FX Daily Strategy: N America, December 20th

GBP risks on the upside on UK CPI

BoE priced to cut less than ECB and Fed, but this looks justified

USD weakness on Tuesday to fade

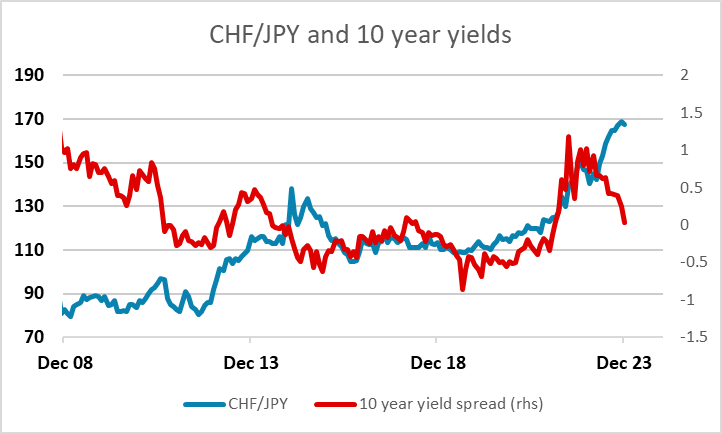

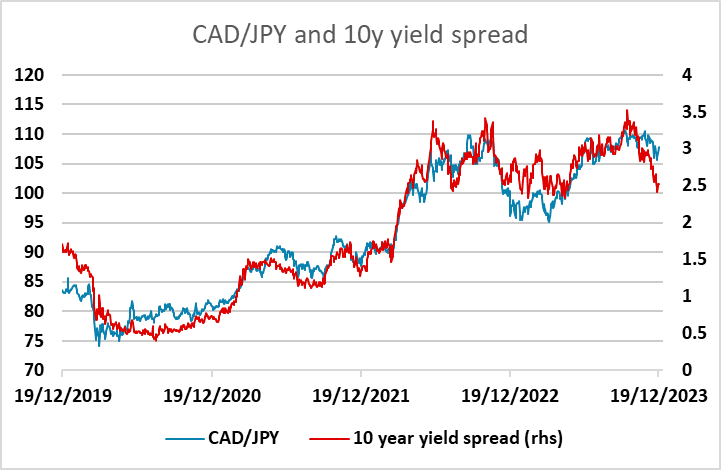

JPY decline overdone, most obviously against the CAD and CHF

GBP risks on the upside on UK CPI

BoE priced to cut less than ECB and Fed, but this looks justified

USD weakness on Tuesday to fade

JPY decline overdone, most obviously against the CAD and CHF

GBP fell after the much lower than expected UK CPI figure, with the ONS indicating that it was driven by eight sub categories. The sharp decline in core CPI from 5.7% to 5.1%, will provide comfort in itself to the BOE but will also raise questions whether UK inflation is slowing more quickly than BOE assumptions. This will fuel spring rate cut talk, especially as we think that the market can discount more on UK rates. GBP lost ground across the board.

EUR/GBP has moved closely with 2 year yield spreads in the last year, so we would see a bias towards a soft GBP v EUR, as rate cut speculation grows still further.

Otherwise Wednesday is a relatively quiet calendar. There is German consumer confidence and US existing home sales, but neither seem likely to move the market. The USD was generally soft on Tuesday against everything but the JPY, helped by the gains in equity markets on the back of lower yields. Nevertheless, we don’t see much more USD downside here, with yields unlikely to fall significantly and 1.10 likely to be a difficult barrier for EUR/USD to break.

The JPY was the outlier, as the market showed disappointment at the lack of any change in BoJ rhetoric at the BoJ meeting. Even so, JPY weakness looks very overdone, with yield spreads still pointing the general JPY gains. The correlation with yield spreads has been strongest with USD/JPY and CAD/JPY, but from a value perspective CHF/JPY looks the most obvious trade, with the CHF having no significant yield advantage to justify the 30% rise in CHF/JPY in the last two years. Meanwhile, the SNB indicated that they will wind down their CHF buying/FX selling going forward, which should reduce CJF strength.