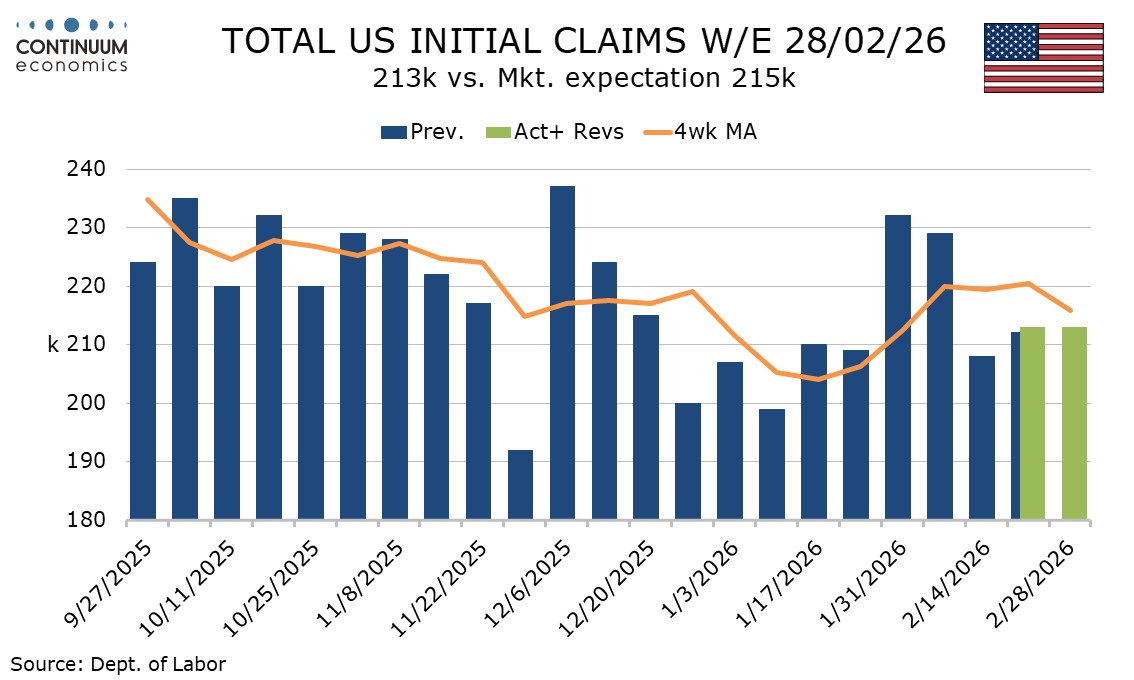

U.S. Initial Claims remain low, Some inflationary risk visible in Q4 Productivity and Costs report

Initial claims are unchanged at 213k, a recent bout of bad weather having no significant impact, contrasting late January when a spell of bad weather did coincide with a rise in initial claims. Q4 productivity data is solid but this is not eliminating inflationary pressures.

The survey week for February’s non-farm payroll came two weeks ago. The spike in initial claims in late January means that the 4-week average, which fell to 215.75k this week, stood at 219.5k in February’s payroll survey week, up from 204k in January’s but little changed from 217.5k in December’s. January’s payroll was above trend, and unlikely to be matched in February, but a very weak February payroll is not signaled.

