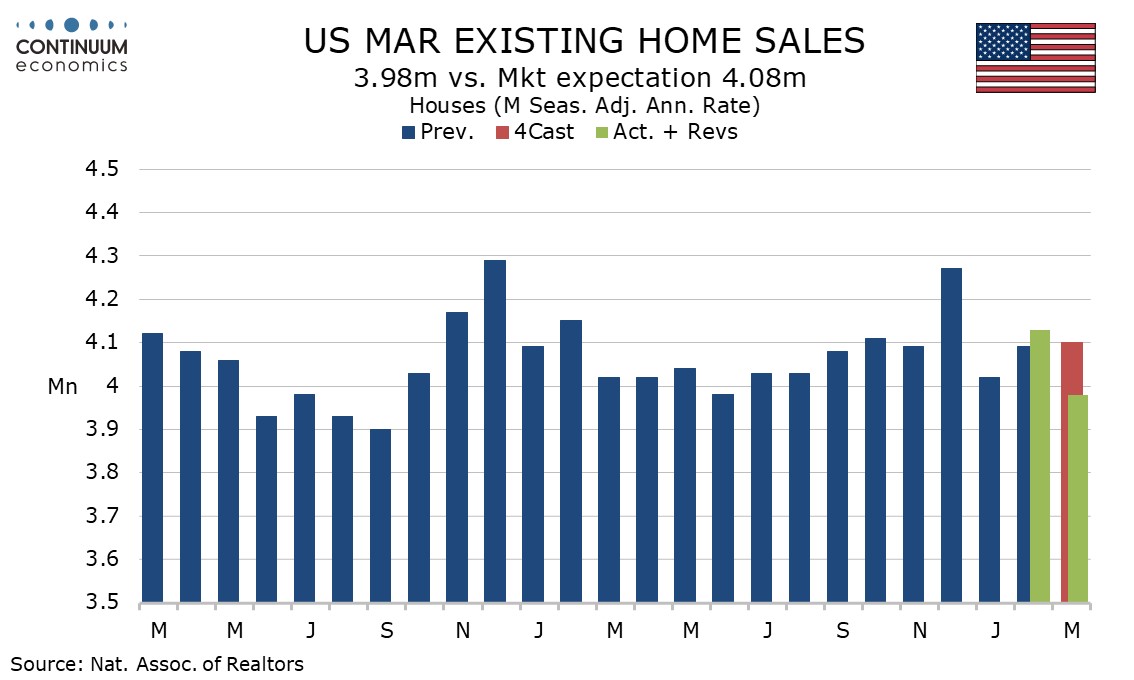

U.S. March Existing Home Sales - A weak month, downside risk in Q2

March existing home sales with a 3.6% decline to 3.98m are weaker than expected. There may be some lagged impact from bad weather in late February but if energy prices remain elevated, restricting the ability of the Fed to ease, there are downside risks in Q2.

