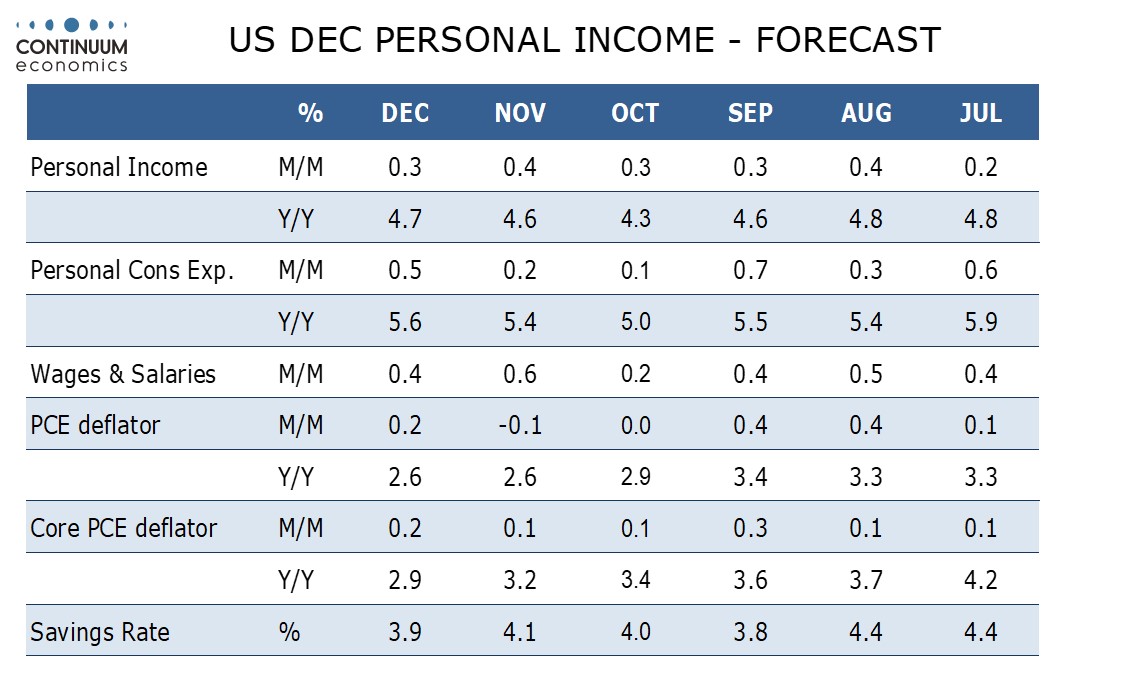

Preview: Due January 26 - U.S. December Personal Income and Spending - Q4 totals to be confirmed, PCE prices seen softer than CPI

