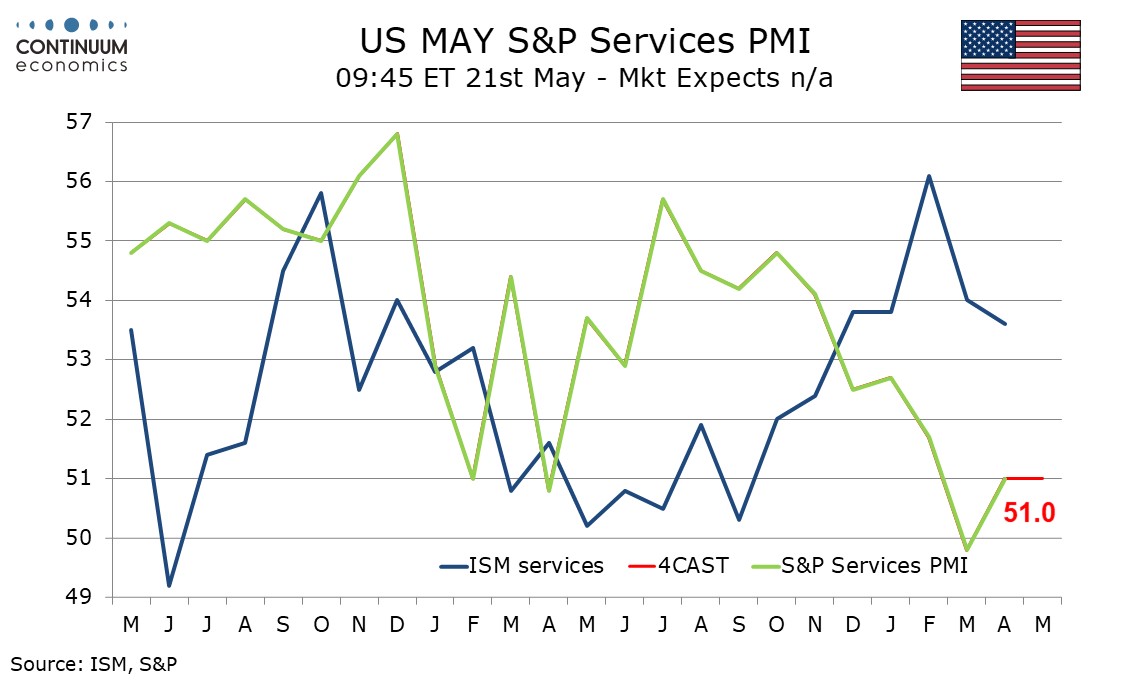

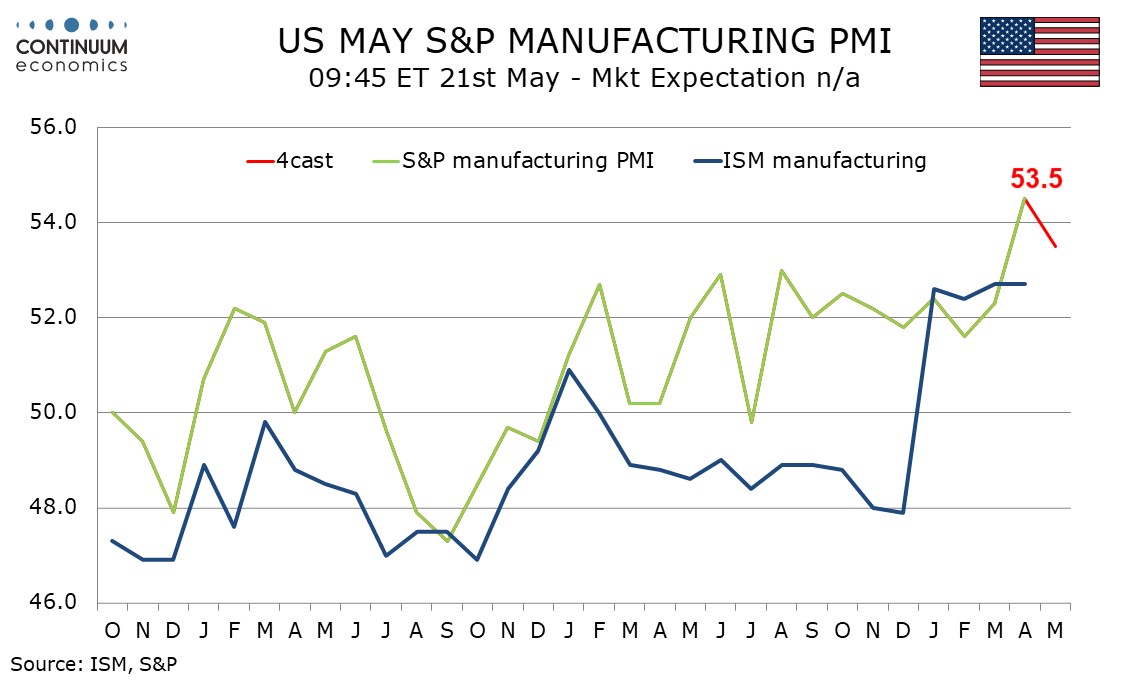

Preview: Due May 21 - U.S. May S and P PMIs - Manufacturing to correct lower, services stable but subdued

We expect a correction lower in May’s S and P manufacturing PMI to a still firm 53.5 from 54.5, but an unchanged S and P services PMI at a still subdued 51.0.

April’s S and P manufacturing PMI was the strongest since May 2022, and our forecast for May would be too if April’s bounce from March’s 52.3 is excluded. April’s bounce moved ahead of the ISM manufacturing index, which has shown little change in the last four months after turning positive in January. The manufacturing picture remains positive, but there is scope for a correction lower in the S and P index.

The S and P services index also bounced in April from a March index which fell below the neutral 50 level for the first time since January 2023. Even before the oil shock trend in the ISM services index was sliding, underperforming the ISM services index, suggesting a further increase from April’s 51.0 reading is unlikely. Consumers are getting squeezed by higher gasoline prices, but the underlying picture probably remains marginally positive, with March’s negative reading probably understating the picture.