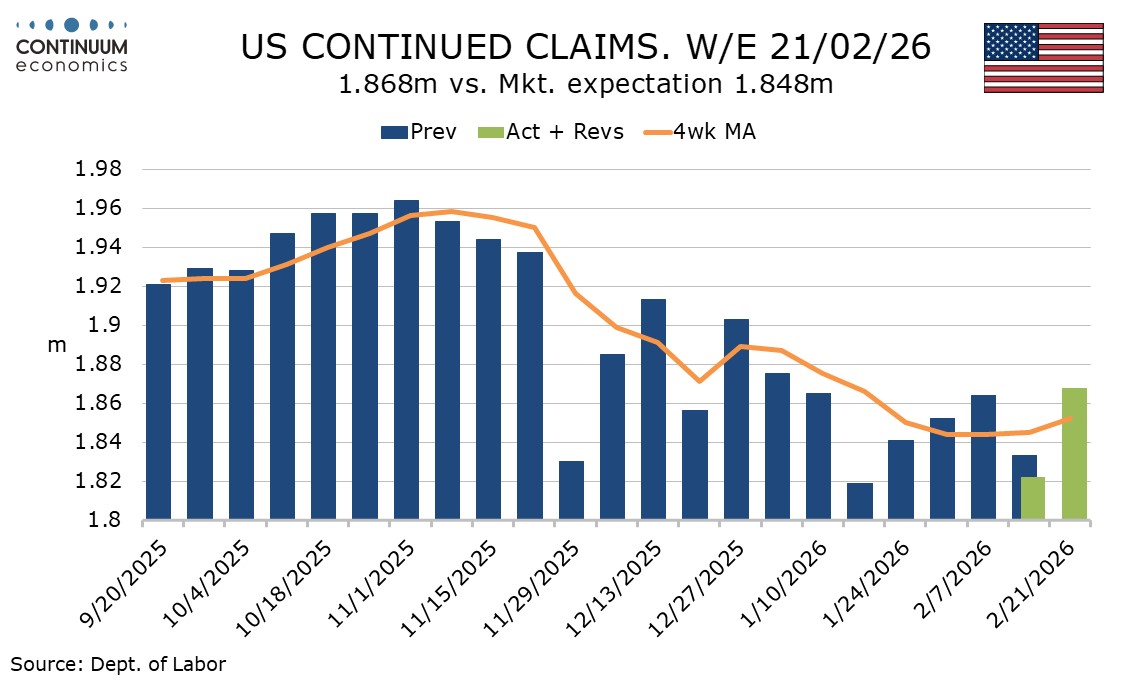

Continued claims cover the week before initial claims, and the week after February’s payroll was surveyed. Here the data was higher than expected, up 46k to 1.868m, but this does little more than erase a 42k decline in the preceding week, which came in the week the payroll was surveyed. A decline in the 4-week average may however be finding a base.

February corporate layoff data from Challenger, Gray and Christmas provides further comfort on the labor market, falling 71.9% yr/yr to largely reverse an alarming 117.8% rise seen in January, which provided a misleadingly negative signal for January’s non-farm payroll.