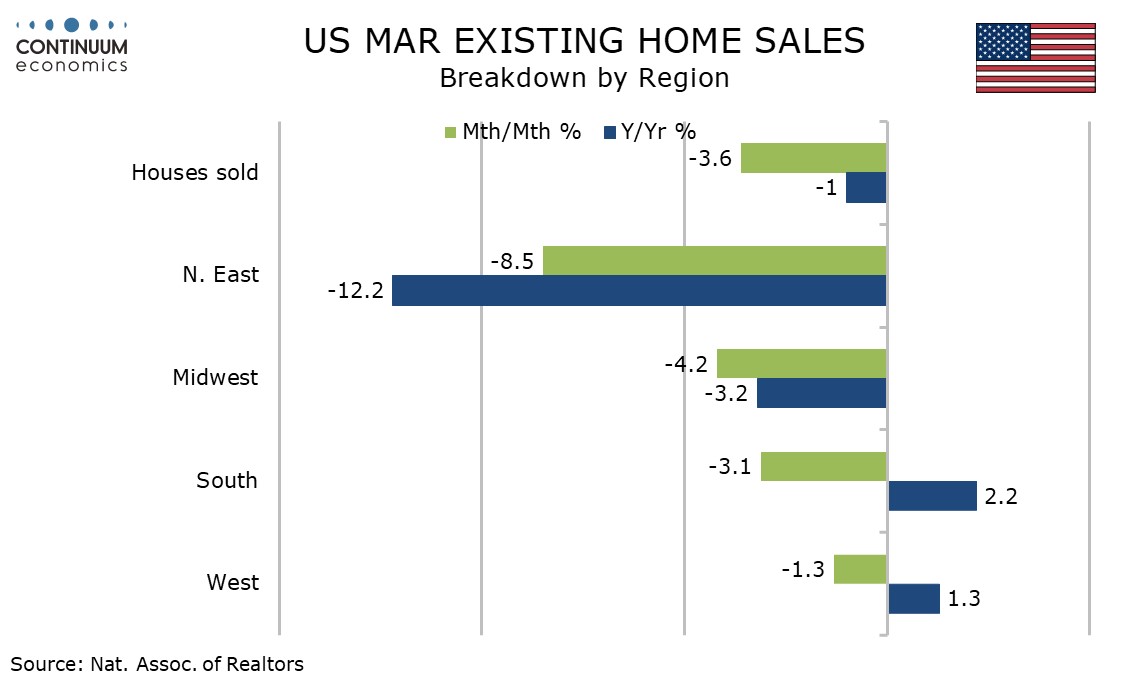

The level is the weakest since a matching June 2025, which was the weakest since October 2010, so this is clearly a weak level of activity. Sales fell in all four regions but declines of 8.5% in the Northeast and 4.2% in the Midwest may have been exaggerated by weather. The South and West while down on the month are still up yr/yr.

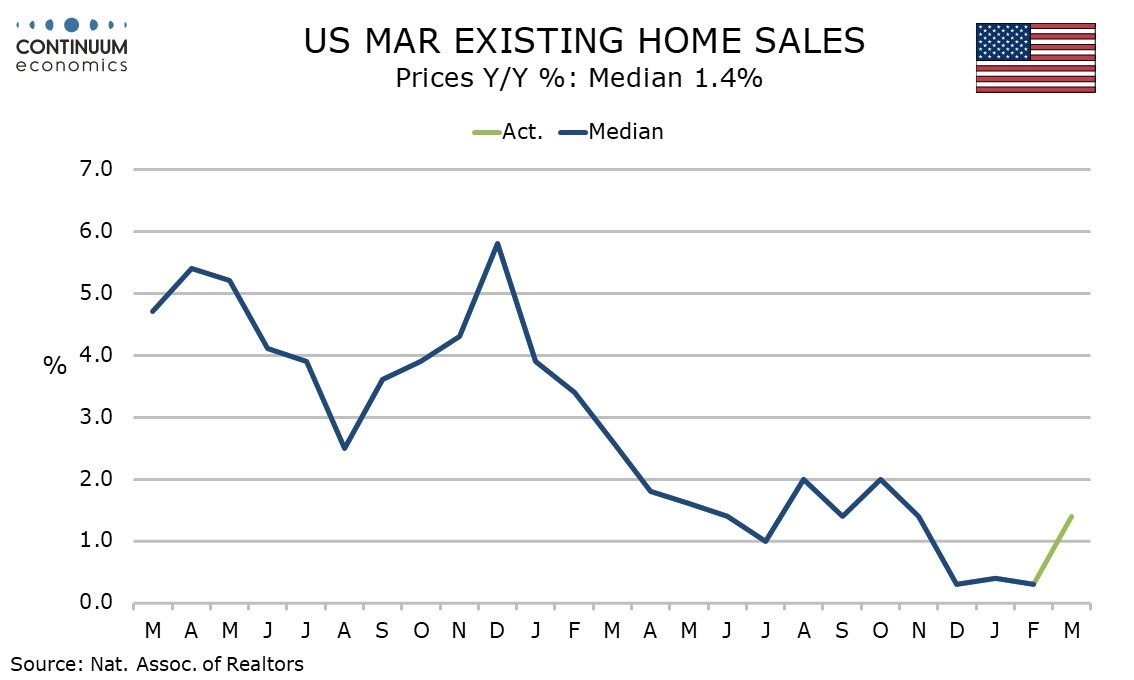

The median price saw a rise of 2.7% on the month, and while this is in part seasonal yr/yr growth was lifted to 1.4% from 0.3%, which hints that the weakness of sales is overstated relative to the underlying picture.

Survey evidence from February pending home sales and March’s MBA and NAHB data showed marginal improvement if still at weak levels, but the weekly MBA data lost momentum late in the month as mortgage rates picked up. This suggests downside risks in Q2.