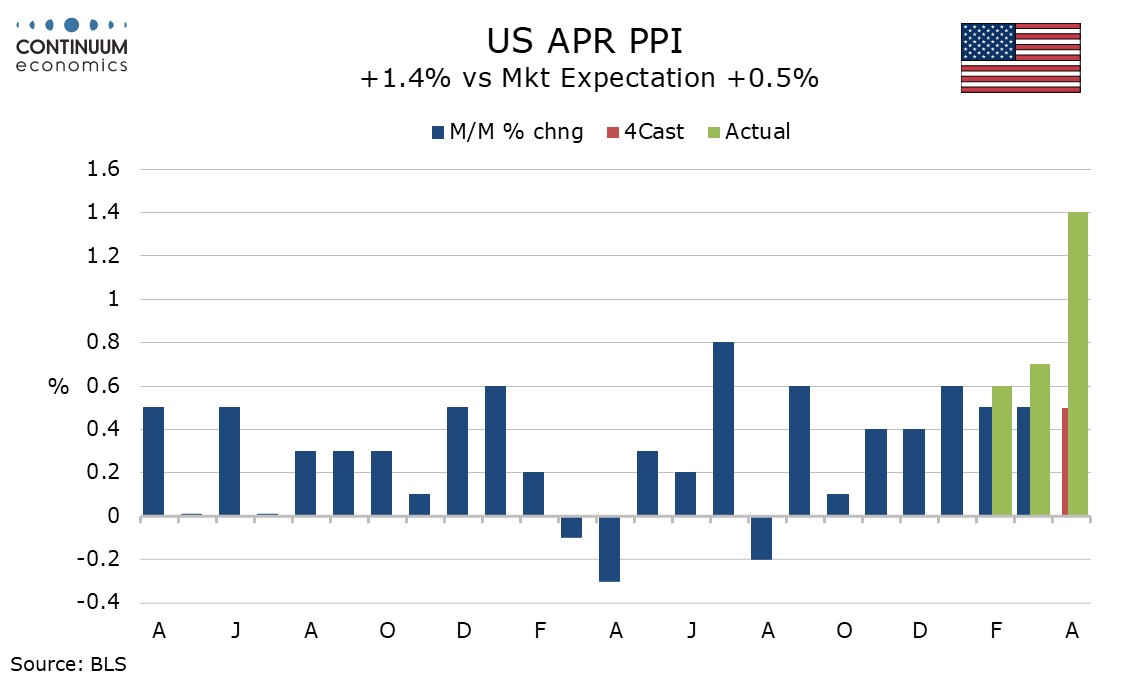

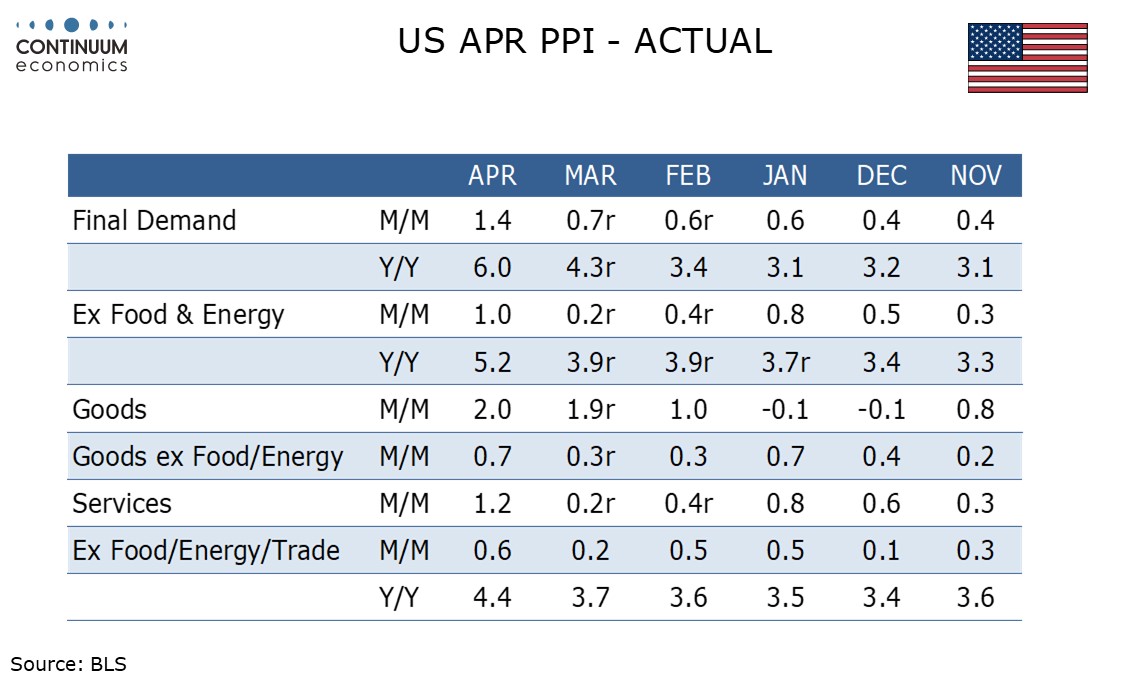

U.S. April PPI - Strong picture restored after pause in March core rates

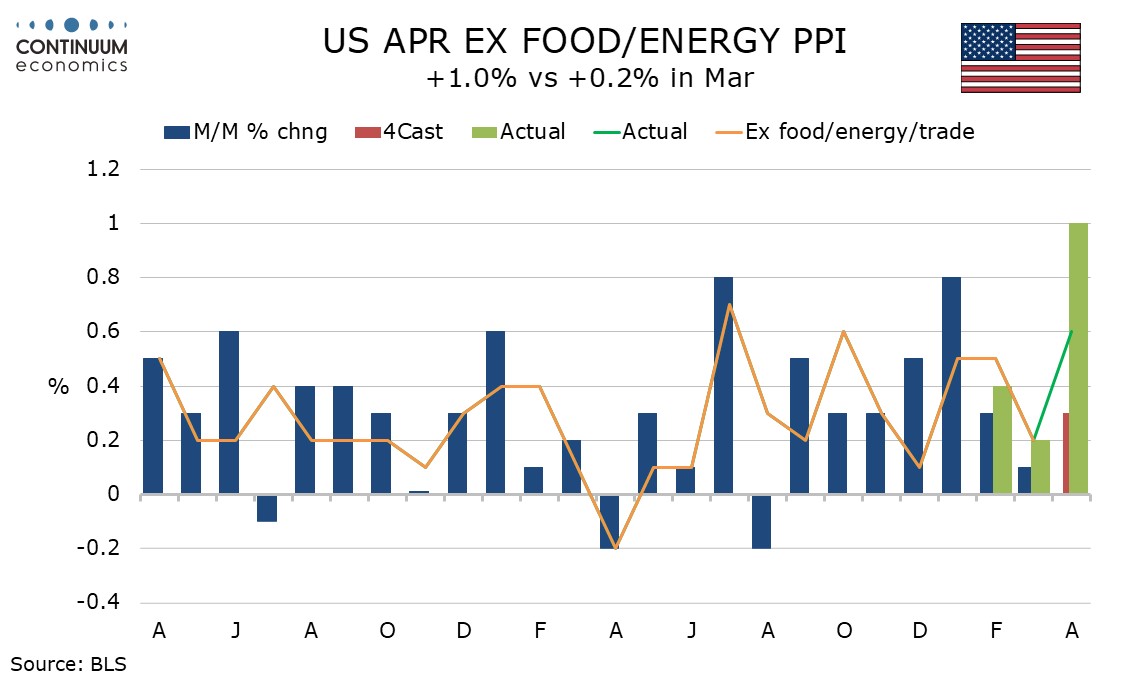

After a surprisingly low March, which saw modest upward revisions, April PPI has rebounded above expectations, rising by 1.4% overall, 1.0% ex food and energy and 0.6% ex food, energy and trade. March and April together show the strength of January and February’s core rates persists, with energy, though not yet food, accelerating.

The 1.0% rise ex food and energy and the 0.6% rise ex food, energy and trade both follow gains of 0.2% in February, with the latter having increased by 0.5% in both January and February.