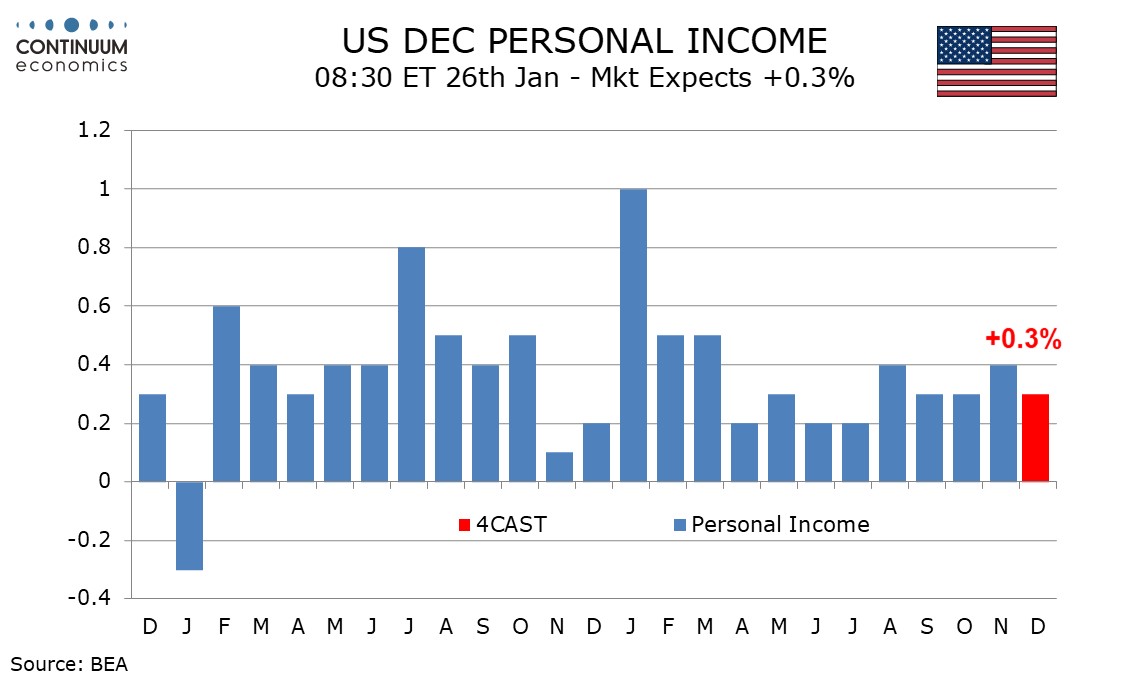

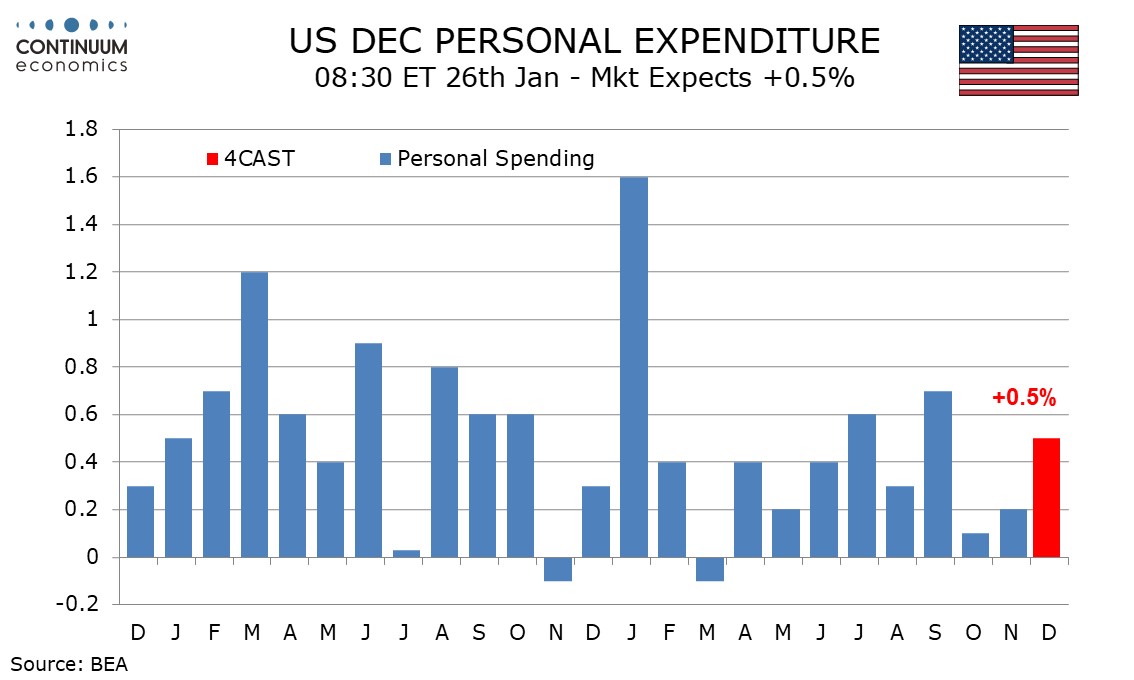

December’s personal income and spending report will be largely old news with Q4 totals already seen in the GDP report. The Q4 totals are consistent with our forecasts for a 0.2% gain in core PCE prices and a 0.3% gain in personal income, though imply a 0.7% gain in personal spending, above. 0.5% is still possible if October and November are revised higher.

