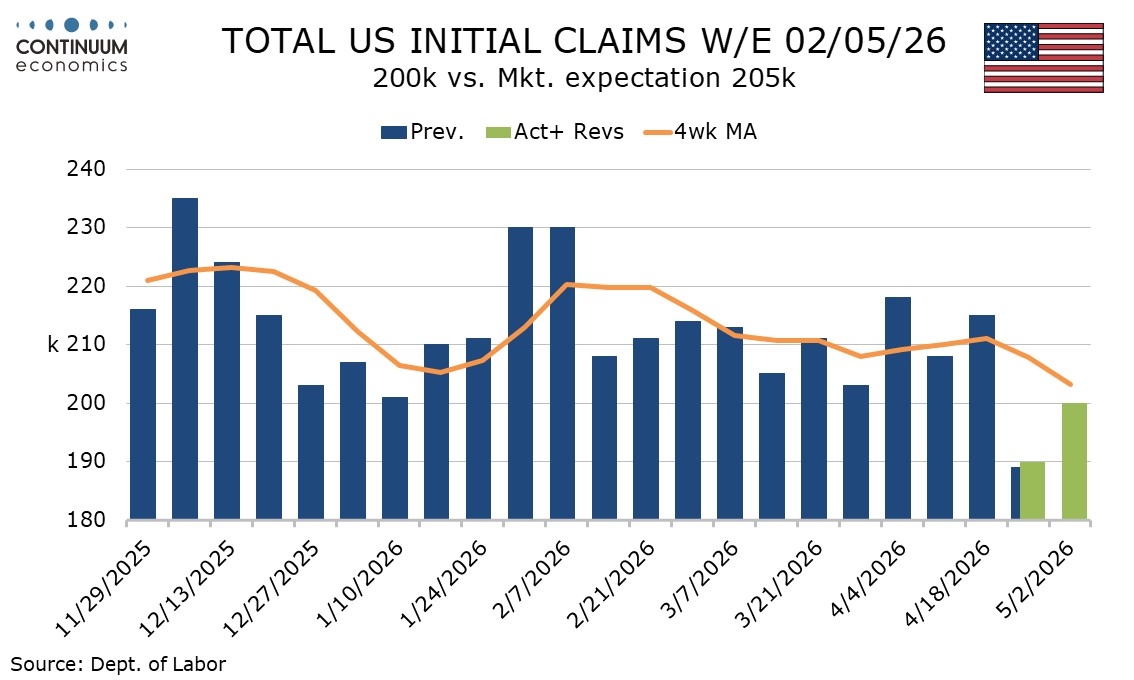

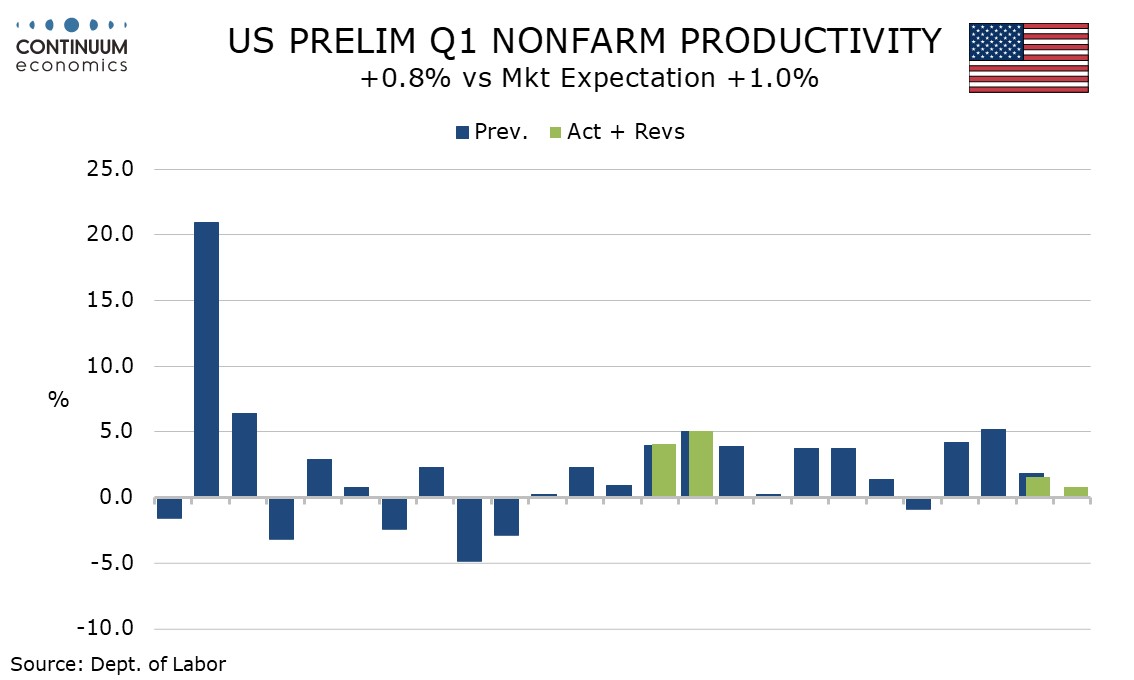

U.S. Initial Claims still very low, Q1 Productivity and Costs report shows strength in non-labor costs