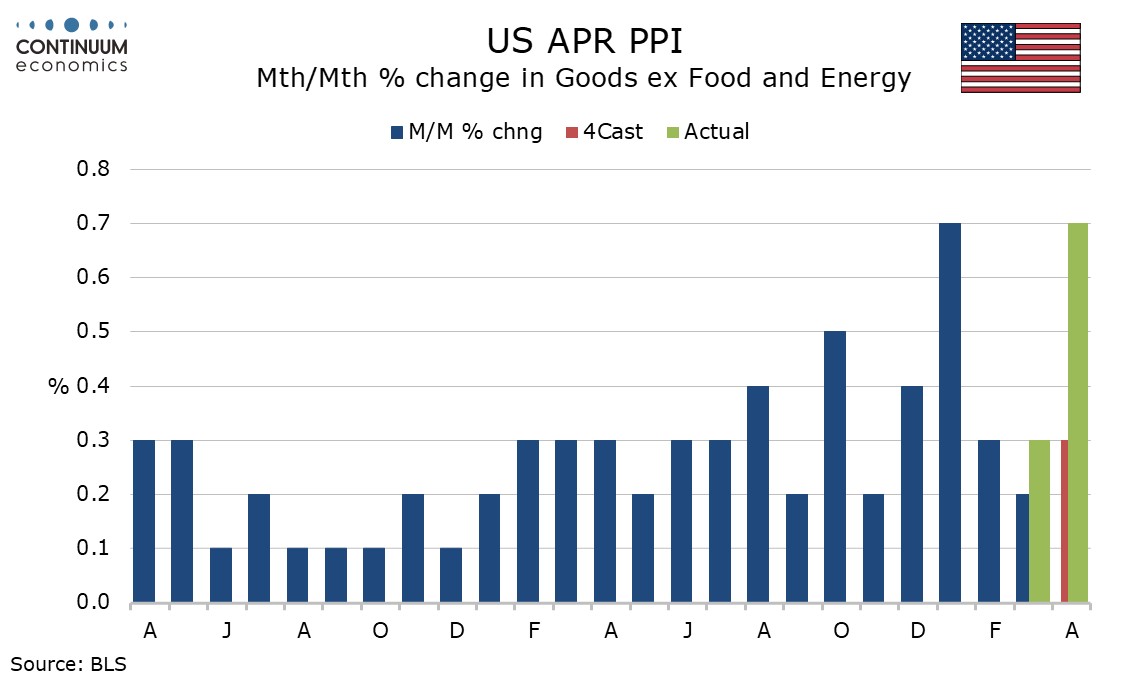

Goods less food and energy rose by 0.7% in January and April with two gains of 0.3% in between. The April gain suggests hopes that the tariff boost was fading may have been premature, or is now being replaced with an energy feed-through.

Services surged by 1.2% in April, with very strong gains of 2.7% in trade and 5.0% in transportation and warehousing, though other services remain subdued with a rise of only 0.1%.

A 7.8% rise in energy, led by a 15.6% rise in gasoline, extended respective gains of 10.1% and 19.2% in March, and weekly data for early May suggests there is more to come. While there are fears that the Middle East conflict will lift global food prices, so far there is not much to see in the PPI, with a modest 0.2% rise in April following a 0.6% decline in March.

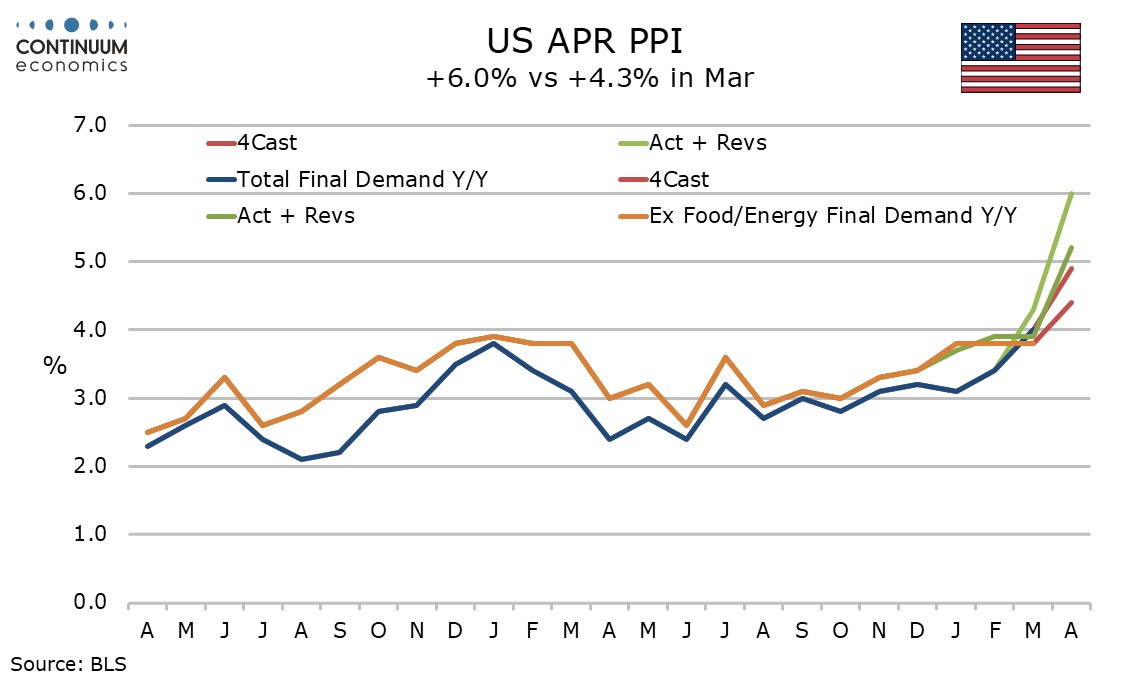

Yr/yr PPI has bounced to 6.0% from 4.3% and is the highest since December 2022. Ex food, energy and trade PPI now stands at 4.4%, a break from a 3.4% to 3.7% range over the past six months and up from sub-3.0% levels in early 2025.

Intermediate goods show strength overall. With processed goods up 2.7% on the month and unprocessed goods up by 4.1%. Ex food and energy the former was strong with a 1.5% rise but the latter saw a 1.0% decline. However unprocessed goods saw strength in food as well as energy, Intermediate services were strong with a 1,1% rise, and here even other services, up by 0.5%, was quite strong.