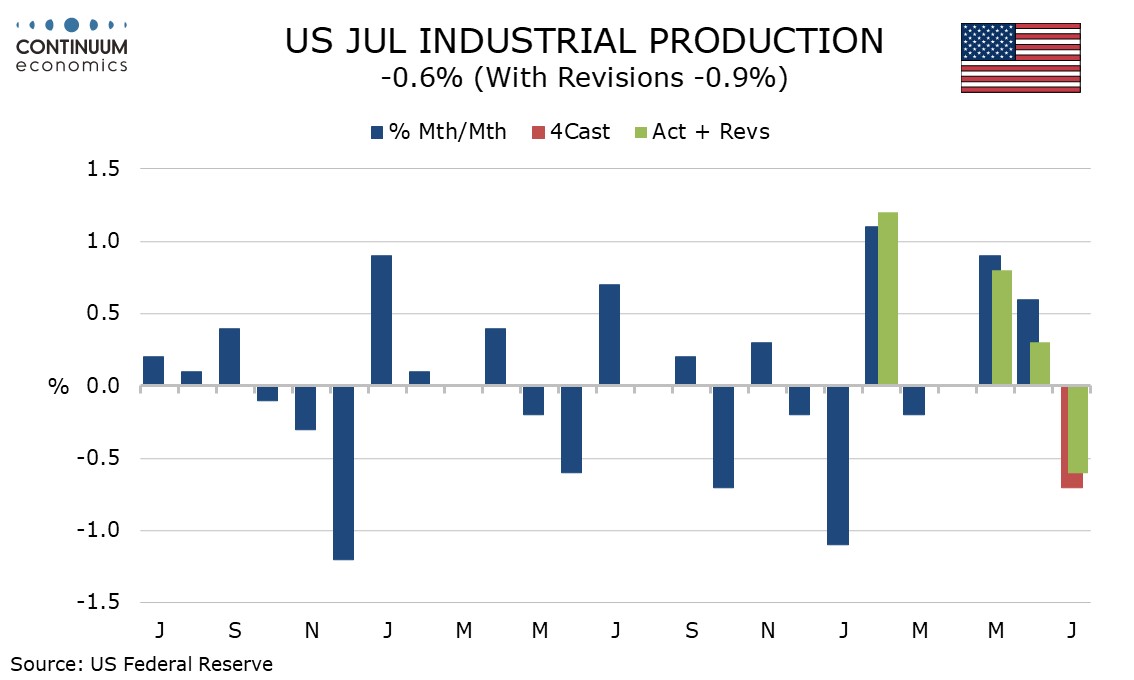

U.S. July Industrial Production - Weakness due to temporary factors

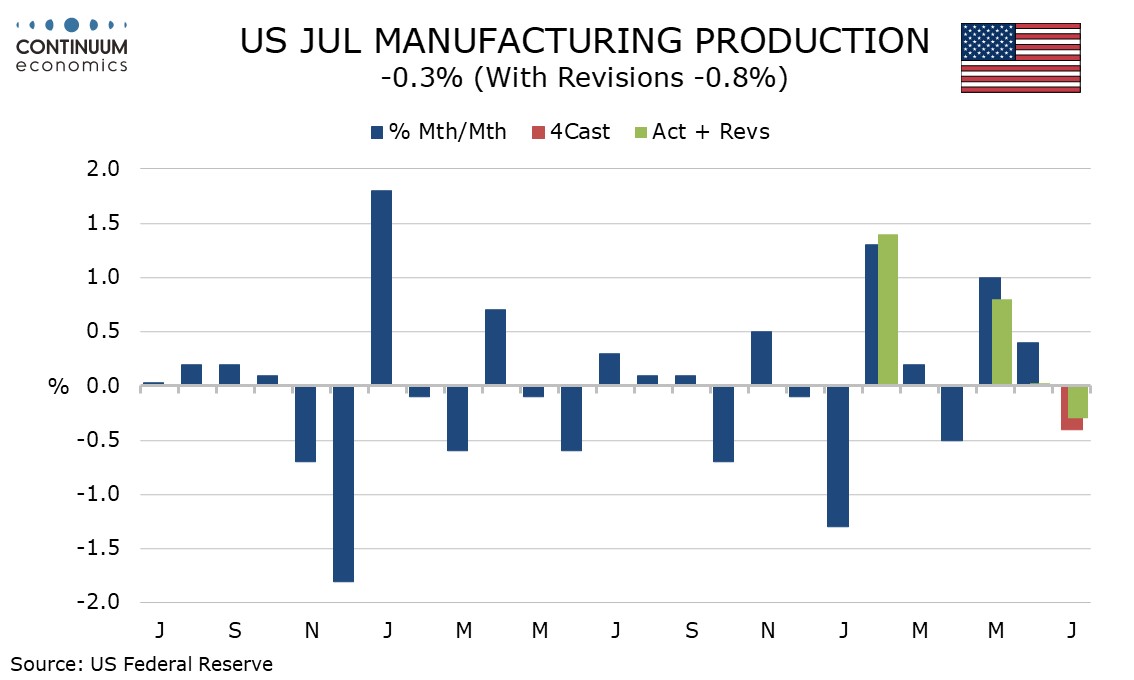

July industrial production is weaker tan expected at -0.6% overall and-0.3% for manufacturing with strong data in June seeing significant negative revisions, though Hurricane Beryl was seen as taking 0.3% off the July data, while a sharp drop in autos took 