FX Daily Strategy: N America, May 22nd

NZD jumped on RBNZ's upward OCR revision

GBP risks slightly on the downside on UK CPI

The USD could benefit from more hawkish FOMC minutes

NZD jumped on RBNZ's upward OCR revision

GBP risks slightly on the downside on UK CPI

The USD could benefit from more hawkish FOMC minutes

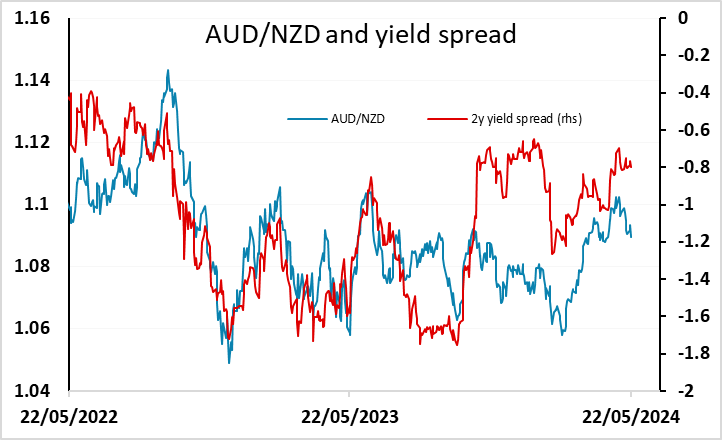

The RBNZ monetary policy decision had some impact overnight. There was no expectation of any change in policy, with nothing priced in and all forecasters looking for no change, but there was nevertheless some impact from the statement. The market was looking for rate cuts later in the year, with nearly two cuts priced by the end of the year, compared to none in Australia (or just around a 35% chance of one). The RBNZ did keep OCR at 5.5% but the OCR forecast in 2025 has been revised almost 25bps higher by september 2025. NZD/USD jumped as a knee-jerk reaction gaining around 50 pips initially, but finished the Asian session only around 15 pips higher. AUD/NZD dipped below 1.09 and held onto losses of around half a figure, although te movement in yields and yield spreads was quite modest, so holding onto these gains may prove difficult given the spread movement in favour of the AUD in recent weeks.

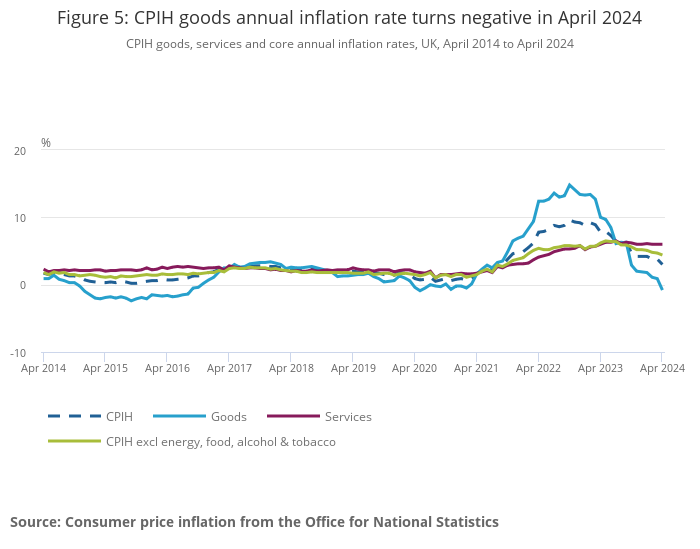

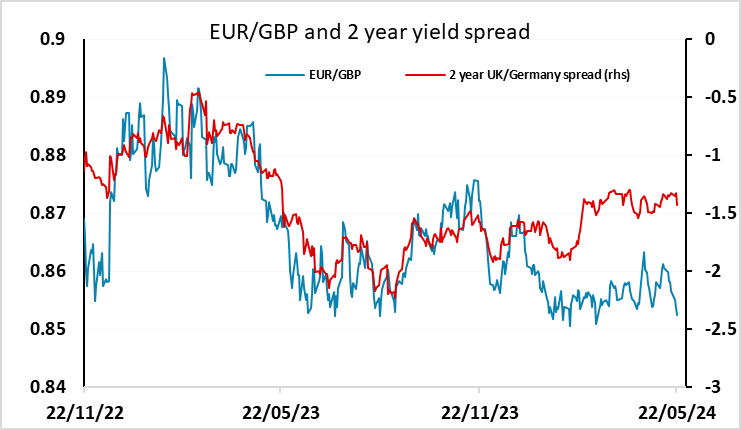

Stronger than expected April UK CPI data this morning significantly reduce if not completely rule out a rate cut from the Bank of England at the June meeting, with the market now pricing it as less than a 15% chance from around 50% before the data. GBP has rallied in response, with EUR/GBP losing 20 pips to trade below 0.8520 for the first time since March. There is still strong support down to 0.85, and even though UK yields moved higher after the data, yield spreads don’t provide a clear rationale for a break. This is still only one number, and the headline inflation print of 2.3% is the lowest since July 2021, albeit helped a lot by base effects. The core CPI decline to 3.9% y/y was also disappointing, with a market expectation of a dip to 3.6%, but this was also the lowest since October 2021. Of particular concern to the MPC hawks will be the stubbornness of services inflation, which held at 6.0% in April. This is seen as a better indicator of the underlying inflation pressure, linked to the strength of wage growth, and while headline inflation has fallen because of the decline in gas and electricity prices on a y/y basis, these base effects will soon drop out and inflation will rise again unless services inflation falls.

The June meeting therefore looks unlikely to deliver a rate cut. The MPC will want to see at least some decline in services inflation before pulling the trigger. With the ECB likely to cut in June, the short term risks are therefore now on the downside for EUR/GBP, even though yield spreads don’t provide a clear rationale for GBP strength. Longer term the risks are more balanced as in the end we see UK yields as likely to fall to similar levels to yields in the Eurozone, and GBP remains somewhat overvalued from a longer term perspective. So a dip sub-0.85 looks to be on the cards, with the 0.8492-0.8500 the initial target but scope beyond there to 0.8450 on a break. However, such losses may not last long.

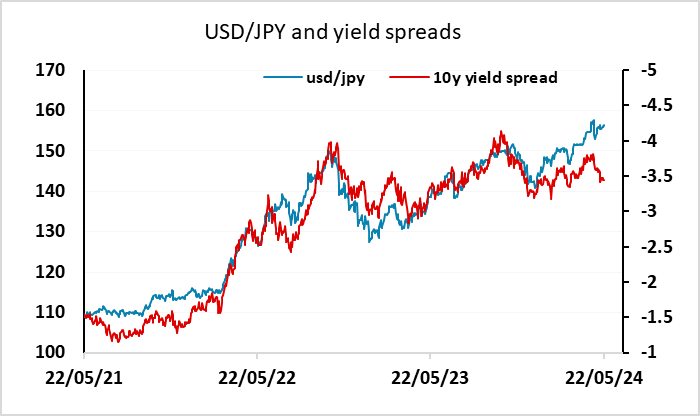

The FOMC minutes are likely to be a more hawkish than those from the March 20 meeting released on April 10, given the strength of data released between the two meetings. Restrictive policy for longer is likely to be the message, but with no clear timetable. Softer data released since May 1 may however have the FOMC feeling slightly less concerned now, so to that extent the minutes have been a little overtaken by events. Even so, the USD may manage some gains on the minutes if they remind the market that the Fed will take some convincing to cut rates by September. But even if the USD does make gains, we suspect they will be short lived, especially against the JPY with USD/JPY likely to be toppy at 157.