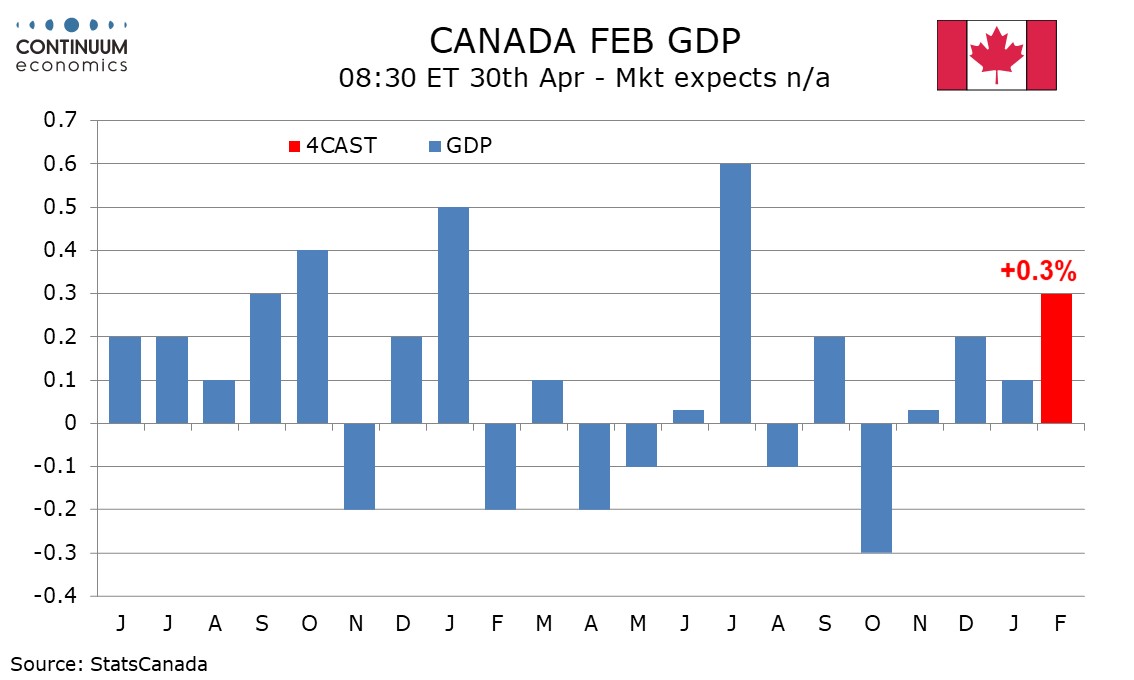

Preview: Due April 30 - Canada February GDP - A stronger month though March may slip

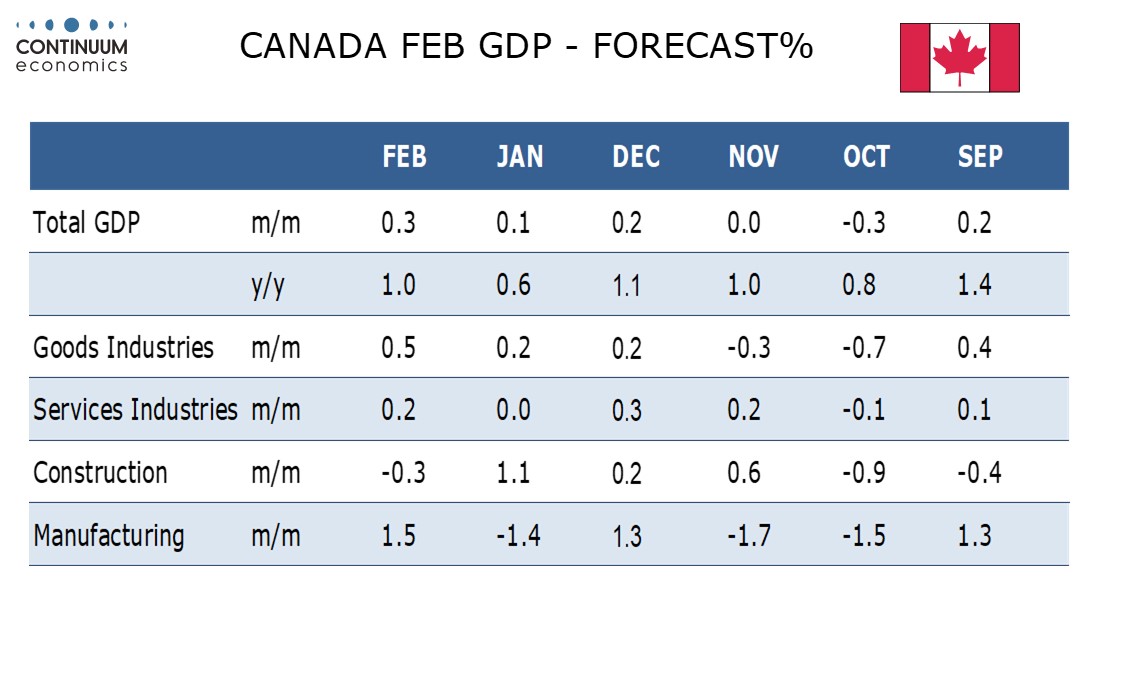

We expect February GDP to increase by 0.3%, slightly stronger than a 0.2% gain predicted with January’s report, though risk is for a weaker preliminary estimate for March. If March declines by 0.1% after a 0.3% February increase, and January’s 0.1% increase is unrevised, this would imply a 1.6% annualized increase in Q1.

The energy shock will have mixed implications for Canada, but we would expect the negatives to be felt more in March with the energy industry likely to take time to respond to higher prices. A 1.6% annualized Q1 increase would be slightly lower than a 1.8% forecast made in January’s Bank of Canada Monetary Policy Report, though at March’s meeting the BoC stated that near term GDP growth could be lower than anticipated in January. 1.6% may be stronger than the BoC expected in March.

January’s report looked for positive February contributions from manufacturing, mining and finance/insurance, with the relatively small agriculture, forestry, fishing and hunting sector being the only negative cited. In February we expect manufacturing to fully explain a 0.5% increase in goods output with February’s shipments report rebounding from a weak January. Wholesale and retail are likely to make positive contributions to services, where we expect a 0.2% increase after a flat January.

Yr/yr GDP would then pick up to 1.0% from 0.6% in January, returning to near Q4 levels. While we expect a stronger monthly GDP report, this would contrast a very weak February employment report which probably understated the underlying picture.