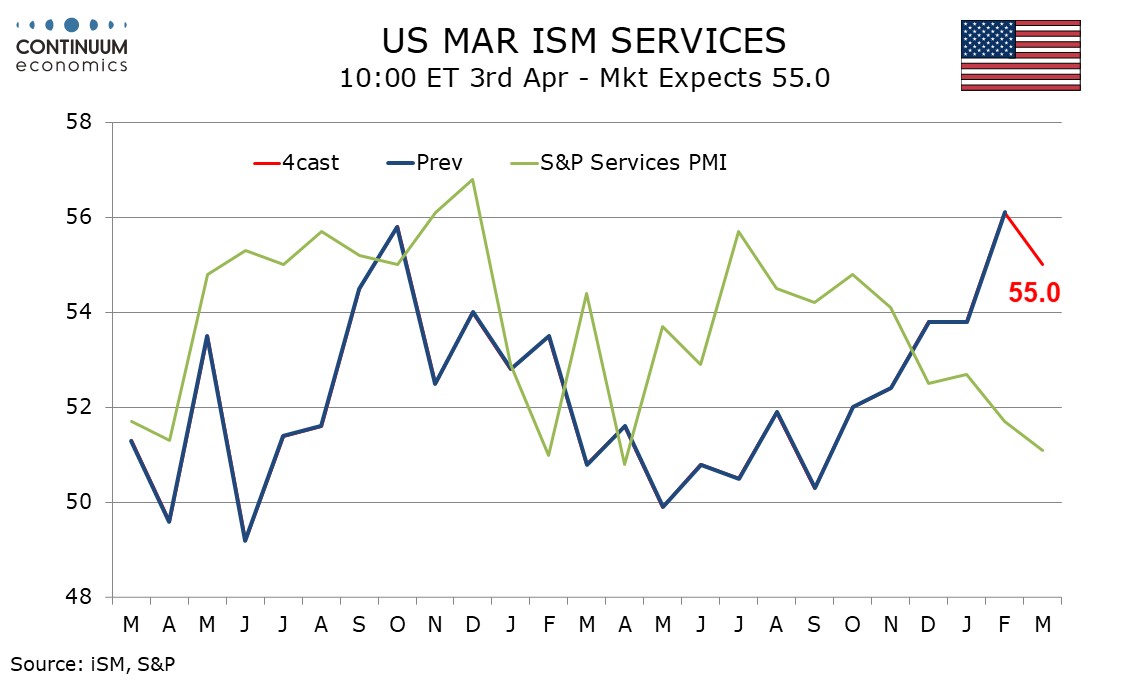

Preview: Due April 3 - U.S. March ISM Services - February strength difficult to sustain

We expect March’s ISM services index to slip to 55.0 from February’s 56.1, which in being the highest reading since July 2002 looked unsustainably high, even ahead of the Middle East conflict.

The Middle East conflict presents downside risk to consumers due to higher energy prices. The strength of recent ISM services data has not been matched by the S and P services index, which is trending in the opposite direction. Regional service sector surveys show continued weakness from the Empire State and Philly Fed in March, though the Richmond Fed’s did see a bounce from a weak February.

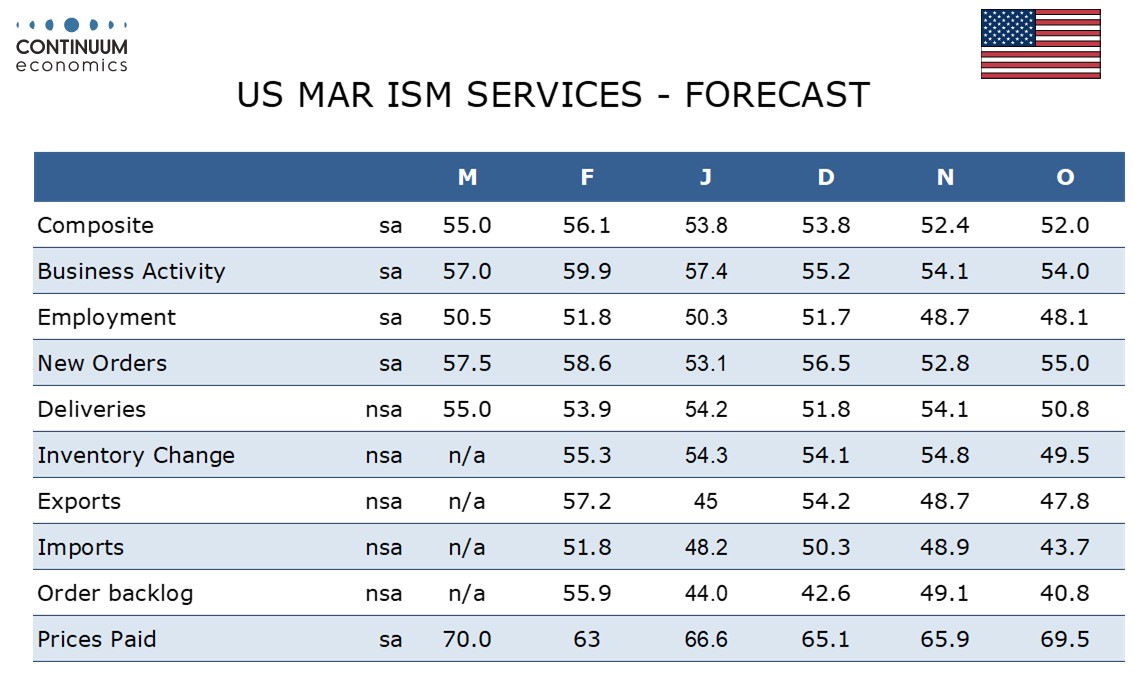

We expect ISM services detail to show slippage in three of the four components that make up the composite, the exception being delivery times which may be supported by the situation in the Middle East. While new orders may be particularly vulnerable, they will get some support from seasonal adjustments. In contrast, the seasonal adjustments for business activity and employment are more negative.

Prices paid do not contribute to the composite and here we see a bounce to 70.0 from 63.0 on higher energy prices. This will be the highest reading since October 2022.