Fed: Door Still Open to 2024 Rate Cuts

Though the June SEP median Fed dot is for one 25bps cut in 2024, the details of the summary of economic projections and guidance from Fed chair Powell during the press conference make clear that one or two cuts are in current Fed thinking. Data dependence is key for the Fed and we look for less GDP momentum than the Fed, plus slightly lower on inflation and this likely means two or three cuts. On balance, we forecast three 25bps cuts starting at the September FOMC meeting.

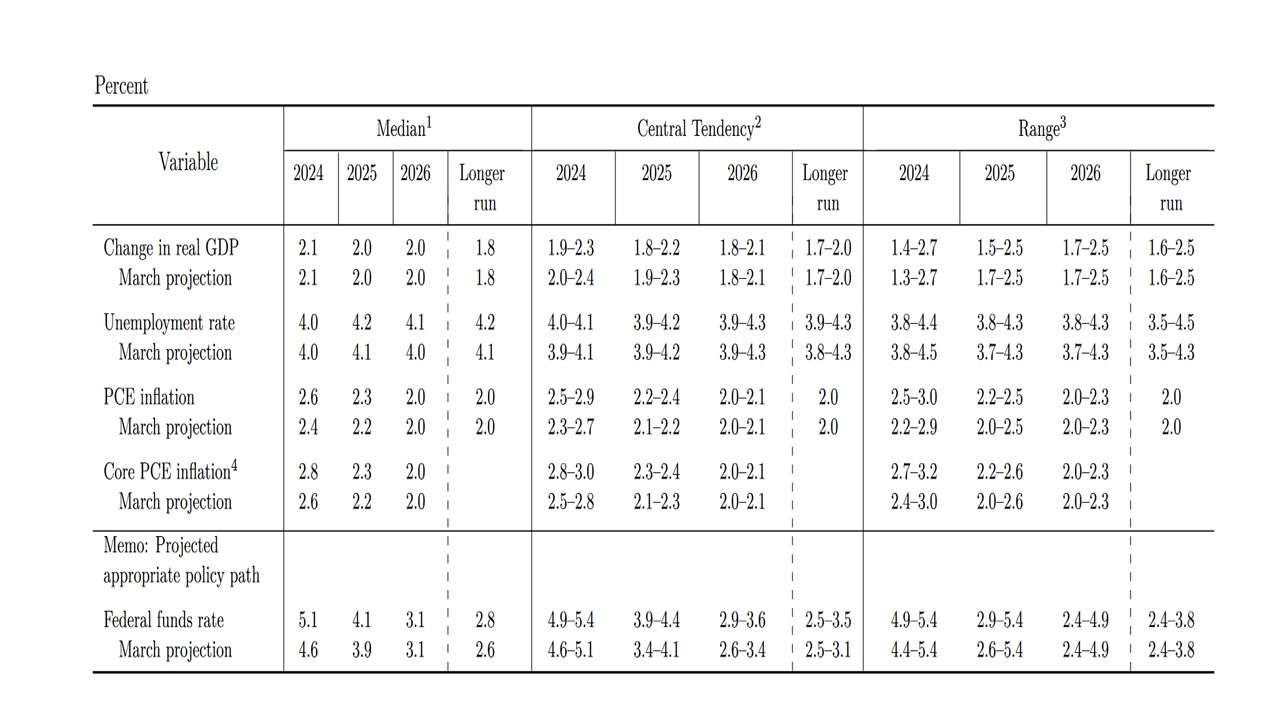

Figure 1: Fed June Summary of Economic Projections (SEP)

Source: Fed (June SEP)

Higher for Longer Then 2024 Rate Cuts

The June FOMC statement and Fed Chair Powell Q/A provide a number of clues on prospective policy. Key points include

· Inflation Revised. The SEP had upwards revision to 2024 PCE and core PCE inflation, but the median for 2025 core went up only from 2.2% to 2.3% and remain at 2.0% for 2026. This is likely to reflect a broad view on the FOMC that the disinflation process remains, but is just taking somewhat longer. Even so, the FOMC statement shows that the Fed remain patient and noting inflation remains elevated and progress to target remains modest. During the Q/A, Fed Powell indicated that the May CPI was welcome and also explained that the 2.8% median for 2024 core inflation was conservative and the outcome could be lower. The Fed made no adjustment to its GDP forecasts.

· Guidance on Interest rates. The median dots showed a move from three to one 25bps cut in 2024, but from three to four in 2025. Additionally, the breakdown shows that eight of the 19 FOMC members forecast 50bps of 2024 cuts and a 4.75-5.00% Fed Funds rate. Remember that all 19 FOMC members do not vote and the Fed chair tends to hold more weight. Thus Powell comment in the press conference that the dots did indeed show one or two rate cuts in 2024 are of interest. However, Powell noted that policy is data dependent including inflation, labor market and balance of risks around the central scenario. As in the May Q/A, he did note that a sharp softness of the labor market would likely warrant a policy response.

· Neutral drifting towards 3%. Long-term the median shifted from 2.6% to 2.8% for the Fed Funds suggesting that the consensus on the FOMC is shifting upwards from 2.5%. This process could continue multi quarter, as the current U.S. labor market tightness will not be solved quickly outside of a recession i.e. mismatch between vacancies and unemployed; reduced labor mobility and insufficient government focus on retraining. Additionally, the realignment of global supply chains and the push towards climate solutions are also creating more global inflation than the post GFC era. Though tech/AI is helping productivity and disinflation, these other forces will likely be more important. However, our macro forecasts are still consistent with the Fed Funds rate falling to the low 3’s in 2026, whereas the market is discounting a Fed Funds rate of 3.75-4.00% in 2 years.

· 2024 rate cut prospects. The Fed does not want to provide specific guidance on rates for the remainder of 2024, as it wants to see data before the next few meetings. Realistically this means three months of data by the September 18 FOMC meeting. Our GDP forecast trajectory is lower than the Fed or the market, as we see the lagged feed though of restrictive monetary policy coming through. We also favor slightly lower core PCE than the 2024 Fed median of 2.8%. We favor two to three 25bps rate cuts from the FOMC in 2024 and it is a close call depending on the scale of the economy slowdown and inflation prints. On balance, we stick with three 25bps cuts in 2024 starting at the September FOMC meeting.