0.6% off manufacturing output, leaving the underlying picture looking slightly positive.

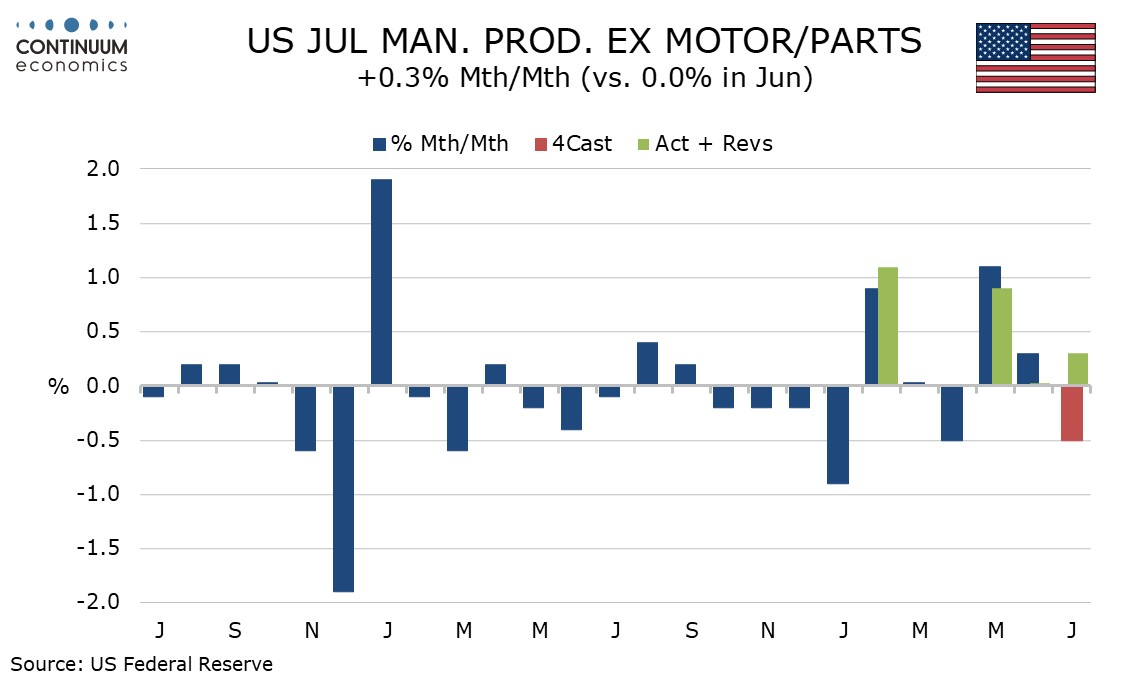

Manufacturing output ex autos increased by 0.3% despite the negative coming from Hurricane Beryl and this suggests an underling improvement from June data which was unchanged for both overall and ex auto manufacturing (revised down from gains of 0.4% and 0.3% respectively).

