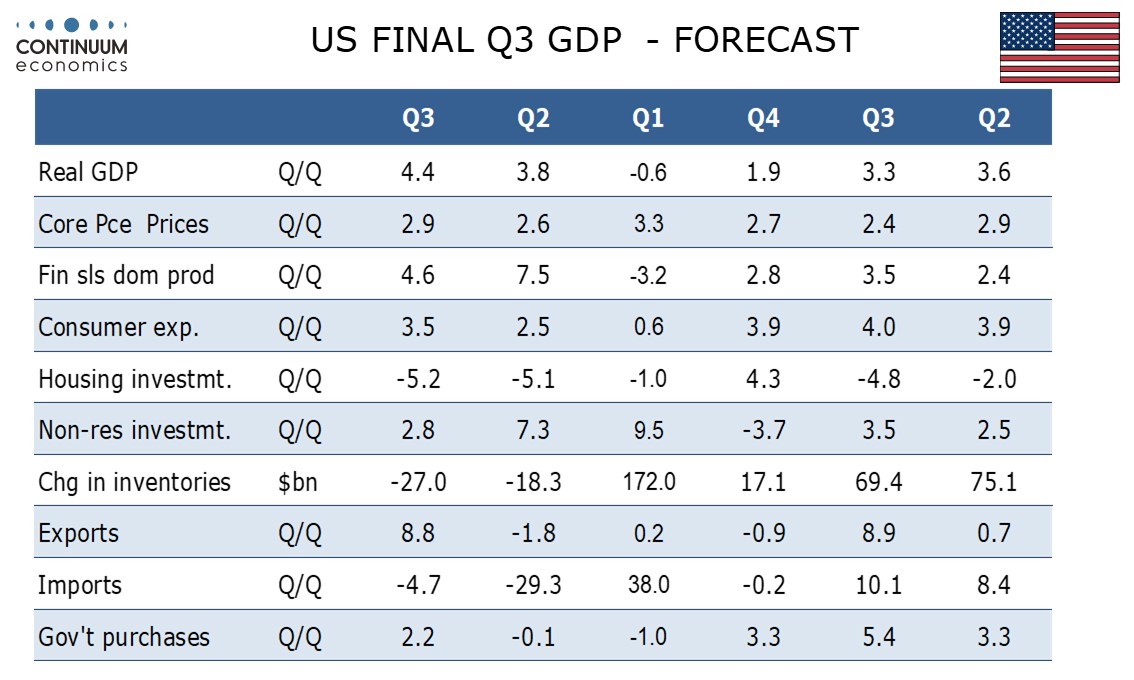

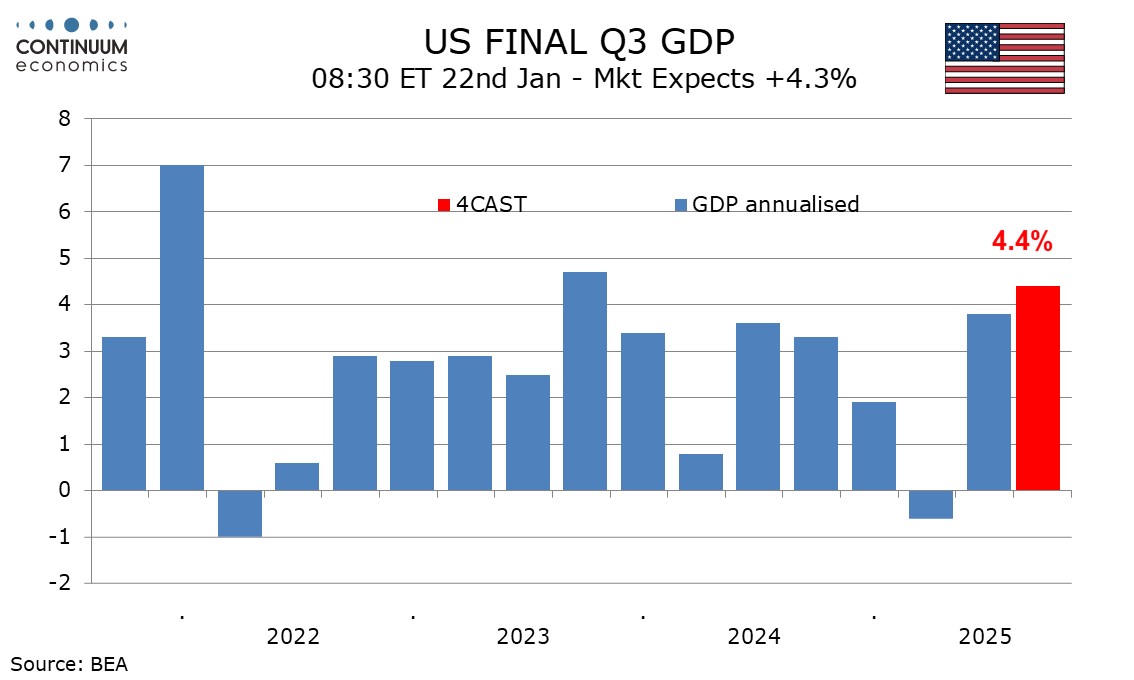

Preview: Due January 22 - U.S. Final (Second) Estimate Q3 GDP - Marginally stronger still

We expect a marginal upward revision to Q3 GDP to 4.4% from an already strong 4.3%. The only component we are expecting a revision to is inventories, on an upward revision to September retail inventories led by autos.

Most components will not see significant revisions with the first estimate having come later than usual due to the shutdown and thus less subject to revisions than usual. October’s trade data did see upward revisions to Q3 data led by services, but the data in the previous Q3 GDP report looks consistent with the revised trade data.

September construction spending data due on January 21 could still change the outcome. We do not expect any revisions to the price indices, of 2.9% for core PCE, 2.8% for overall PCE and a significantly higher 3.8% for GDP.