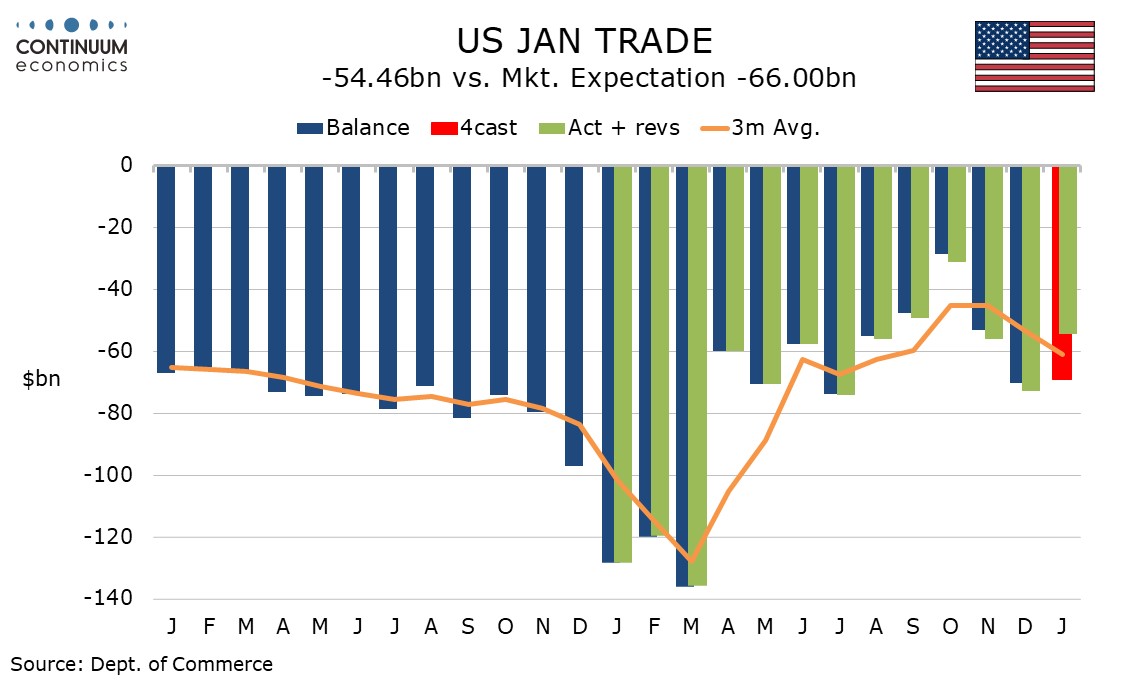

U.S. January trade deficit shows continued volatility, Initial Claims still low, January housing data mixed