Weakness in autos is likely to prove temporary as July tends to see annual retooling shutdowns, which this July seem to have cut output by more than usual, though the impact is still likely to be temporary.

Weakness in autos is likely to prove temporary as July tends to see annual retooling shutdowns, which this July seem to have cut output by more than usual, though the impact is still likely to be temporary.

Mining, which we had expected to be sensitive to Hurricane Beryl, was unchanged. A 3.7% decline in weather-sensitive utilities needs to be seen alongside three straight strong gains.

Mining, which we had expected to be sensitive to Hurricane Beryl, was unchanged. A 3.7% decline in weather-sensitive utilities needs to be seen alongside three straight strong gains.

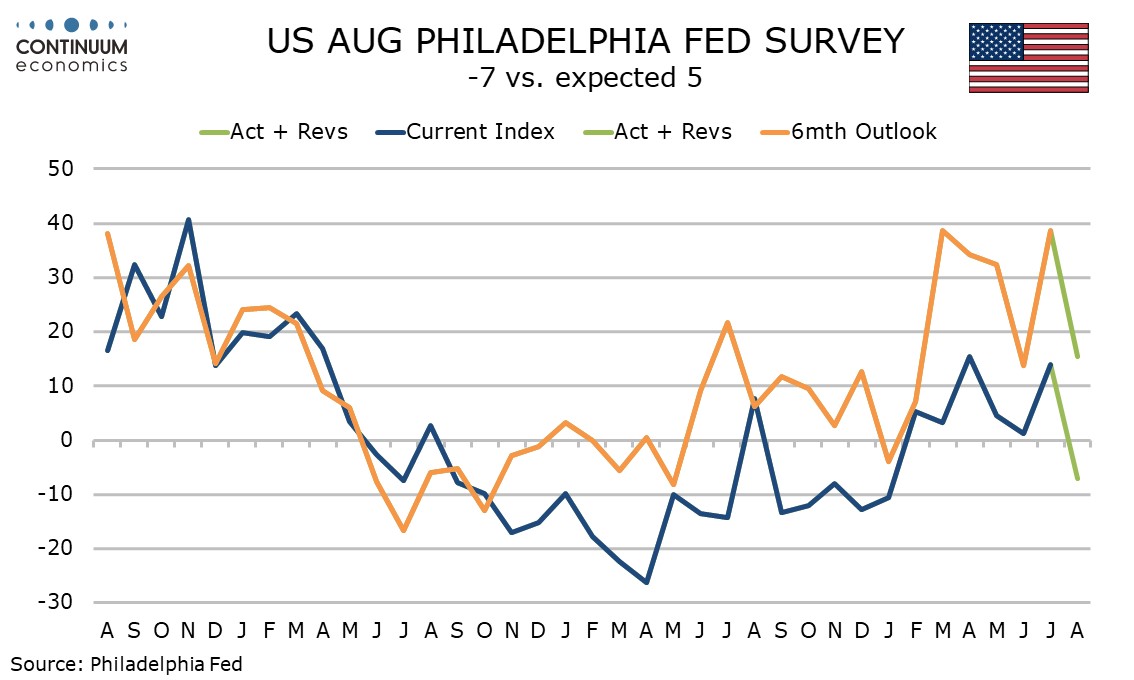

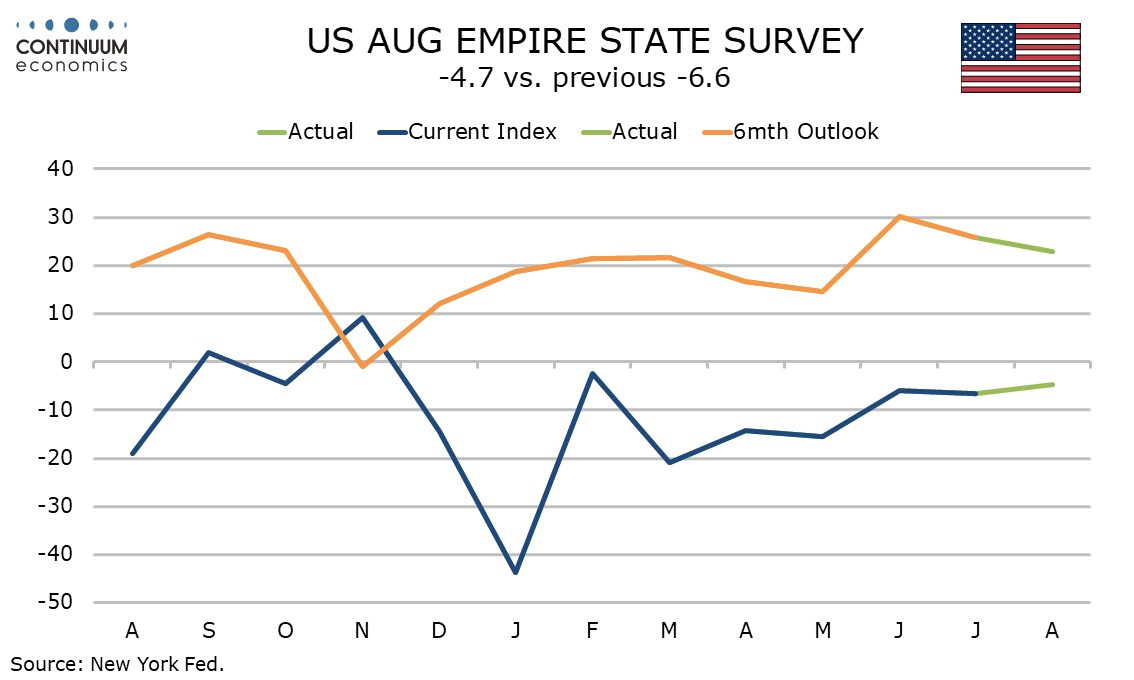

Weaker data for July is consistent with July manufacturing non-farm payroll details and July’s ISM manufacturing survey, but the industrial prediction report looks stronger in its details that the data noted above implied. Signals for August from the Philly Fed and Empire State surveys however do not suggest any underlying bounce in July will be extended.

Weaker data for July is consistent with July manufacturing non-farm payroll details and July’s ISM manufacturing survey, but the industrial prediction report looks stronger in its details that the data noted above implied. Signals for August from the Philly Fed and Empire State surveys however do not suggest any underlying bounce in July will be extended.

