U.S. March PPI - Core rates pause after strong start to 2026

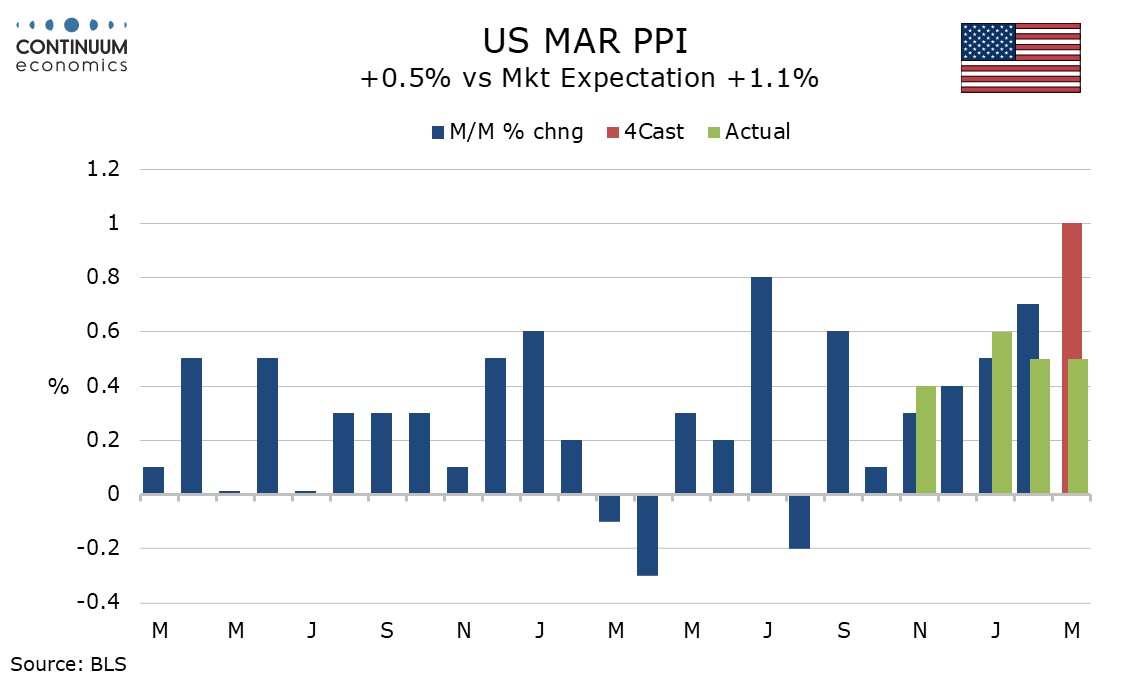

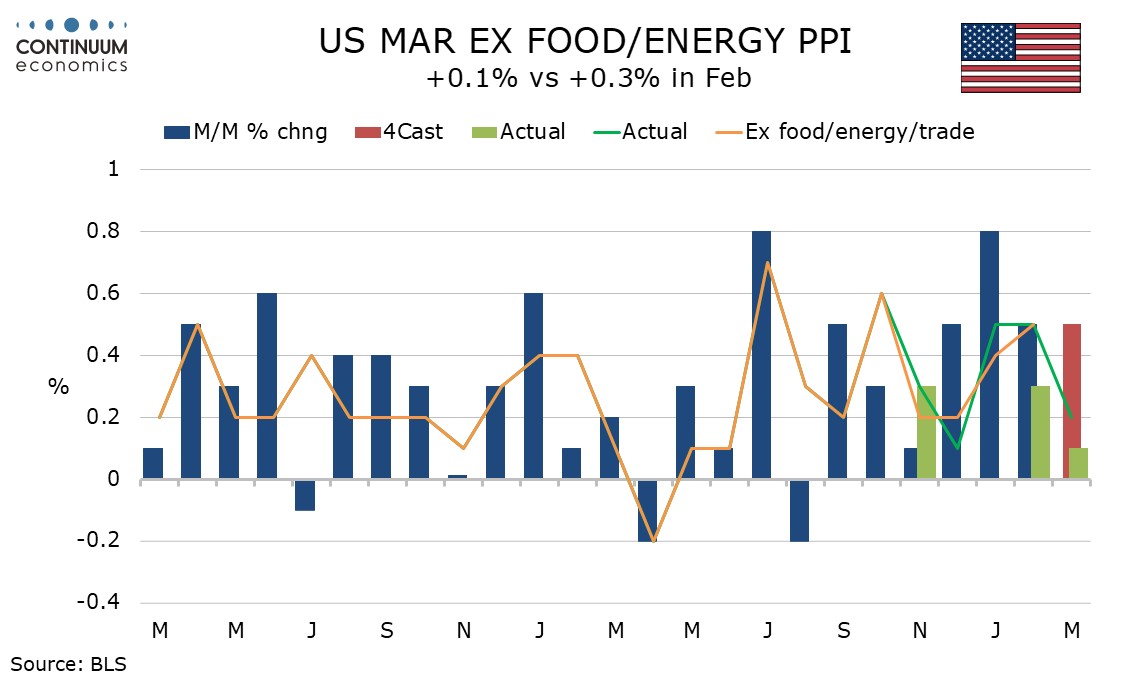

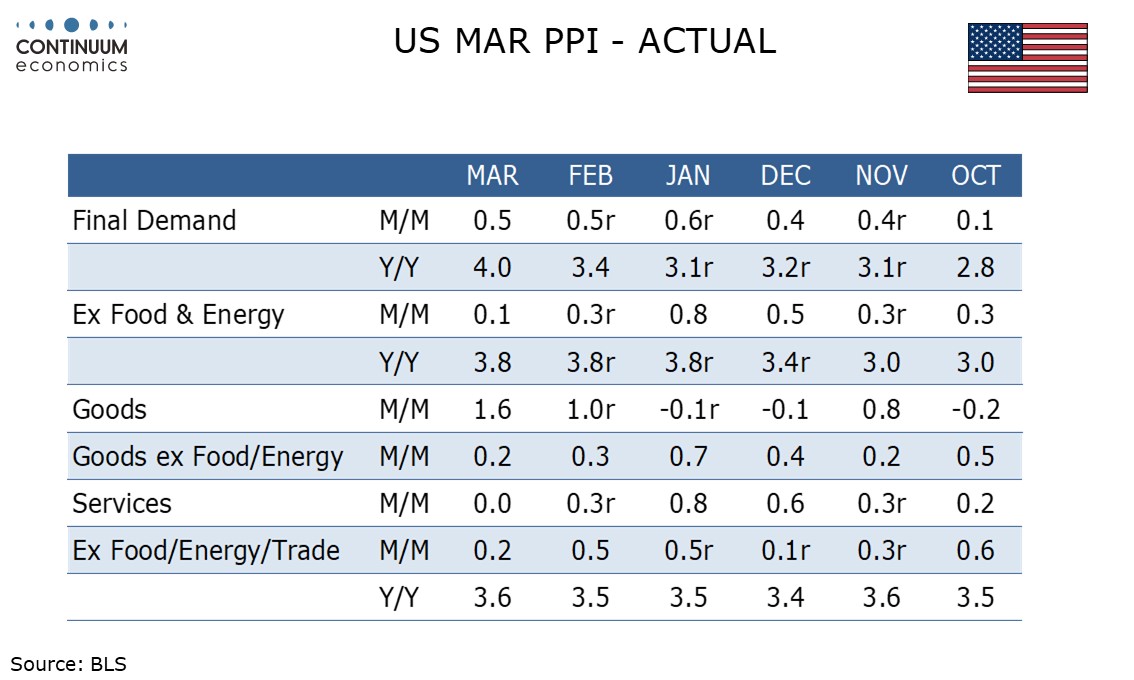

March PPI has come in significantly below expectations, up 0.5% overall with the core rates ex food and energy and ex food, energy and trade up only 0.1% and 0.2% respectively, pausing after strong gains seen in January and February.

Energy saw a strong 8.5% increase with gasoline up 15.7% though residential electric power and residential natural gas saw marginal declines. Foods slipped by 0.3% after a strong 2.4% increase in February. The PPI survey probably missed some of the gasoline price gains late ion the month, and further energy strength is likely in April.

Goods ex food and energy rose by 0.2%, the slowest increase since September, a hint that tariff feed through is starting to fade, while services were unchanged, their softest since a decline in August. Trade prices fell by 0.3%, a second straight modest decline after two straight surges of 2.0%. Transportation and warehousing was firm with a 1.3% increase which may be impacted by the situation in the Middle East, but other services rose by only 0.1%.

Yr/yr PPI rose to 4.0% from 3.4% reaching its highest since February 2023 but Yr/yr ex food and energy PPI was unchanged at 3.8%. Ex food energy and trade edged up to 3.6% from 3.5%, but has changed little in the last six months.

Intermediate detail was mixed. Processed goods with a 2.6% rise, 0.7% ex food and energy were firm, but unprocessed goods fell by 2.6% with energy correcting two straight strong gains that may have been impacted by weather, and ex food and energy up only 0.2%. Intermediate services fell by 0.1%, their first fall since April 2025.

March’s core PPI can be seen as corrective from recent months in which it has outperformed core CPI. Strength in PPI has also assisted core PCE prices to outperform core CPI. However, despite the soft overall core rates in March PPI, the components that continue to core PCE prices remain firm, most notably a sharp 4.1% rise in air transport, a feed through from the energy shock.