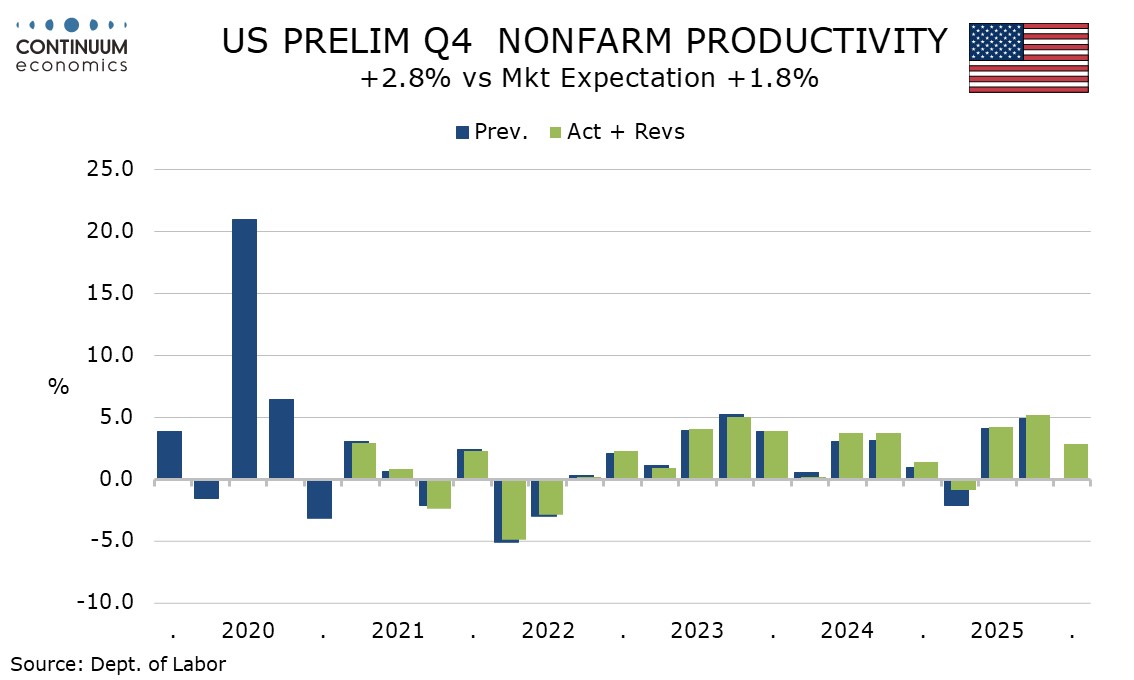

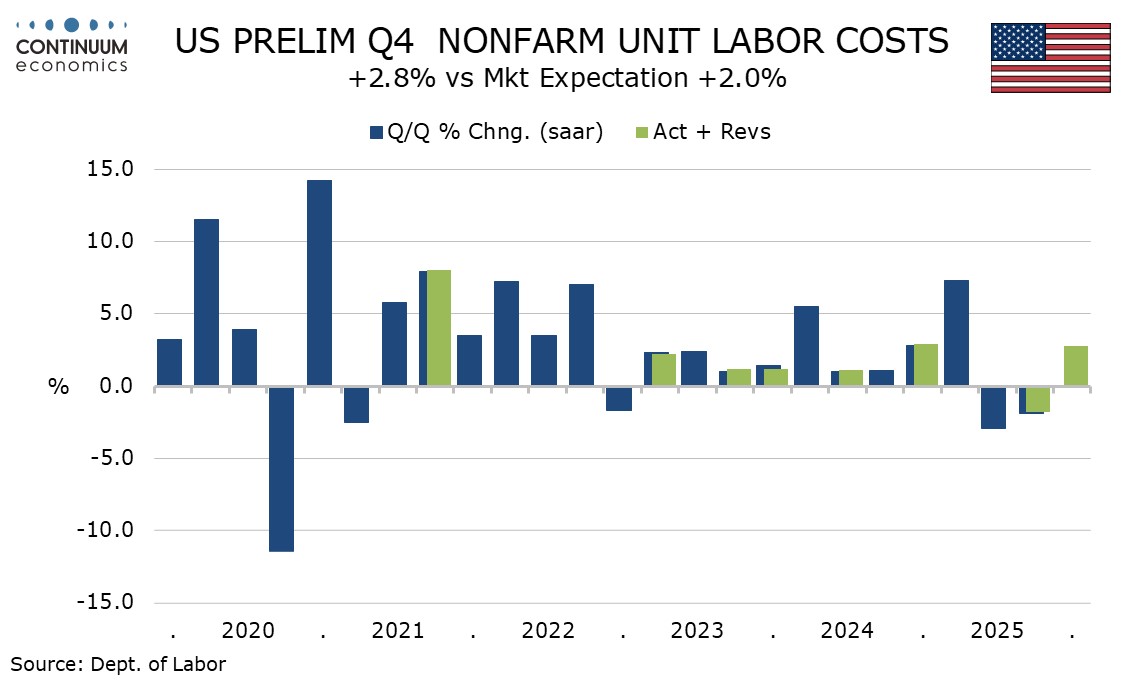

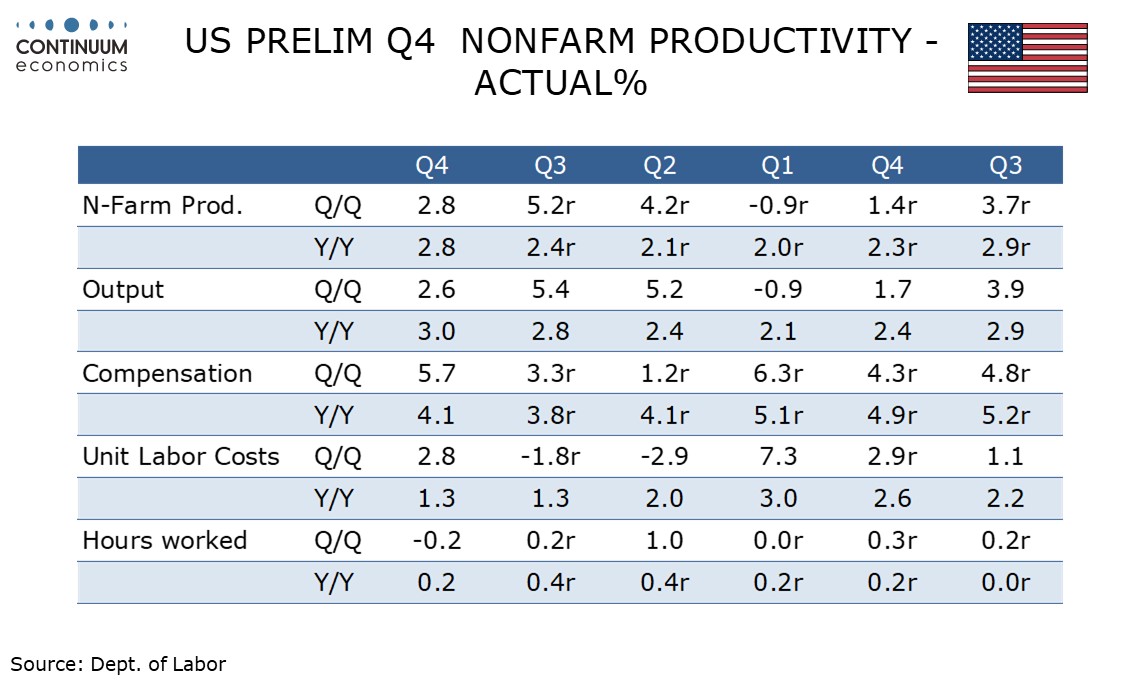

Q4 non-farm productivity at 2.8% was stronger than expected. Non-farm business output rose by 2.6% as signaled by GDP detail, outperforming overall GDP which was depressed by the government shutdown. Aggregate hours worked however fell by 0.2%, weaker than implied by non-farm payroll data, lifting productivity.

Compensation at 5.7% rose by a 3-quarter high and is stronger than payroll