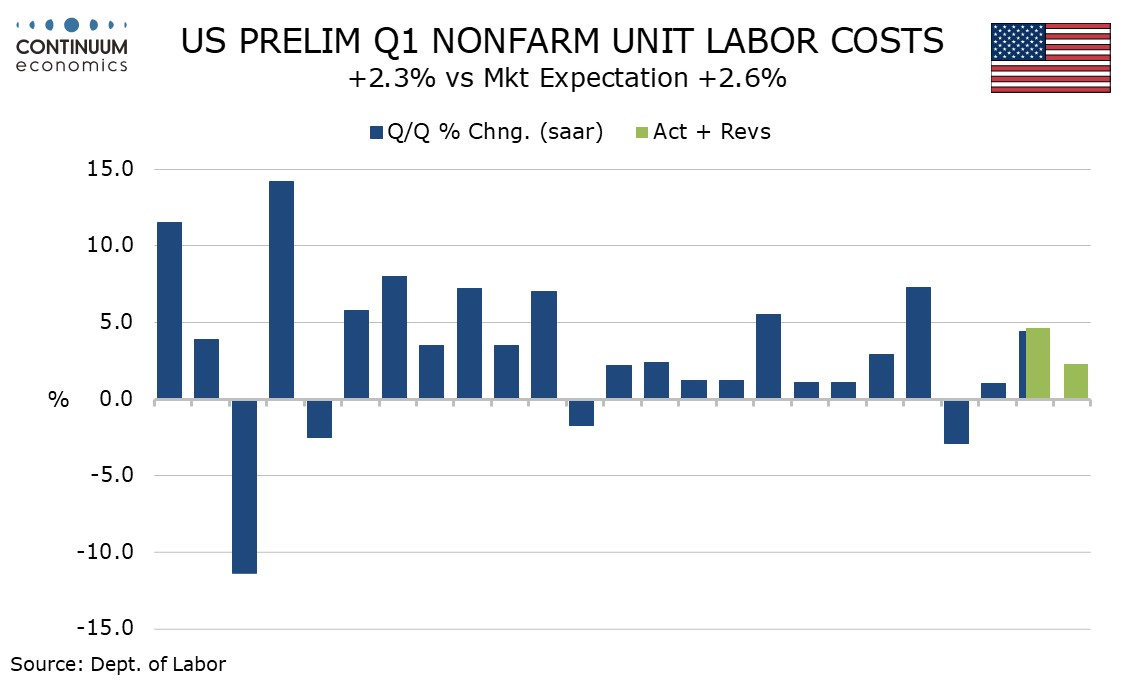

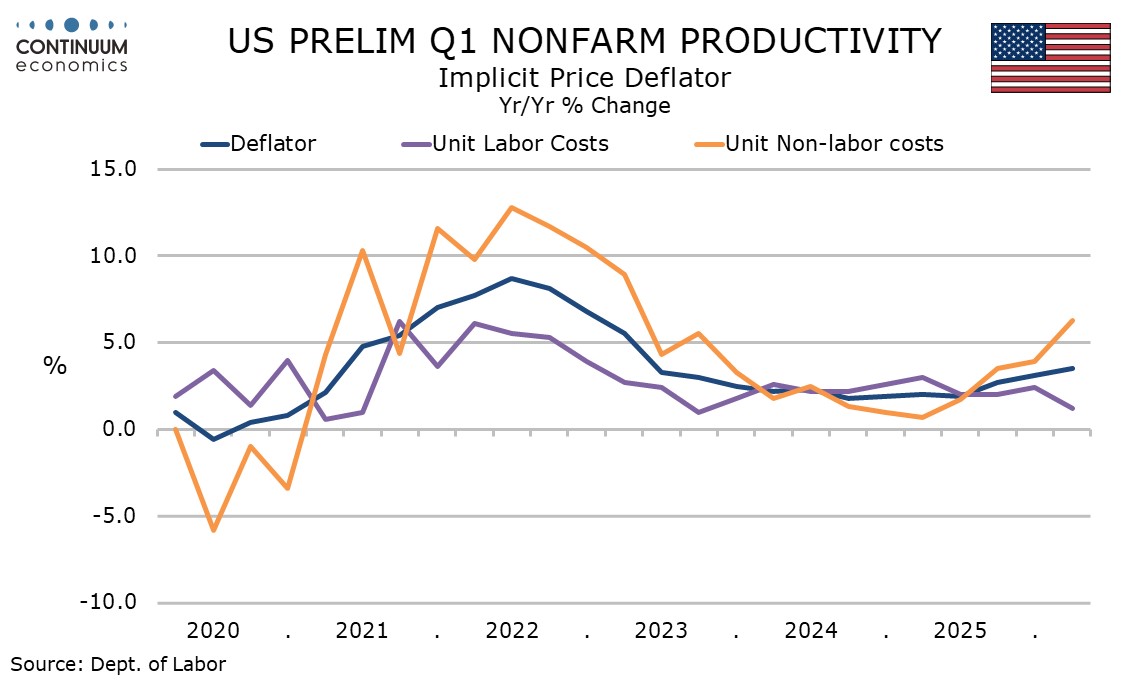

Initial claims at 200k are up from last week’s exceptionally low 190k but still consistent with layoffs running at veery low levels. Q1 non-farm productivity at 0.8% is marginally below consensus and unit labor costs at 2.3% more significantly so but non-labor costs saw a strong 8.0% increase which suggests inflationary concerns are justified.

Before last week initial claims had not fallen below 200k since January 2024 so this week’s number is still very low. The survey week for April’s non-farm payroll however came two weeks ago, though even two weeks ago initial claims were looking subdued.

