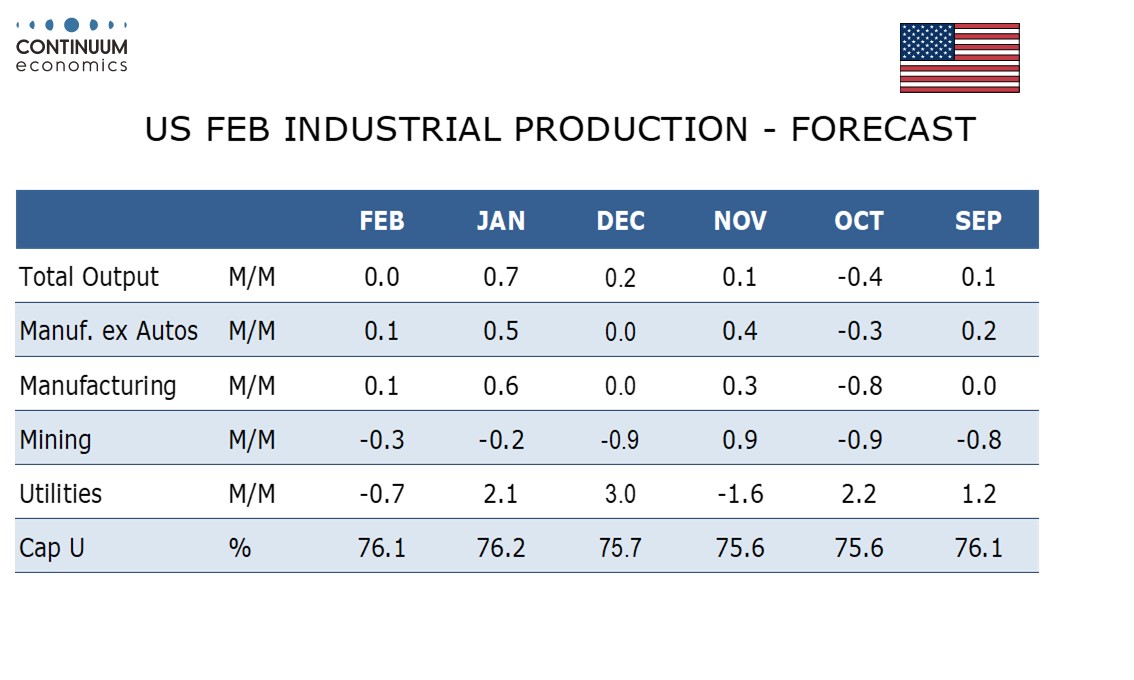

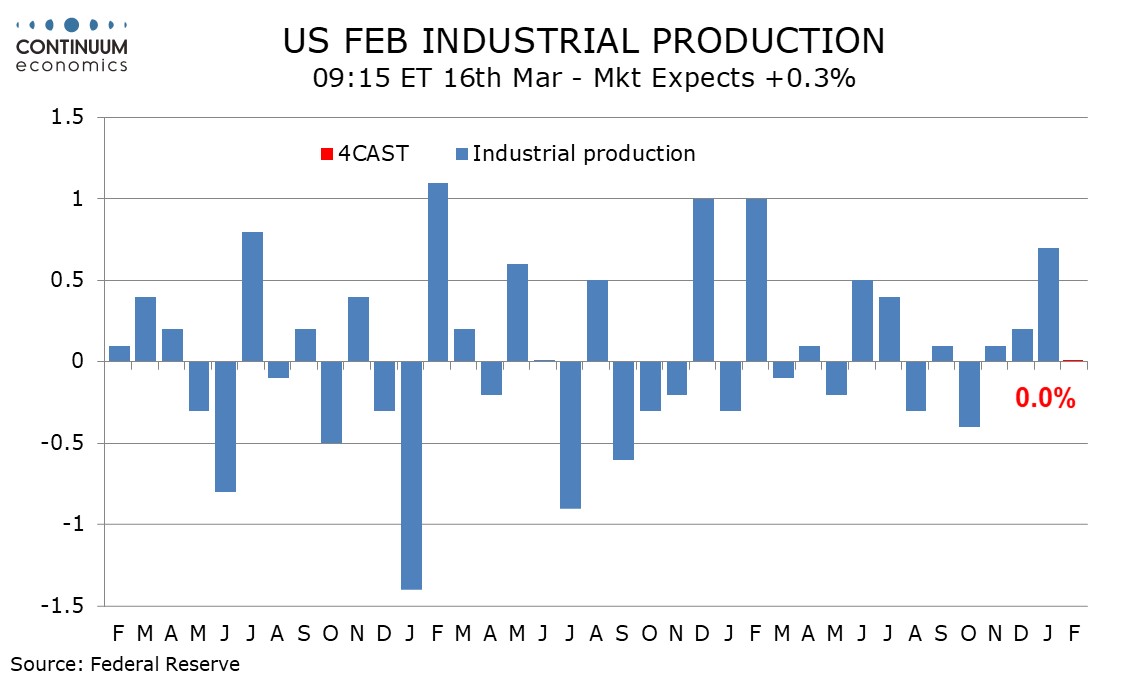

Preview: Due March 16 - U.S. February Industrial Production - Pause after a stronger January

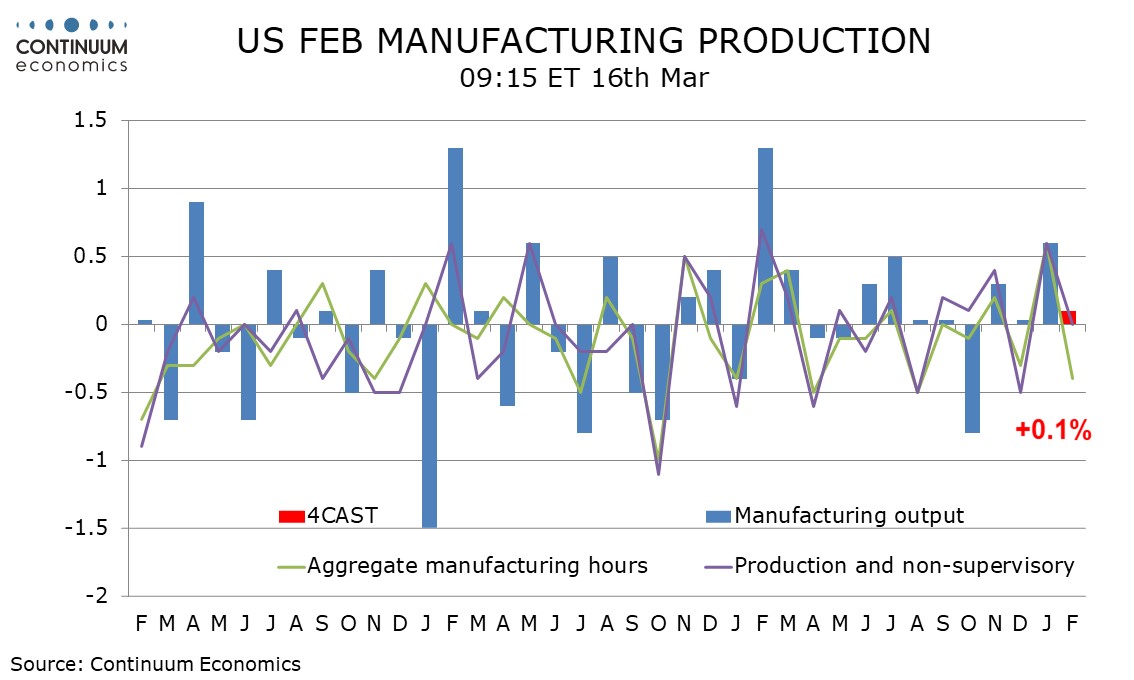

We expect an unchanged February industrial production total to follow a strong 0.7% increase in January. For manufacturing we expect a 0.1% increase to follow a 0.6% rise in January. Despite the subdued February forecast, trend appears to be picking up.

A second straight strong ISM manufacturing index, backed by several other recent manufacturing surveys, was contrasted by a 0.4% decline in aggregate manufacturing hours worked in February’s non-farm payroll breakdown. Still for production and nonsupervisory manufacturing workers aggregate hours worked were unchanged, suggesting manufacturing output will be able to marginally extend a strong January increase.

We expect mining to sustain a marginally negative trend and payroll data for mining is consistent with that. Weather-sensitive utilities output is likely to correct from two straight strong gains, though not sharply with weather remaining cold in much of February.

We expect capacity utilization to slip to 76.2% from 76.1% overall and to 76.6% from 76.6% for manufacturing. Trend has little clear direction but may be starting to pick up.