FX Daily Strategy: Europe, July 26th

FX market dominated by fluctuating risk sentiment

Much of the JPY gain reflects a big overshoot since early May, but JPY remains undervalued

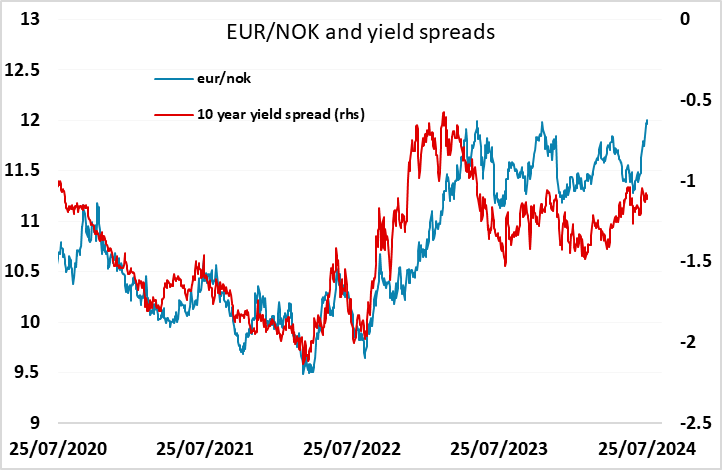

Risk positive currencies may now be oversold, notably NOK

Tokyo CPI may determine risk tone on Friday

FX market dominated by fluctuating risk sentiment

Much of the JPY gain reflects a big overshoot since early May, but JPY remains undervalued

Risk positive currencies may now be oversold, notably NOK

Tokyo CPI may determine risk tone on Friday

The FX market has been very risk sensitive this week, with the JPY and CHF managing general gains on the unwinding of risk and yield positive carry positions. Thursday saw an initial sharp risk off move in Asian hours followed by a risk recovery after the US GDP data. EUR/USD moved very little, but the commodity currencies all initially fell against the USD in the “risk off” period, with the JPY and the CHF gaining, and these moves were reversed on the risk recovery on the data. The moves were all about risk and positioning, and very little about value. Nor was the initial risk negative mood triggered by any specific event, although a continued pessimism about Chinese growth prospects has underpinned much of the correction lower in equities. While the risk recovery in FX was initially accompanied by a mildly positive equity market response, this quickly faded and the equity tone remained weak through the end of the European day, with yields in the US and Europe also lower.

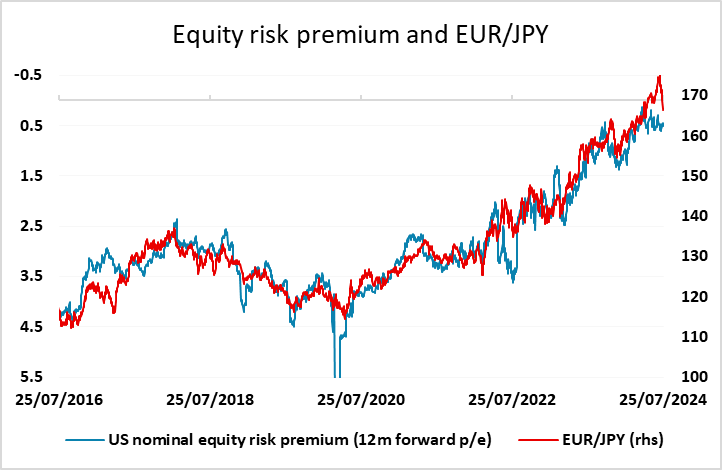

What we are seeing here is not really a response to particular events or data, but a correction to the general risk positive trading bias seen in the first half of the year. The seeds of this correction were already present several months ago, as yield spreads started to move in favour of the JPY, but the positive carry trades were supported by continuing rise in equities and decline in equity risk premia. However, JPY weakness started to overshoot even these measures after the BoJ intervention at the end of April, and the current JPY recovery is largely correcting this excess.