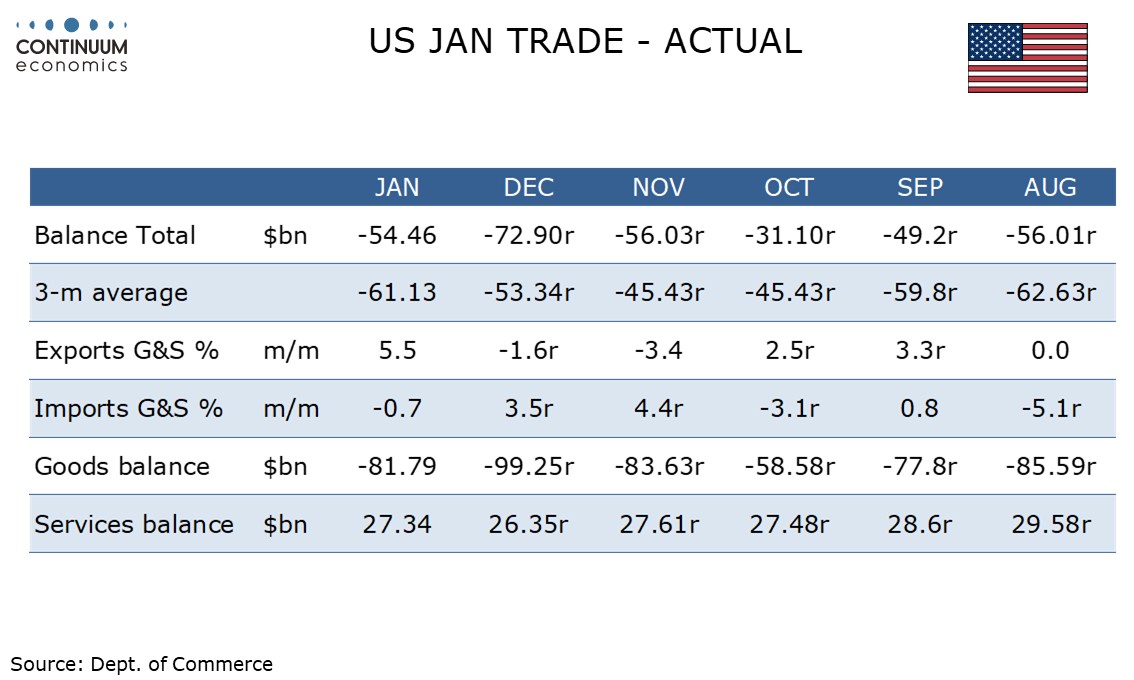

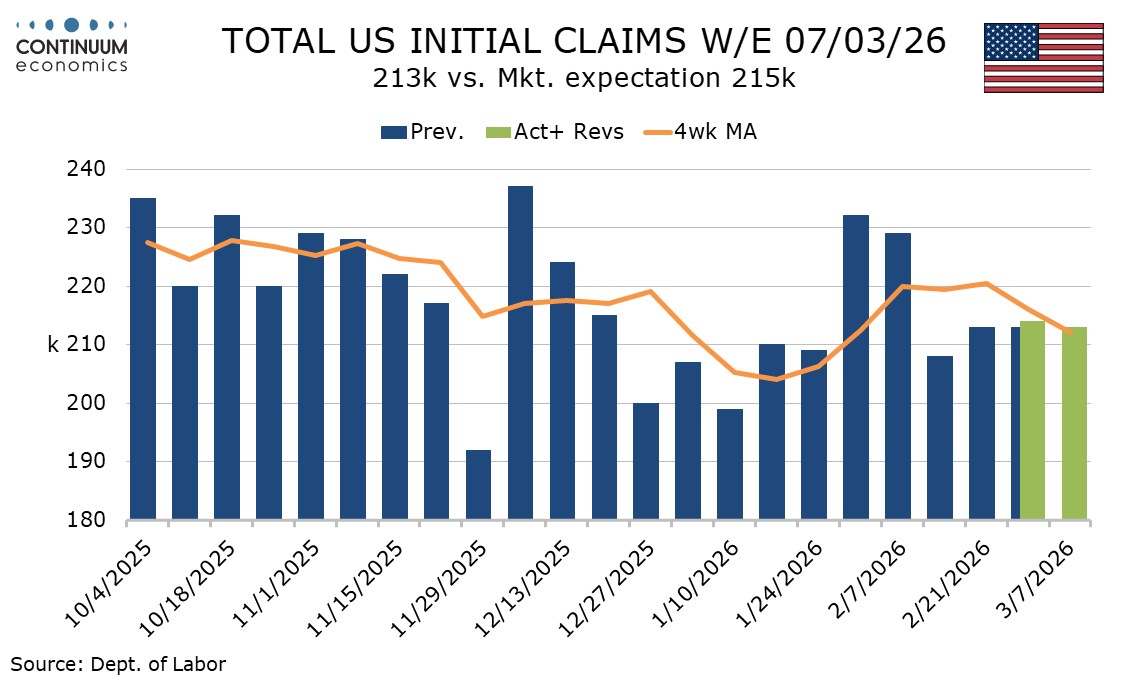

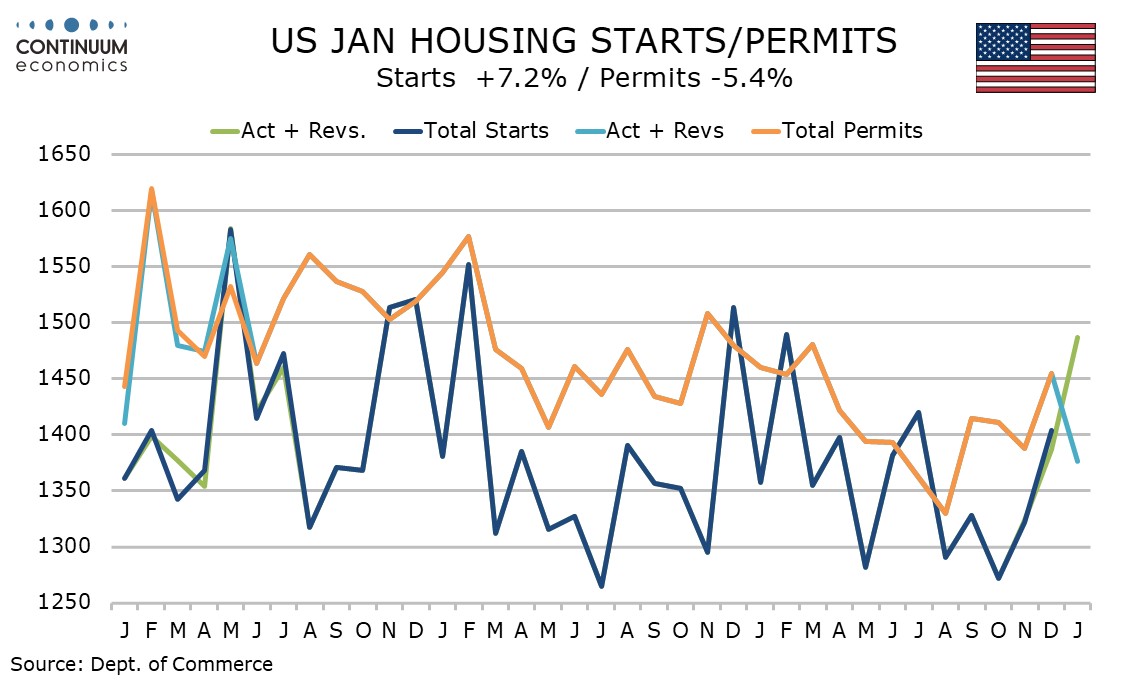

A significantly narrower US trade deficit on January of $54.5bn from $72.9bn is positive for Q1 GDP and led by a rise in exports, though the large swings in the deficit remain led by a few volatile items and trend is unclear. Initial claims at 213k from 214k remain low while January housing data is mixed, with a 7.2% rise in starts but a 5.4% fall in permits.