The Philly Fed index slipped to a 7-month low of -7.0 from June’s surprisingly strong 13.9 while the Empire State survey rose to a 6-month high of -4.7 from -6.6, leaving the two surveys more consistent and implyong a moderately negative underlying picture.

The Philly Fed index slipped to a 7-month low of -7.0 from June’s surprisingly strong 13.9 while the Empire State survey rose to a 6-month high of -4.7 from -6.6, leaving the two surveys more consistent and implyong a moderately negative underlying picture.

Detail shows the contrast between the surveys persisting for new orders, with the Philly Fed’s firm at 14.6 but the Empire State’s weak at -7.9. For 6-month expectations, the Empire State’s little changed 22.9 reading is now stronger than a weaker 15.4 for the Philly Fed.

Detail shows the contrast between the surveys persisting for new orders, with the Philly Fed’s firm at 14.6 but the Empire State’s weak at -7.9. For 6-month expectations, the Empire State’s little changed 22.9 reading is now stronger than a weaker 15.4 for the Philly Fed.

Philly Fed prices data showed slightly stronger prices paid but slower prices received and a significant slowing for 6-mnth price expectations. The Empire State’s price indices did not see much change, but were slightly weaker for the current month and slightly stronger on a 6-month view. These findings are reasonably consistent with those for activity in both surveys.

Philly Fed prices data showed slightly stronger prices paid but slower prices received and a significant slowing for 6-mnth price expectations. The Empire State’s price indices did not see much change, but were slightly weaker for the current month and slightly stronger on a 6-month view. These findings are reasonably consistent with those for activity in both surveys.