Published: 2023-12-14T15:49:59.000Z

Preview: Due December 21 - U.S. Final (Third) Estimate Q3 GDP - Staying strong, though Q4 seen slower

-

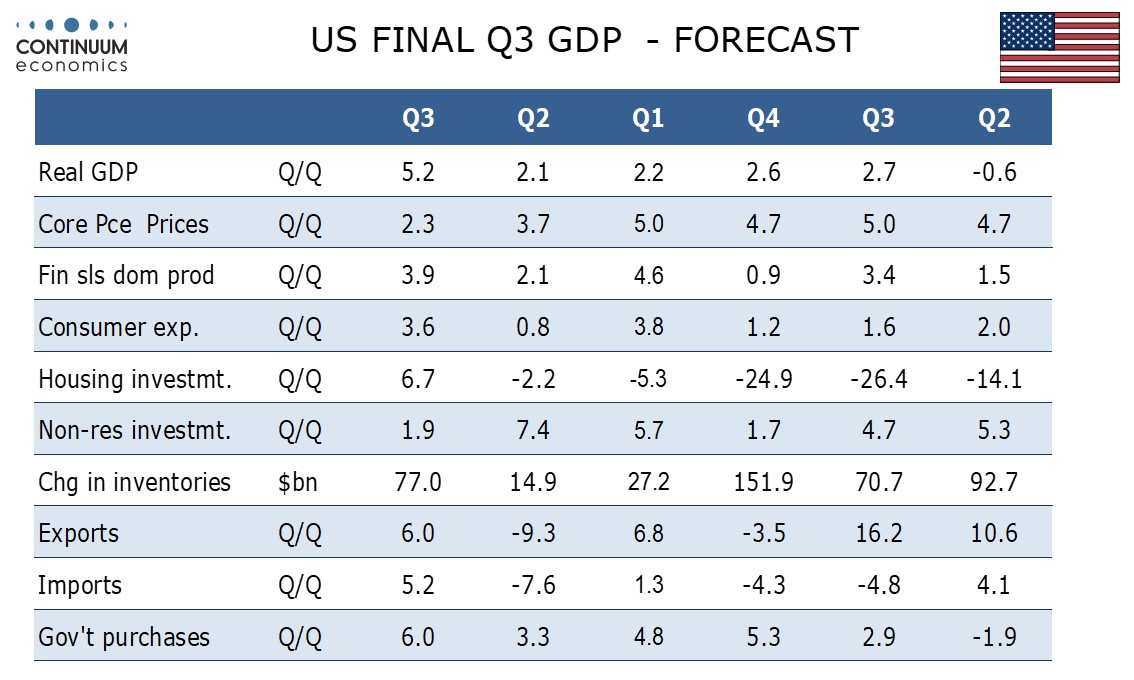

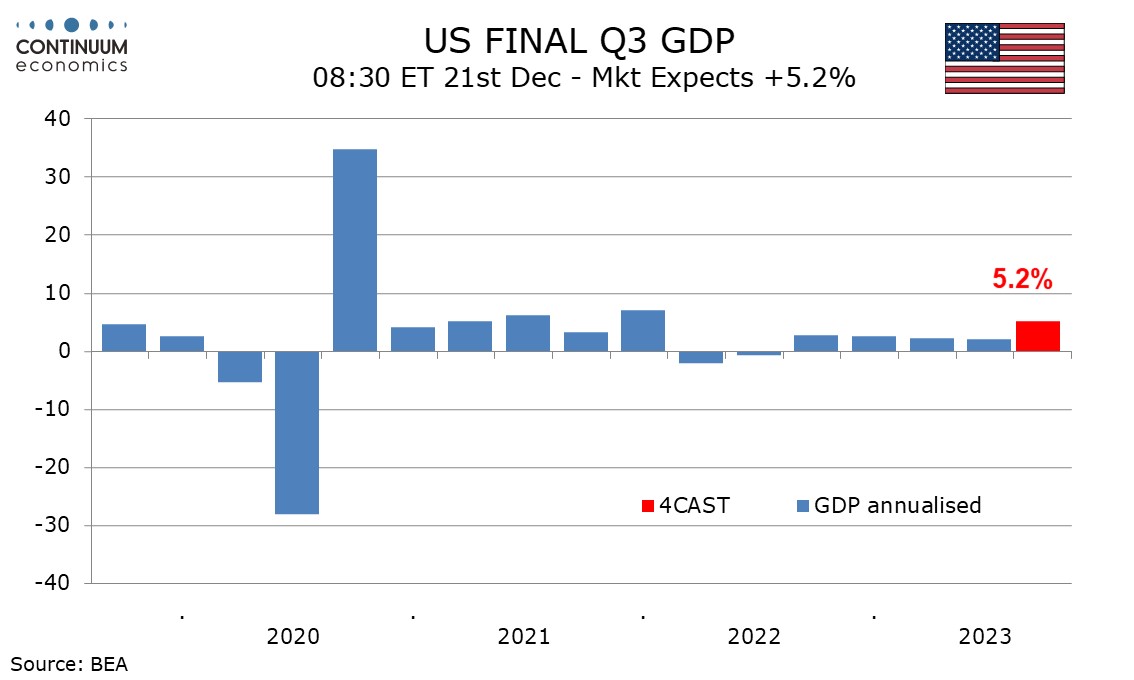

We expect the third (final) estimate for Q3 GDP to be unrevised from the strong second (preliminary) estimate of 5.2%. Momentum is likely to slow in Q4 though consumers remain resilient

.