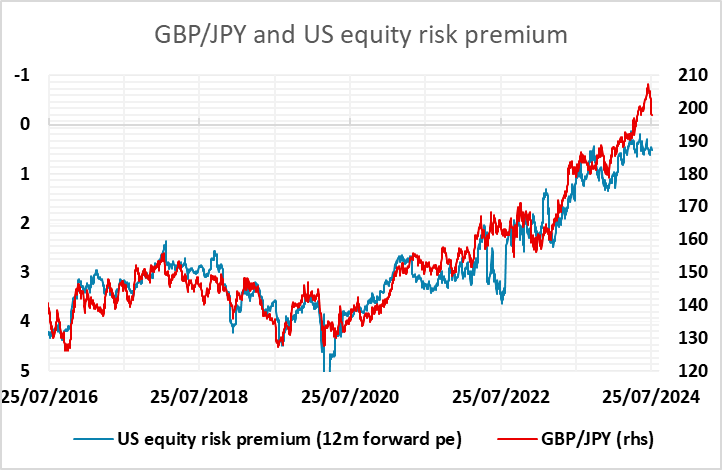

From here, the correlation with equity risk premia suggests there is still a little more downside in EUR/JPY and other JPY crosses. The better than expected US Q2 GDP data has for the moment staunched the bloodletting, but we are likely to require more evidence of better global growth if the JPY’s rise is not to resume. The US numbers have been slowing, but remain significantly better than the European data, where the weakness of the recent PMI data casts some doubt on hopes of a recovery this year. We still see a move to the low 160s in EUR/JPY and the low 190s in GBP/JPY before this phase of JPY recovery is over. And we would emphasise that this is only the first phase of the JPY recovery. The JPY remans hugely undervalued, and in the next couple of years we are likely to see USD/JPY back down to 125. But the next phase is likely to accompany significant rate cuts in the US and Europe, and may begin in September when the Fed is likely to ease for the first time this cycle.

However, the JPY is a different story to most currencies because it has weakened so much over the last few years. Other risk sensitive currencies have also moved sharply this week. The NOK is one of the most notably weak currencies, with EUR/NOK reaching a new all time high on Thursday (pandemic spike excluded), having failed to benefit from the risk positive tone in the first half of the year (and previous years). This looks anomalous, and the AUD has also probably fallen too far due to its connection with China demand and Asian risk sentiment.

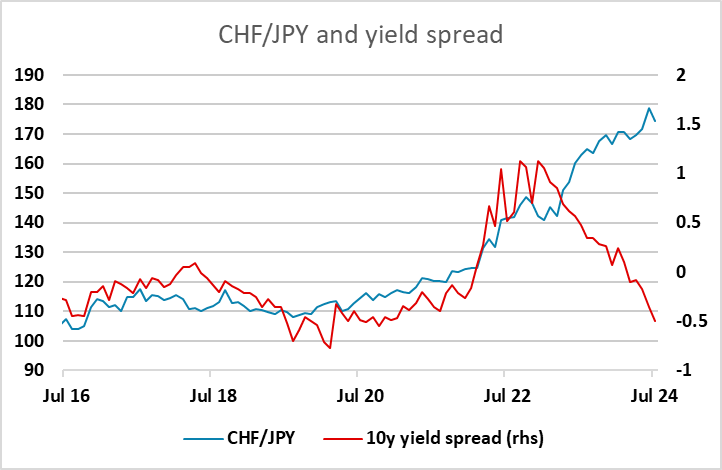

For Friday, the tone might be set by the Tokyo CPI data due out at the beginning of the Asian session. There is more focus on the BoJ meeting next week after the JPY’s sharp recovery, which was also helped by comments from a senior LDP politician calling for a more hawkish BoJ stance and a stronger JPY. The market has gone from pricing a BoJ rate hike as a 40% chance to around a 65% chance. We still suspect they will wait until the September meeting, given the weakness of consumer spending, but strong Tokyo CPI could re-ignite JPY strength. If so, we still see the clearest value trade as being against the CHF. The low JPY valuation is much clearer than the case for weaker risk assets, and the CHF should be more vulnerable at these levels to any risk recovery.