FX Weekly Strategy: June 17th-21st

French political picture in focus as risk sentiment suffers

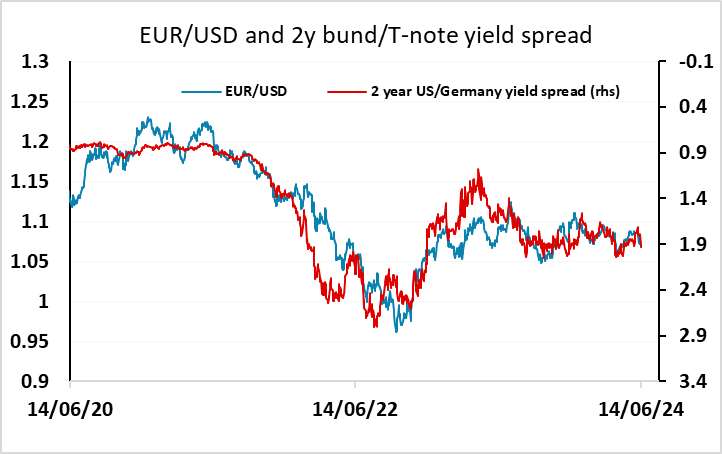

EUR likely to remain under pressure

Some downside risks for GBP on MPC meeting

PMIs look like the most important data

Strategy for the week ahead

Last week, for the first time in a while, the market was driven less by central bank expectations and yield moves and more by political and fiscal concerns, at least as far as the EUR was concerned. Uncertainty around the impact of the French parliamentary election drove the EUR lower on a broad front, with EUR/USD hitting its lowest since May 1 and EUR/CHF at its lowest since February. The market concerns centre on the possibility of the populist right wing RN party gaining control and enacting policies involving billions in unfunded spending. RN gained the largest vote in the European elections and is currently polling around 33%. However, the two round system used in the French elections makes it harder for RN to gain a controlling number of seats. There is also the left-green alliance, which has agreed to field only one candidate between them per constituency. Together they are polling around 30%. Macron’s Renaissance party currently have the largest number of seats but are only polling at 19%. The electoral system makes the result hard to predict, but it looks unlikely that any party will achieve a majority. It may also be that there is no feasible alliance that can command a majority. So a mess may be the most likely outcome, which may not be ideal, but it may prevent any radical policies being pushed through. The market will be focused on any polls in the coming week, and any evidence of a drift towards RN could be expected to undermine the EUR, while a recovery for Macron’s Renaissance would be EUR positive. But with the election process not ending until July 7, the EUR may be in for a period of struggle, underperforming the levels suggested by yield spreads.

The main calendar events of the week are the UK CPI data and the UK MPC meeting. Our forecast for CPI is broadly in line with the market consensus of a drop to 2.0% in the headline CPI and 3.5% in the core, so the impact on GBP should be modest. The market expects no change in policy at the MPC meeting, but we see a cut as an outside chance with inflation back at target and sclear evidence of weakening in the labour market. But if there is no change in policy the market will be focused on how many votes there are for a cut and whether the statement and press conference suggest a cut in August is likely. Currently, the chances of a cut this month are priced at less than 10% while an August cut is priced as a 44% chance. We see scope for that to become a probability rather than a possibility after the meeting, suggesting downside risks for GBP.

However, EUR/GBP will probably be driven as much by the EUR as GBP, so GBP bears would probably be better focus on other pairs. GBP/JPY and GBP/NOK would probably be our choices for GBP bears, with both the NOK and JPY looking cheap relative to yield spreads. However, the NOK would likely suffer if risk sentiment continues to weaken, while the JPY would likely benefit.

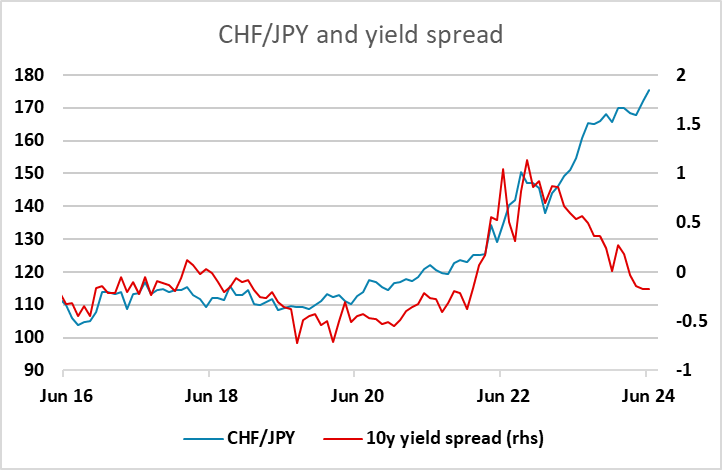

We expect the SNB to cut rates another 25bps to 1.25%, and this is also the market expectation. The SNB were the first to cut rates, and this initially had a negative impact on the currency, but rate spreads have not typically had mush impact on the CHF, and while they are likely to cut again this week, it is expected and they will in the end be easing less than the ECB and others. The CHF picture is likely to be determined more by sentiment around the French election than the SNB decision, although we would note that another rate cut would strengthen the case for the CHF to be usurped as the preferred safe haven by the JPY – a case that is already strong with CHF/JPY up more than 50% in the last few years and at all time highs.