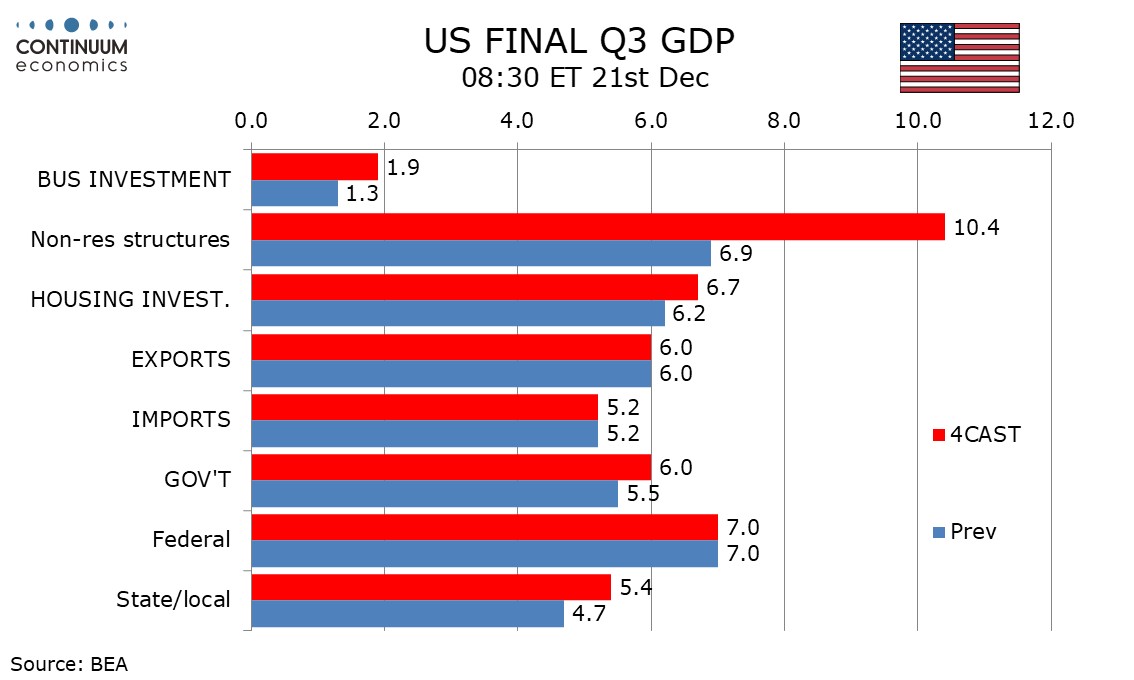

We expect an upward revision to construction, led by private non-residential, but with contributions also coming from housing and government, to be largely offset by a downward revision to inventories.

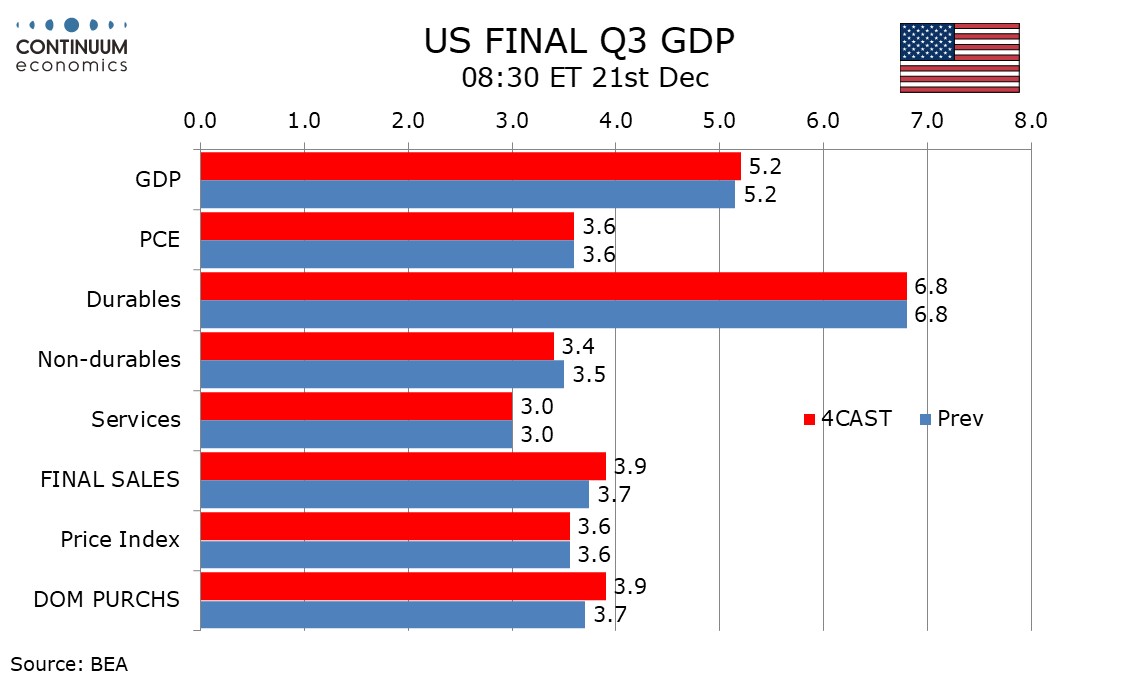

Final sales (GDP less inventories) is likely to be revised up to 3.9% from 3.7%. There will also be a marginal downward revision to non-durable consumer spending.

We do not expect any revisions to the price indices, from 3.6% for GDP, 2.8% for overall PCE and 2.3% for core PCE.