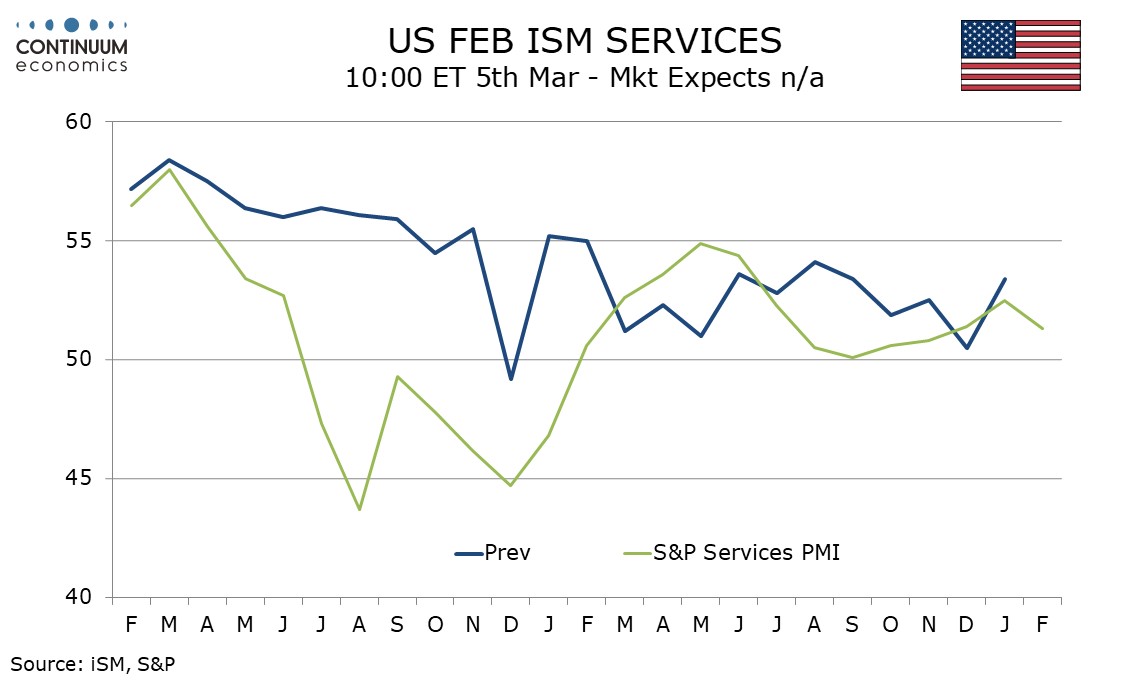

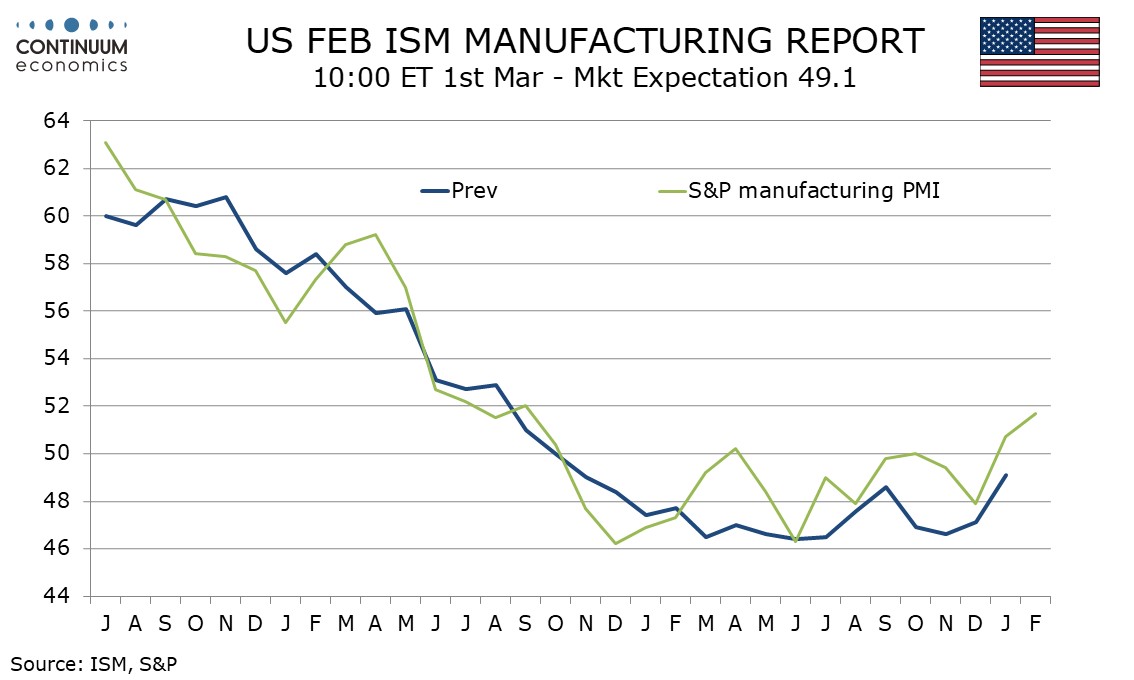

U.S. February S&P PMIs - Similar levels, contrasting direction

February’s preliminary S and P PMIs show similar levels, though manufacturing is significantly stronger at 51.7 from 50.7 and services weaker at 51.3 from 52.5. The composite fell to 51.4 from 52.0.

The manufacturing index is the strongest since September 2022, and the first significant move above neutral since then. The data suggests December’s improvement in the ISM manufacturing index can be extended, particularly with January’s Philly Fed and Empire date surveys showing improvement, though only the former moved above neutral.

The S and P services index is not well correlated with its ISM counterpart. It does however appear responsive to moves in bond yields with a slide to a low of 50.1 in September before seeing four subsequent gains. This month’s dip appears to be responsive to renewed gains in bond yields after recent strong data.