FX Daily Strategy: Europe, July 5th

US employment report the main market focus

Some mild USD downside risks seen

EUR has upside scope despite soft data

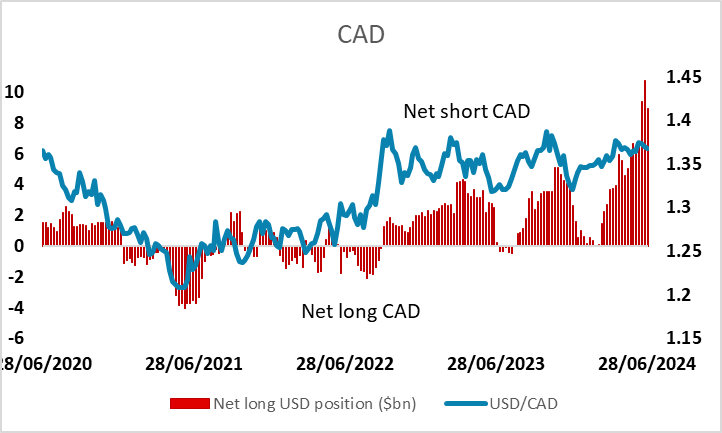

CAD may have the biggest scope for gains given positioning

US employment report the main market focus

Some mild USD downside risks seen

EUR has upside scope despite soft data

CAD may have the biggest scope for gains given positioning

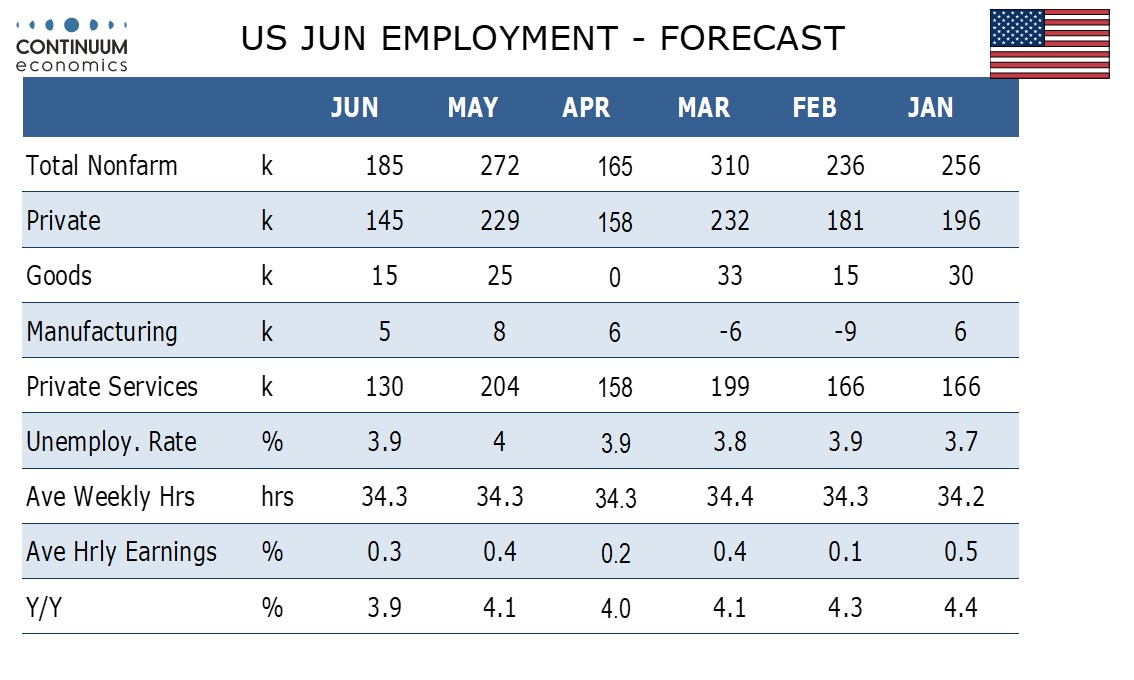

The US employment report will be the prime focus on Friday. We expect June’s non-farm payroll to hint at some loss of labor market momentum, with a 185k increase overall and 145k in the private sector, the latter the slowest since October 2023. We expect average hourly earnings to follow a strong 0.4% May increase with a rise of 0.3% and less before rounding, though we expect unemployment to reverse a May increase to 4.0% and fall back to 3.9%. Our forecasts are broadly in line with the market consensus, which is slightly higher for the payroll number but in line for earnings and looks for an unchanged 4.0% unemployment rate. We therefore aren’t looking for a big reaction, but the data is consistent with slowdown, and the softer numbers this week on ISM and claims on top of the more dovish Powell comments suggests that the risks are biased towards lower yields and a lower USD.

