FX Daily Strategy: N America, July 24th

PMIs the main focus on Wednesday

USD strength can extend if relative US PMI strength continues

EUR and GBP may both be vulnerable against the JPY

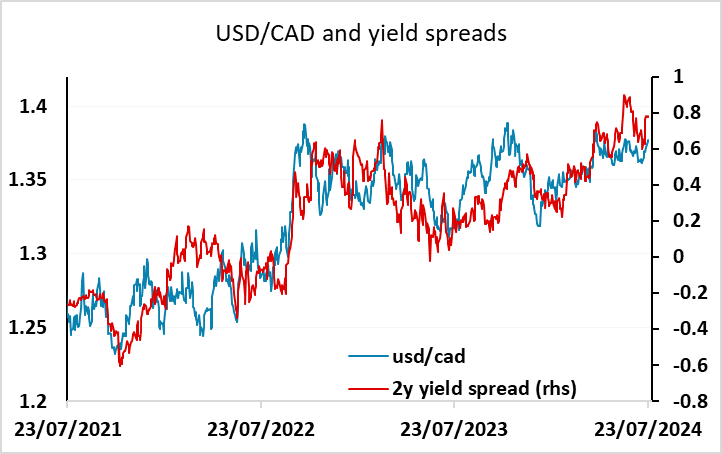

CAD has upside scope with the market overpricing the risks of a BoC rate cut

PMIs the main focus on Wednesday

USD strength can extend if relative US PMI strength continues

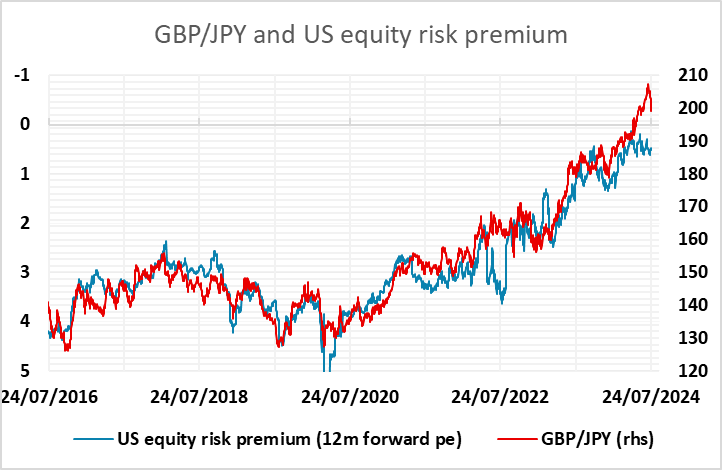

EUR and GBP may both be vulnerable against the JPY

CAD has upside scope with the market overpricing the risks of a BoC rate cut

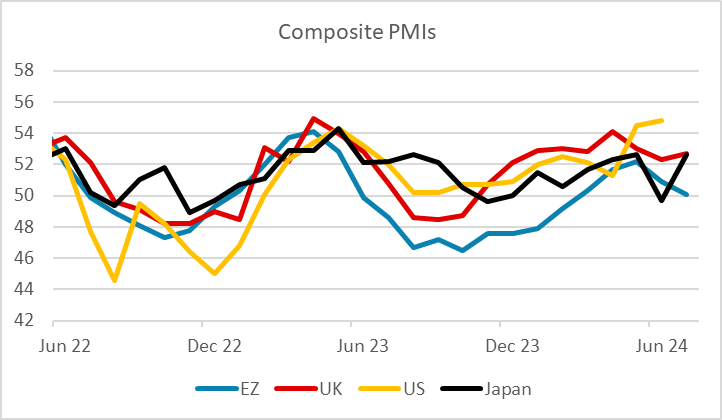

Wednesday is PMI day, with the focus likely to be on whether the recent relative strength of the US PMIs persists, and the relative weakness of the Eurozone PMIs. The weakness of the Eurozone continued in July, with the composite index dropping to 50.1, its lowest since February. UK PMI came in broadly as expected, but relatively strong compared to the Eurozone. EUR/GBP is consequently once more pressing on the 0.84 level. EUR/USD dipped on the Eurozone data, but the decline has so far been relatively modest.