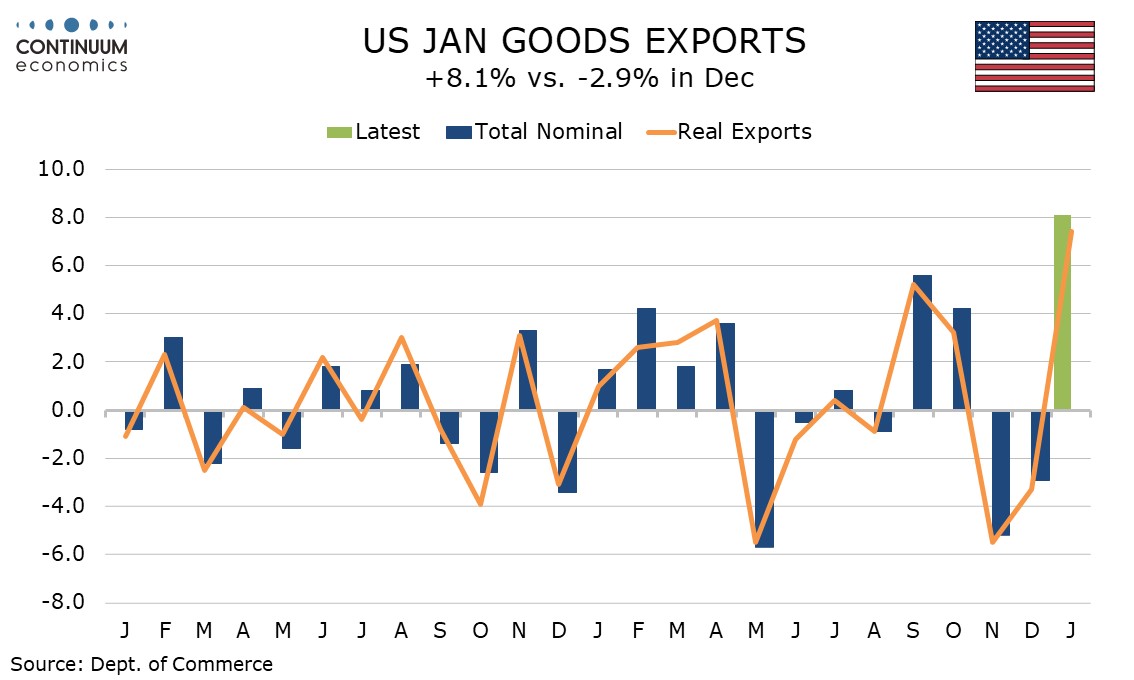

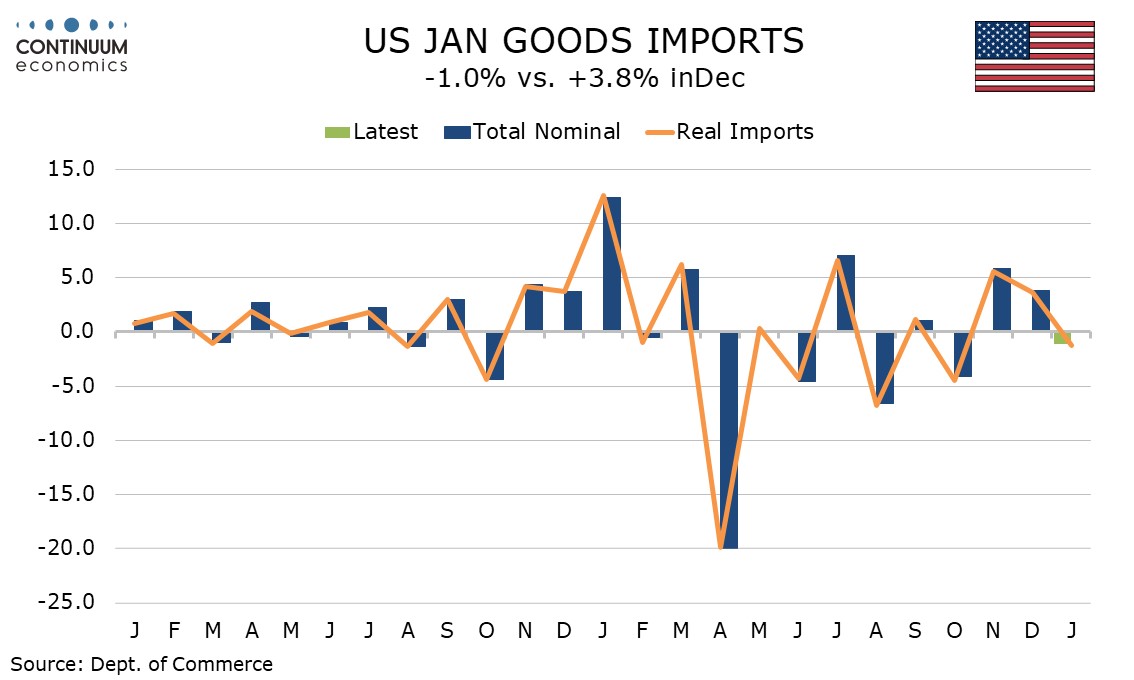

January’s trade data shows exports up by 5.5%, more than fully reversing two straight declines, while imports fell by a modest 0.7% after two straight strong increases. Goods showed a rise of 8.1% for exports but a fall of 1.0% in imports while services showed exports up by 1.2% but imports up by only 0.3%, the latter pausing after a strong 2.7% increase in December. The service surplus remains below November’s.

Exports increased by $14.6bn with nonmonetary gold up by $4.7bn and other precious metals up by $4.1bn, together explaining 60% of the increase. These components, particularly the former, have been very volatile recently, surging in October before slipping back in November and December. January’s strength brings the series back to what look like unsustainably high levels.

Also in the exports breakdown computers rose by $2.6bn which may be in part erratic but trend is strong, while pharmaceutical preparations, which have also seen high recent volatility, fell by $2.1bn. Imports saw little change overall but computers, by $3.9bn. saw an even larger rise than did computer exports, while pharmaceutical preparations saw an even larger fall, by $3.4bn, than did imports in the sector.

The bulk of January’s trade surprise thus comes from nonmonetary gold and other precious metal exports. Recent trend in the deficit is running below pre-tariff levels but it is not convincing that can be sustained in the longer term once exports of non-monetary gold and other precious metals stabilize.

Initial claims have seen very little change in the last three weeks and that is encouraging given that there has been some bad weather in those weeks. Next week will be the survey week fir March’s non-farm payroll and weather in that week has been unseasonably mild.