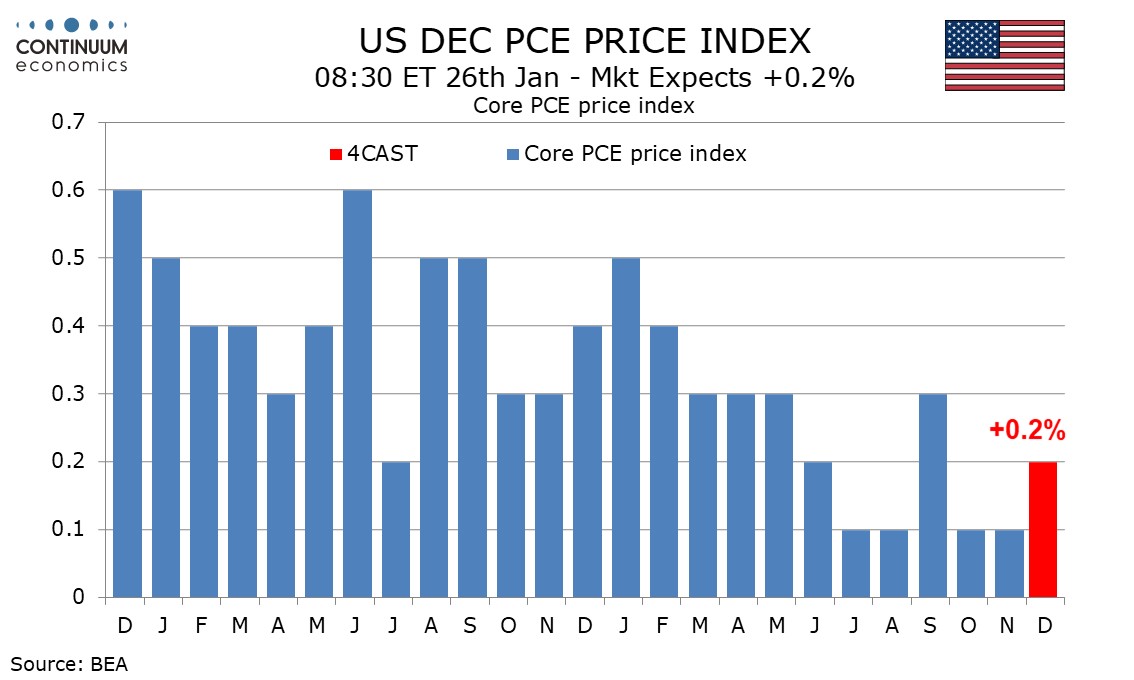

CPI increased by 0.3% in December, both overall and ex food and energy, but recently CPI has been outperforming PCE price data, where we expect December gains of only 0.2% both overall and ex food and energy.

In fact we expect the December PCE gains to be marginally below 0.2% both overall and ex food and energy before rounding even though CPI gains were very marginally above 0.3% in both series. Yr/yr PCE prices would then remain at 2.6% but the core rate would slow to 2.9% from 3.2%.

In the personal income detail we expect a 0.4% rise in wages and salaries with a dip in the workweek weighing against strong gains in employment and average hourly earnings. We expect the other components of personal income to be in line with trend, after a weak November corrected a strong October.

Retail sales increased by 0.6% in December but we expect a slightly slower 0.4% rise in services, with real spending in services increasing by 0.2% for a fourth straight month. The GDP detail is consistent with our services view, with non-durables being the main source of the Q4 beat. This could easily come at least in part from upward revisions to October or November.