Last week saw the JPY suffer after the BoJ decided not to change policy at this month’s meeting, leaving the potential for a rate hike and a big reduction in JGB buying for the July meeting. But after the initial dip following the meeting, the JPY managed a recovery as risk sentiment weakened due to the concerns around French politics. Risk sentiment is likely to be key for the JPY this week, so developments on the French political front will be watched carefully. The other main focus will be the preliminary S&P PMI indices, which showed strength in May but are expected to correct lower in June. These are not due until Friday, so the more negative risk tone seen at the end of the last week may initially persist, supporting the JPY.

Data and events for the week ahead

USA

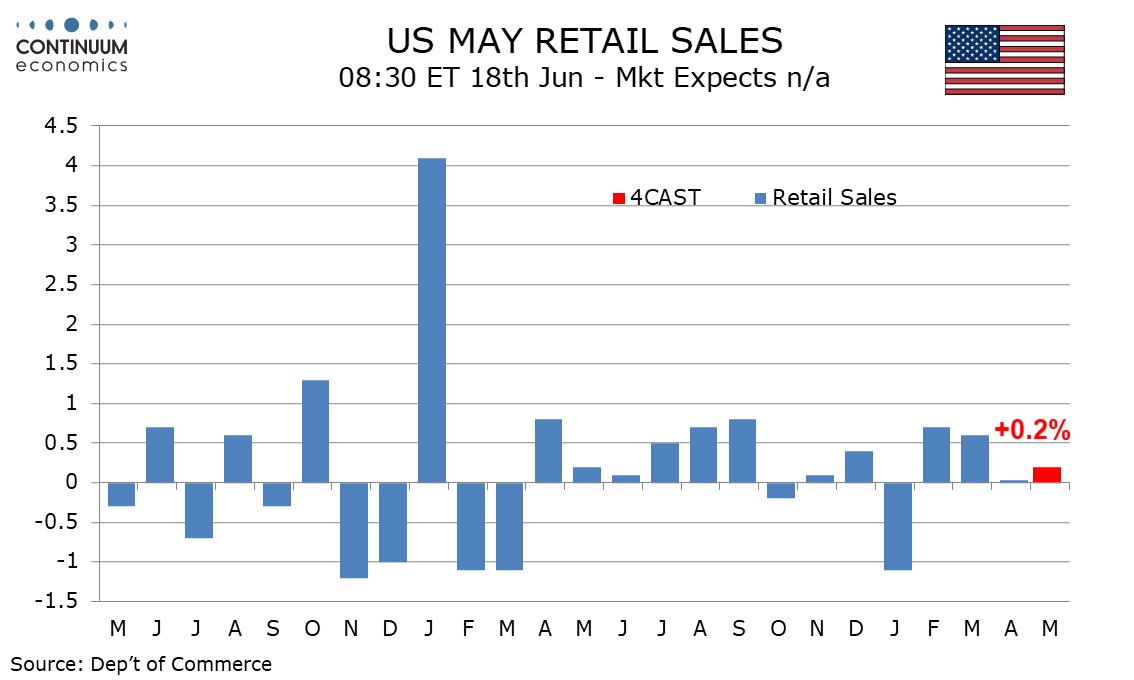

On Monday the June Empire State manufacturing survey is due and Fed’s Harker will speak. The week’s most significant release is May retail sales on Tuesday. We expect modest gains of 0.2% overall, 0.1% ex autos and 0.3% ex autos and gasoline. Later we expect a rise of 0.5% in May industrial production, with manufacturing up by 0.3%. Existing data implies a 0.3% rise in April’s business inventories report. Fed speakers on Tuesday include Logan, Kugler, Musalem and Goolsbee. Wednesday sees the Juneteenth holiday but June’s NAHB homebuilders’ survey will be released.

On Thursday initial claims will be closely watched after a preceding sharp increase. At the same time we expect May housing starts to rise by 0.7% to 1370k, permits to be unchanged at 1440k, and Q1’s current account deficit to increase to $207.0bn from $194.8bn. June’s Philly Fed manufacturing survey is also due while Fed’s Barkin will speak on Thursday. On Friday we expect June’s S and P PMIs to correct lower from stronger May data, manufacturing to 50.0 from 51.3 and services to 53.0 from 54.8. Also scheduled are May existing home sales, where we expect a 3.4% fall to 4.00m, and May’s leading indicator.

Canada

In Canada Monday sees May housing starts and existing home sales data. On Wednesday minutes from the June 5 Bank of Canada meeting will be released. If the decision to ease at the meeting turns out to have seen some debate, it would argue against a further move at the next meeting in July, though there is plenty of data to see before then. Friday sees April retail sales. A preliminary estimate for a 0.7% increase was made with the March report.