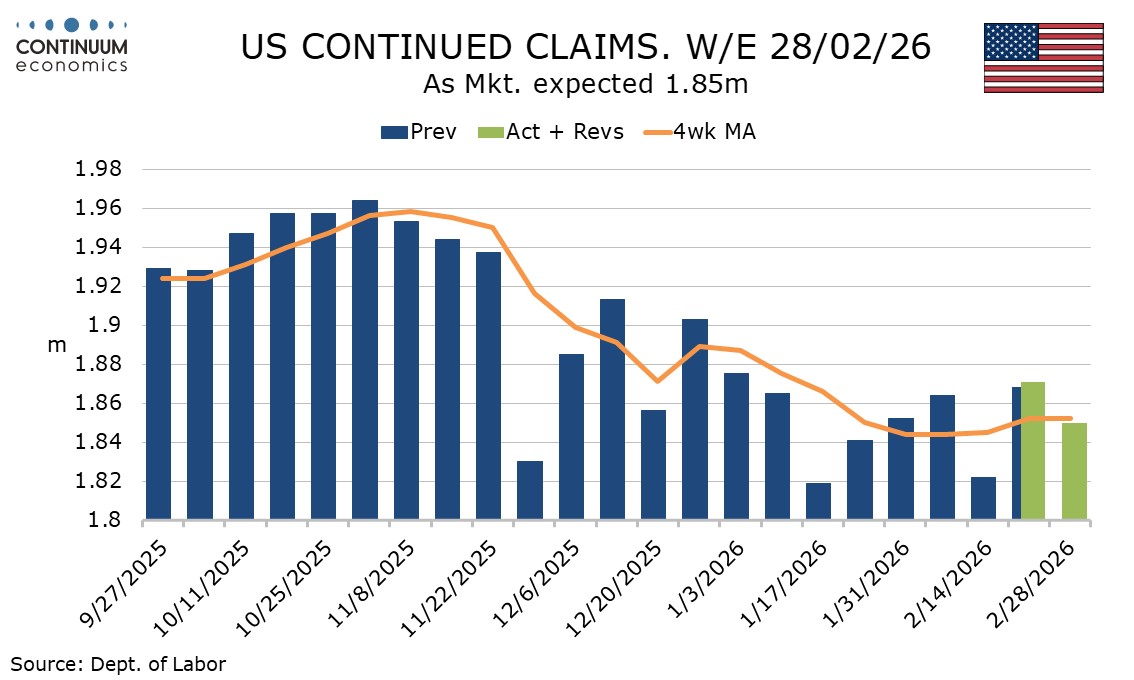

This suggests March’s non-farm payroll is unlikely to be as weak as February’s, which corrected an above trend January. Continued claims were also in line with expectations, down by 21k to 1.85m, and trend there appears to be stabilizing at lower levels than seen in late 2025.

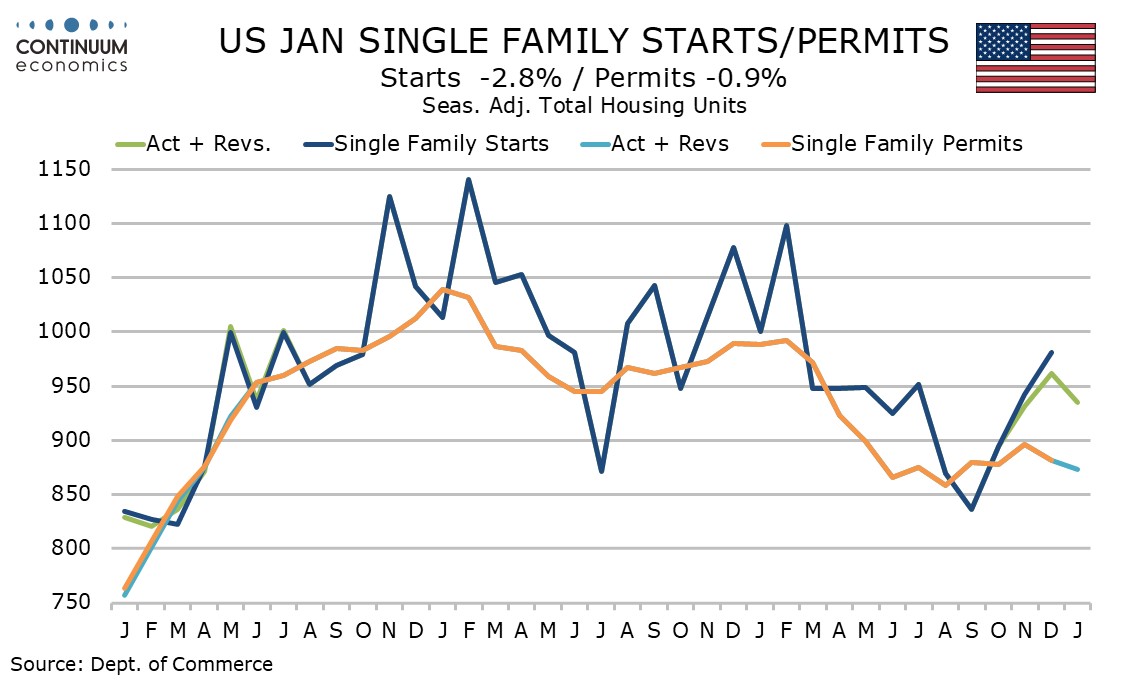

A 7.2% rise in January housing starts is the third straight and the level of 1.487m is the highest since February 2025. However the rise came fully in the volatile multiples sector which surged by 29.9%. Single starts fell by 2.8%, their first fall in four months.

Permits fell by 5.4% to 1.376m, with a second straight decline in singles, by 0.9%, while multiples fell by 12.4% after a 16.7% December increase. Overall the housing sector has no clear trend, but January’s data on singles is consistent with survey evidence suggesting a modest loss of momentum.