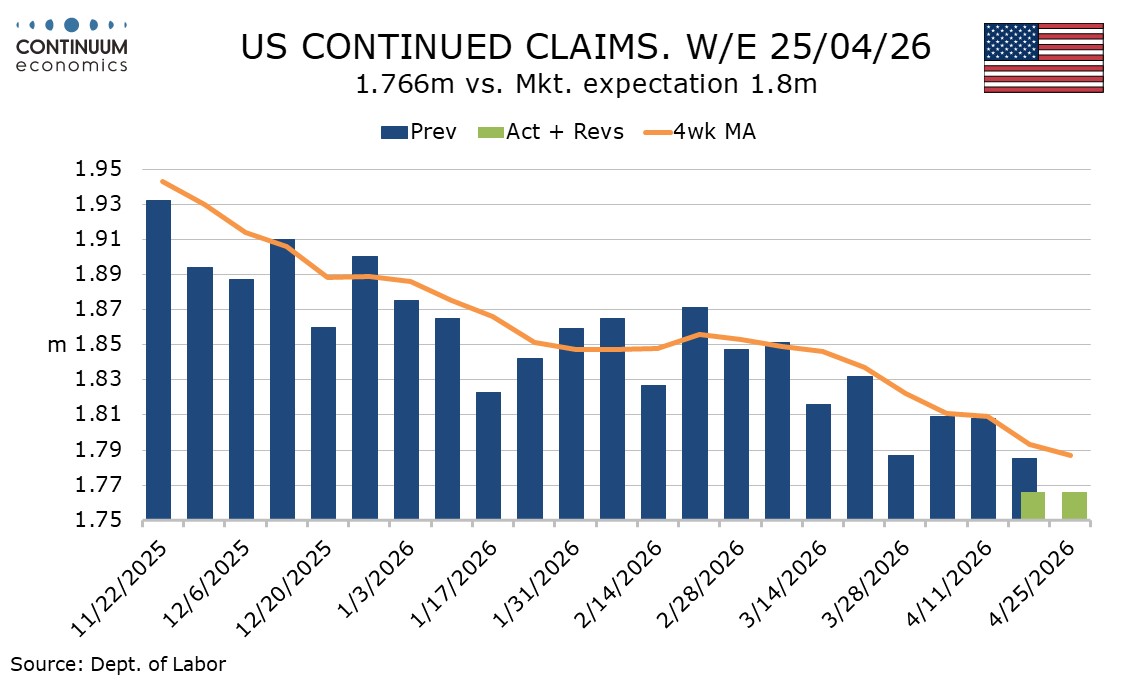

Continued claims at 1.766m were unchanged and lower than expected, with last week revised down from 1.785m, and that covers the survey week for April’s payroll. The level is the lowest since June 2023.

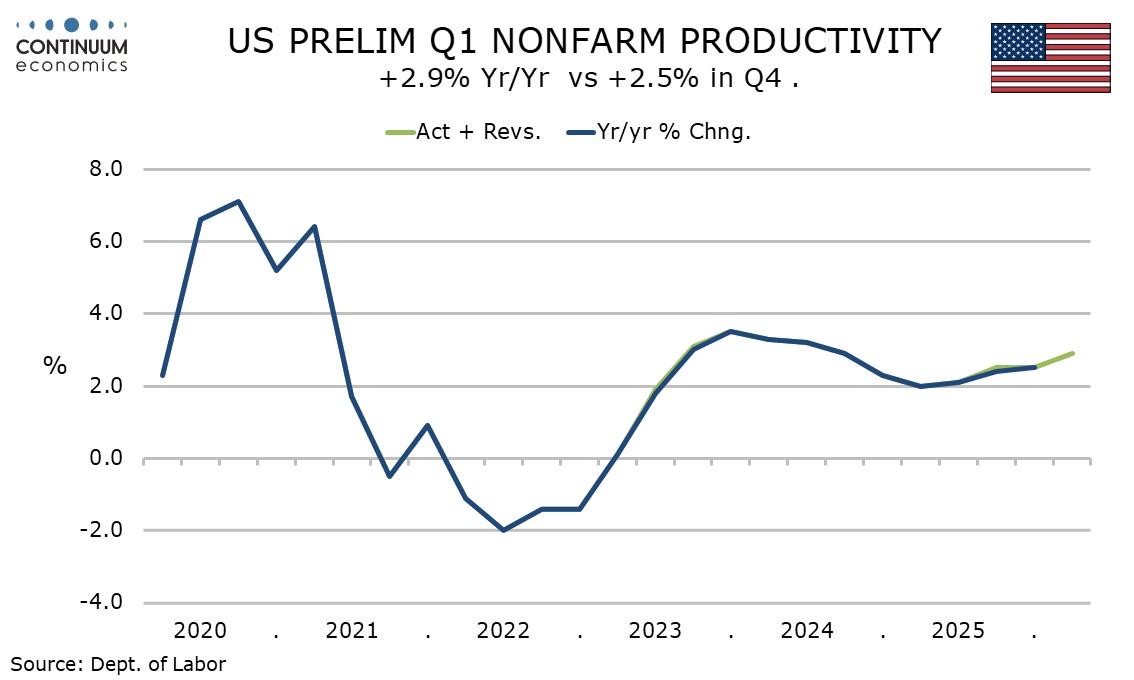

Q1 non-farm productivity with a 0.8% increase comes from a 1.5% increase in non-farm business output (similar to 1.3% in Q4, not influenced by swings in government that were seen in GDP data) and a 0.7% increase in aggregate hours worked.

The modest productivity gain tempers optimism about AI bringing a productivity surge that will allow stronger non-inflationary growth somewhat, though yr/yr growth at 2.9% is firm and at a 6-quarter high.

Compensation costs slowed to 3.1% after two straight quarters above 6.0% and that restrained unit labor costs to a modest 2.3% rise.

However non-labor costs at 8.0% were strong causing the implicit deflator to rise by 4.9%, the strongest since Q2 2022 in the aftermath of the invasion of Ukraine. There is probably more to come in Q2 from non-labor costs.

The yr/yr implicit deflator has accelerated to 3.5% from 3.1% in Q4. This series ran below 2.0% from Q3 2024 through Q2 2025. At that point optimism on returning core inflation to the 2.0% target looked justified. It no longer is.