Eurozone: Credit Weakness Deepens Afresh

The ECB faces an important few weeks, not least with the looming policy assessment and projection update due on Mar 7. Some downgrade to the real economy and inflation outlook (at least for the next 1-2 years) seems to be on the cards, albeit where the ECB hawks may regard the extent of any downward revisions to the real activity picture may be limited given the better PMI business survey data seen of late. If so, we think this again would be the ECB being complacent, given what are shortcomings in the PMI data. Indeed, while there is no hard activity data so far this year to make any judgement to assess how this year may fare, the latest ECB compiled credit and deposit data suggest downside risks remain and may even be deepening (Figure 1), with it looking more the case that this reflects not only ECB rate hikes but balance sheet reduction too (Figure 2).

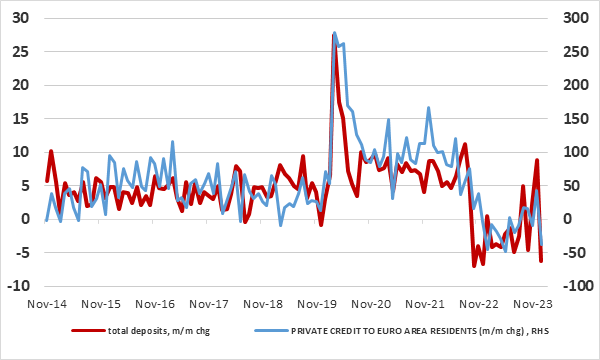

Figure 1: Private Sector Credit and Deposit Levels Fall Afresh

Source: ECB, Euro billions

Mixed Monetary Messages?

At the Jan 24-25 Council meeting, members did suggest that existing real economy projections may need to be pruned back or at least necessitate some deferral of the timing of any perceived recovery. But solace was taken from what was seen to be less-weak credit dynamics. It was accepted that the ECB’s restrictive monetary policy had been strongly transmitted to financing conditions for firms and households, and that even if rates on new lending might be reaching a turning point, much of the repricing of the existing stock of loans at higher rates remained in the pipeline. But it was agreed that credit dynamics had improved somewhat even if they remained weak overall. On the credit supply side, it was argued that weak incentives for bank lending might also have played a role. Banks had attractive alternative ways of putting their liquidity to work, including by investing in bond markets and placing funds in the ECB’s deposit facility. At the same time, it was pointed out that monthly lending flows to firms had reached their highest level in more than a year and loans to households had picked up could be an indication that credit dynamics might be close to a turning point, and that the peak of monetary transmission to bank lending volumes might have been reached.

Credit Dynamics not so Dynamic?

However, January’s money and credit data very much refute such thinking. They showed not only a further and deeper fall in bank deposits but also a fresh m/m drop in adjusted private sector loans, ending a five-month run of increases (Figure 1). Perhaps as important was that the drop in credit levels (trimming overall y/y growth to barely positive 0.4% and strongly negative in real terms at circa -3%) reflected fresh falls in both household and company lending, this very much in conflict with the hopes aired at the January Council meeting. We for some time have underscored how important the monetary data are as they reflect both the direct impact of the ECB’s aggressive conventional policy hiking but also the impact of its balance sheet reductions, in other words refuting the central bank assertion that its QT policy is largely working in the background and not affecting real or nominal activity.

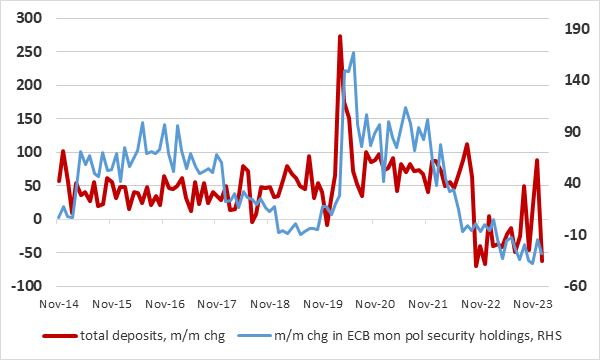

Figure 2: Bank Deposit Drop Linked to ECB Balance Sheet Swings

Source: ECB, Euro billions

In particular, it is clear that rate hikes have curbed loan demand and with the ECB analysis (see above) accepting more of an impact to come. Bu we think that the reduction in the balance sheet, most notably from the on-going and now stepped-up bond sales program is having an impact on both commercial banks willingness and possibility ability lend as those purchasing the bonds are drawing down on deposits to pay for them. Indeed, it is noteworthy that bank deposits have shrunk some 2% (nominal) from their end-2022 peak, an unprecedented development. Moreover, these m/m falls in bank deposits (nine in the last year), are very much correlated with the QT program, namely the reduction in the holding of securities on the ECB balance sheet (Figure 2).

Admittedly, not too much emphasis should be placed on one monthly set of data such as these January monetary figures. But the point here is that they do reinforce a sobering picture of credit dynamics dating back will into 2022 that has helped us identify ensuing weakness in both real and nominal activity; the weakness in monetary growth very much tallying with the slump back in HICP inflation which has surprised the ECB in its recent extent. Overall, the money and credit data very much suggest to us that the ECB has presided of an increase in the cost of credit but also a reduction ion its supply, both of an unprecedented nature.