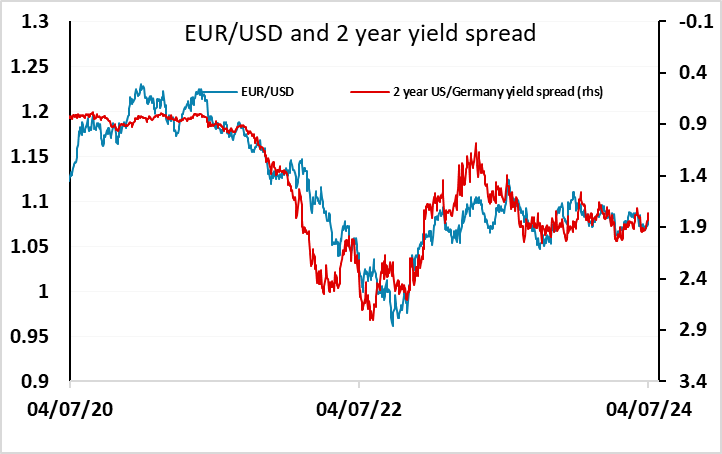

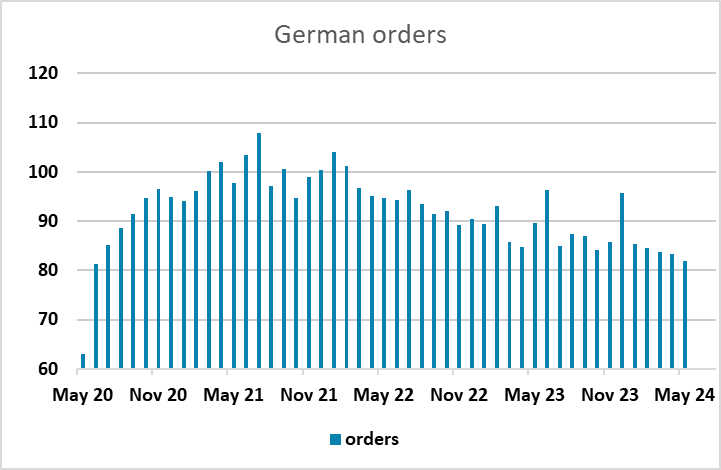

The USD was somewhat softer on Thursday, falling back across the board, with not much movement on the crosses. The market paid little attention to the weak German manufacturing orders data, but the numbers were clearly weak, with orders at the lowest level since the pandemic, and excluding the pandemic, the lowest since 2012. While the marginally stronger than expected core CPI data in June has helped to reduce market expectations of an ECB rate cut in July to around a 33% chance, the weakness in the manufacturing and construction sectors and in money and credit suggests there is scope for earlier and larger ECB easing than the market is pricing in. Nevertheless, current yield spreads suggest there is scope for some further gains in EUR/USD provided the US employment data is not surprisingly strong.

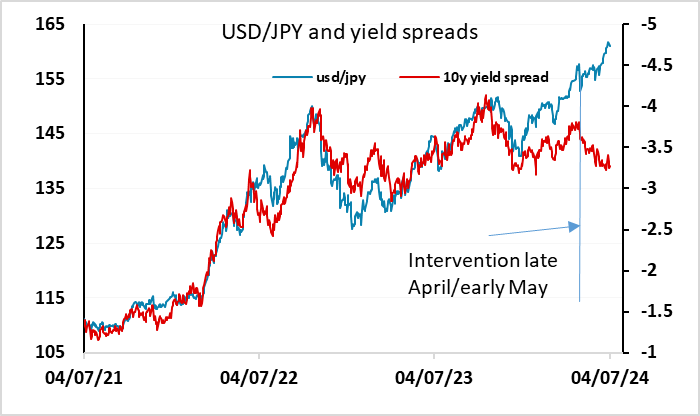

The JPY also managed to recover a little on Thursday, albeit mainly against the USD with most crosses not much changed, although GBP/JPY did break its record 13 day run of gains. Even so, JPY sentiment remains generally negative in the absence of intervention, despite yield spreads having moved substantially in the JPY’s favour this year and the JPY hitting all time lows in real terms this week. It seems that the Japanese authorities are unwilling to commit to further intervention at this stage, perhaps because they are not convinced that inflation is back up to target levels or perhaps simply because the last round proved ineffective except in the short term. We suspect intervention would be successful in the longer run if Japan was supported by the US and others, even if only with token intervention, but at this stage it seems such action is unlikely to be forthcoming. Even so, all the fundamental factors are in place for a JPY recovery, so even intervention from Japan alone might prove successful. But in the absence of intervention we may see JPY gains against the USD if the employment report is weak, but it is unlikely we will see gains on the crosses.

Friday also sees the Canadian employment report, and the CAD has plenty of potential to gain against the USD given the extreme positioning evident from the CFTC data on IMM speculative positioning. Against this, yield spreads have been favouring the USD in recent weeks, but have moved in the CAD’s favour of late. A weak US report and a strong Canadian report could see a sharp USD/CAD move lower to below 1.35.

Net speculative positions on the IMM