average hourly earnings implied. This meant that even with the productivity beat unit labor costs also exceeded expectations at 2.8%.

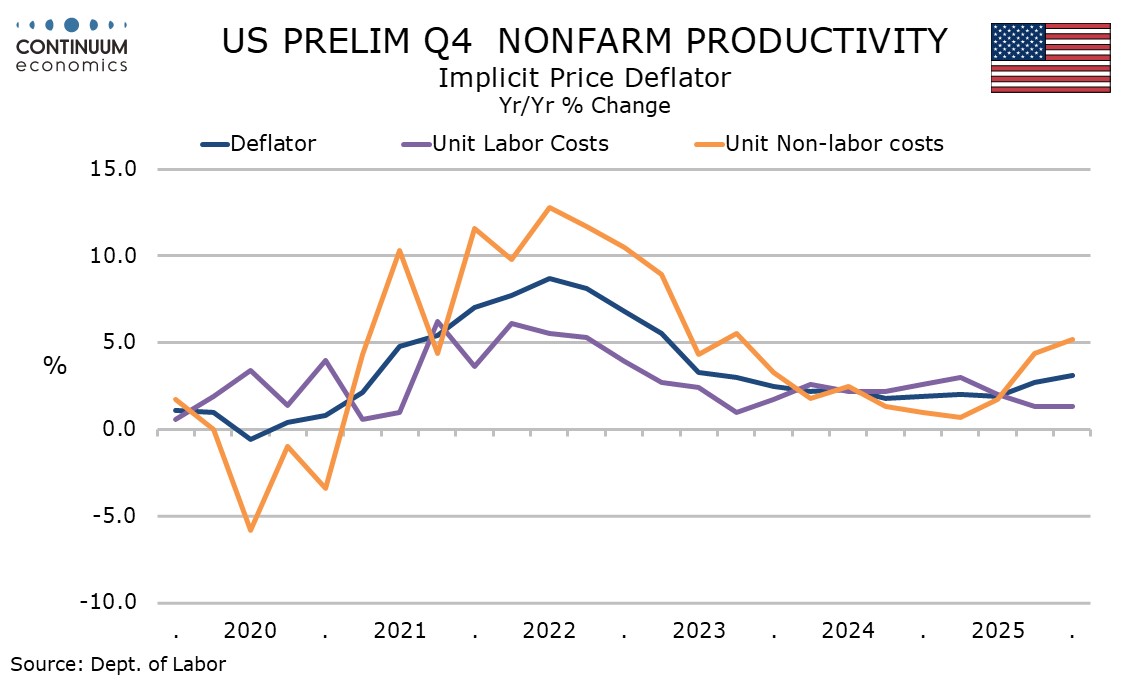

Non-labor costs at 3.6% saw a significant slowing from two strong quarters probably lifted by tariffs, but are still quite firm. The overall deflator rose by 3.1% in the quarter which matches a 10-quarter high in the yr/yr pace. This suggests that underlying inflationary pressures have accelerated to a pace stronger than the Fed’s 2.0% target.