UK

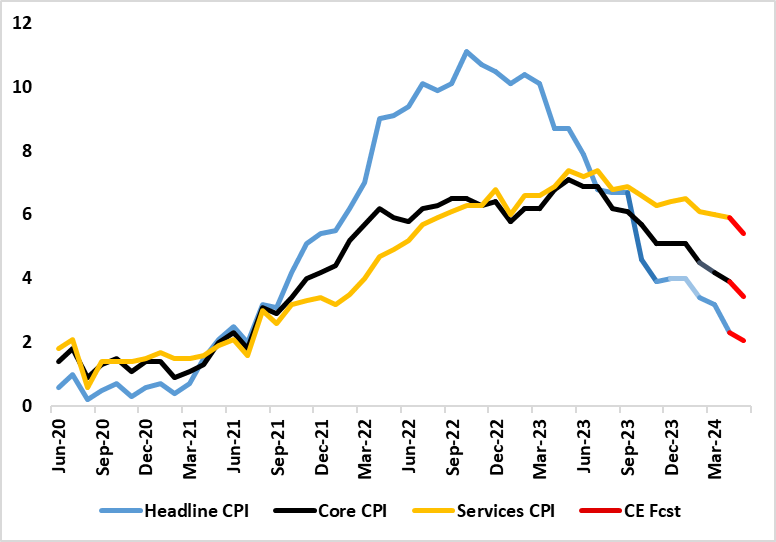

Major data awaits with the May CPI (Wed). Helped by favourable base effects and a belated drop back in services, we see the headline down 0.2-0.3 ppt to 2.0-2.1% (the lowest since July 2021). Flash PMI data are seen correcting back slightly in the June flashes (Fri). The composite fell from April's one-year high of 54.1 to 53.0 in May but also saw calmer price and costs pressures. Public borrowing data (Fri) may show more signs of flagging receipts, alongside lower-than-expected debt interest costs being offset by higher-than-expected spending on subsidies. Finally, retail sales data (Fri) may succumb (again) to poor weather which while warm overall was unsettled and wet through May, with only a modest m/m bounce.

Headline and Core Inflation Drop to Continue and Services Less Resilient?

Source: ONS, Continuum Economics

Otherwise, the focus is on the BoE where we see a 25% chance of an easing on Thursday as opposed to the near zero possibility flagged by markets, that is on the basis of our CPI projection being near correct. But with the BoE verdict now coming during a surprise election campaign this perhaps being the main factor arguing for another stable policy decision.

Eurozone

Datawise, the main interest will be the PMI flashes on Friday, where we see a small drop back in the composite having risen to a one-year high of 52.2 in May, from 51.7 in April. Overall, this indicated the apparent strongest increase in EZ economic activity since May 2023. Equally important will be whether there are more signs of easier inflationary pressures. Other business surveys are due, including the French INSEE figure (Fri) where some small improvement may be in the offing, albeit where the election call may hit sentiment. There is also EZ construction numbers (Thu) too and ECB attention some Council speakers due, most notable Chief Economist Lane (Mon) as well as the ECB Bulletin (Thu).

Rest of Western Europe

In Sweden, there is the Riksbank's Business Survey (Tue) and what are volatile labour market figures (Wed). In Norway and given the thrust of recent data and the Board’s clear caution, the Norges Bank is very likely to leave the policy rate at 4.5% for a fourth successive meeting at its next Board meeting with the decision due on Thursday. It is also likely to retain the thinking first aired at the December meeting, namely ‘policy to stay on hold for some time ahead. In Switzerland, on Thursday, we see the SNB repeating the 25 bp policy rate cut that it surprised many with three months ago. This would take the policy rate to 1.25% and where the very clear below-target inflation picture in both recent actual numbers and the outlook flagged by the SNB in March may point to further easing ahead.

Japan

The key release next week for Japan will be the National Cpi on Friday and BoJ meeting minutes on Wednesday. While the later would give us clarity on the latest BoJ decision, the National CPI carry equal or more weight as at the end of day inflation figure is the trigger for policy change. Very likely we will continue to see a higher read of CPI, but not a significant rebound as consumption remains depressed by approaching positive real wage and low savings. We also have trade balance on Wednesday and PMIs on Friday. With consumption being sluggish, export would be playing a bigger role in GDP. The weak JPY seems to continue supporting Japanese exports.

Australia

Next Tuesday, we will have the RBA interest rate decision where we expect no change to the interest rate. While inflation has been higher than forecast in the past months, it is still showing a decent moderation from the q/q basis. The inflation outlook from the RBA is too pessimistic from or point of view, still they do not see any hike but higher for longer. Else, we have job ads on Monday and PMIs on Friday.

NZ

NZ GDP will be released on Thursday and that is the only importance economic data from NZ.