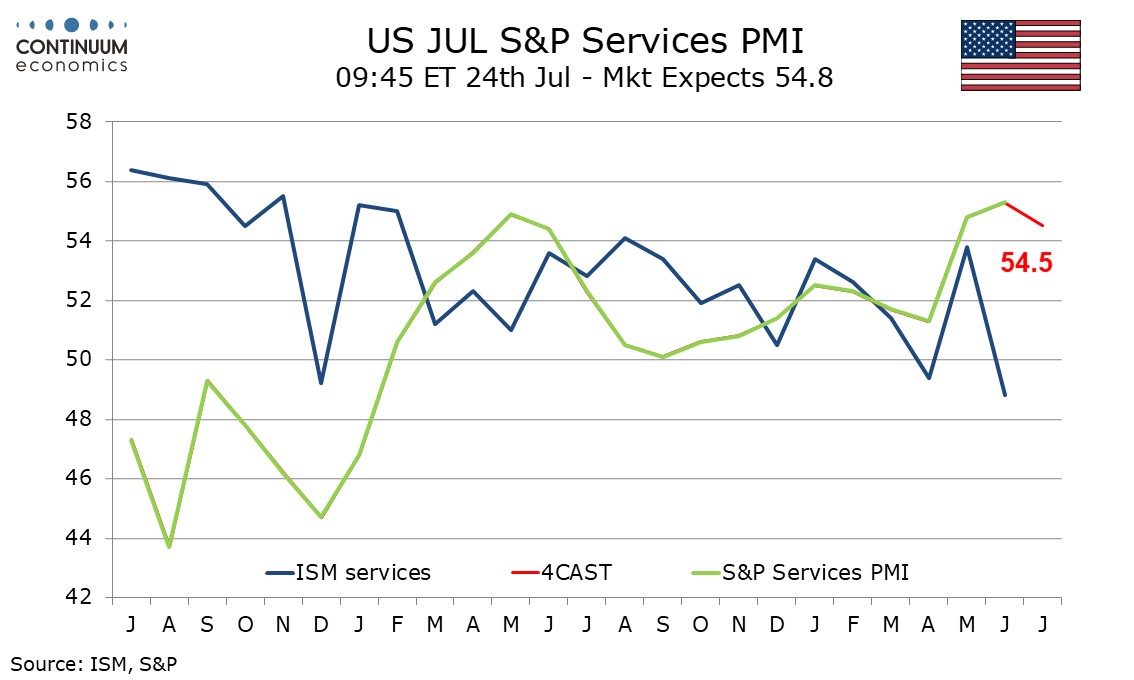

There is scope for volatility on the release of the US numbers, which have been relatively strong of late. A continuation of this would likely mean a EUR/USD test of 1.08, but there is a significant risk of a sharp correction lower in the US PMI as the ISM survey has been much weaker.

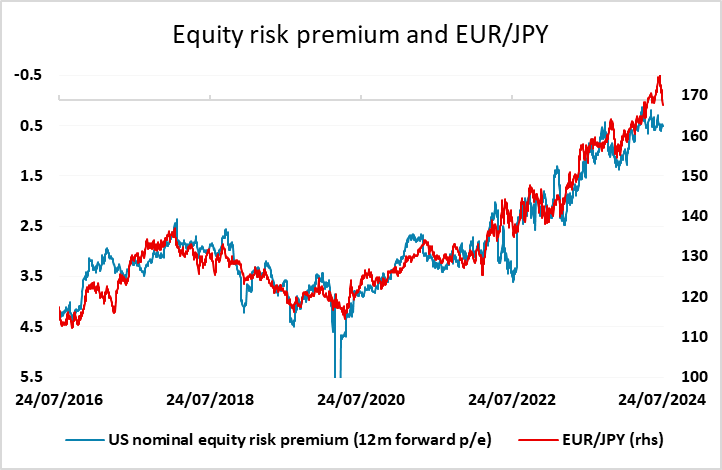

The JPY was once against the strongest of the major currencies on Tuesday, with JPY crosses catching up with the weakness in USD/JPY already seen, and JPY gains have extended overnight. For EUR/JPY, the correlation with equity risk premia suggests scope back to the mid-to low 160s, while for GBP/JPY there looks to be scope for a move to the low 190s based on the same correlation. The CFTC data on net speculative positioning in the futures market suggests net long GBP positions are particularly extended, and GBP valuation also looks particularly highs against the EUR and JPY. GBP/JPY could therefore be the most vulnerable to any negative news, either specifically on the UK or more generally on global risk. While there are some reasons for optimism about UK growth prospects under the new government, we doubt there will be much near term pick-up so current sentiment is likely too positive.

We also have the Bank of Canada meeting on Wednesday. A rate cut is 90% priced for the BoC meeting, and around 75% of forecasters are looking for a rate cut. So there would not be much impact on the market if the BoC do cut rates. But we expect the BoC to surprise the market by leaving rates unchanged. Given market pricing, the risks for USD/CAD should be substantially on the downside, with limited upside on a rate cut, and substantial downside if rates are left unchanged. As it stands, USD/CAD could still have some upside risks based on current yield spreads, but the USD is somewhat expensive from a longer term perspective, and there is scope for USD/CAD to drop a figure or more if the BoC leave rates unchanged.