This week's five highlights

Iran Conflict Persists

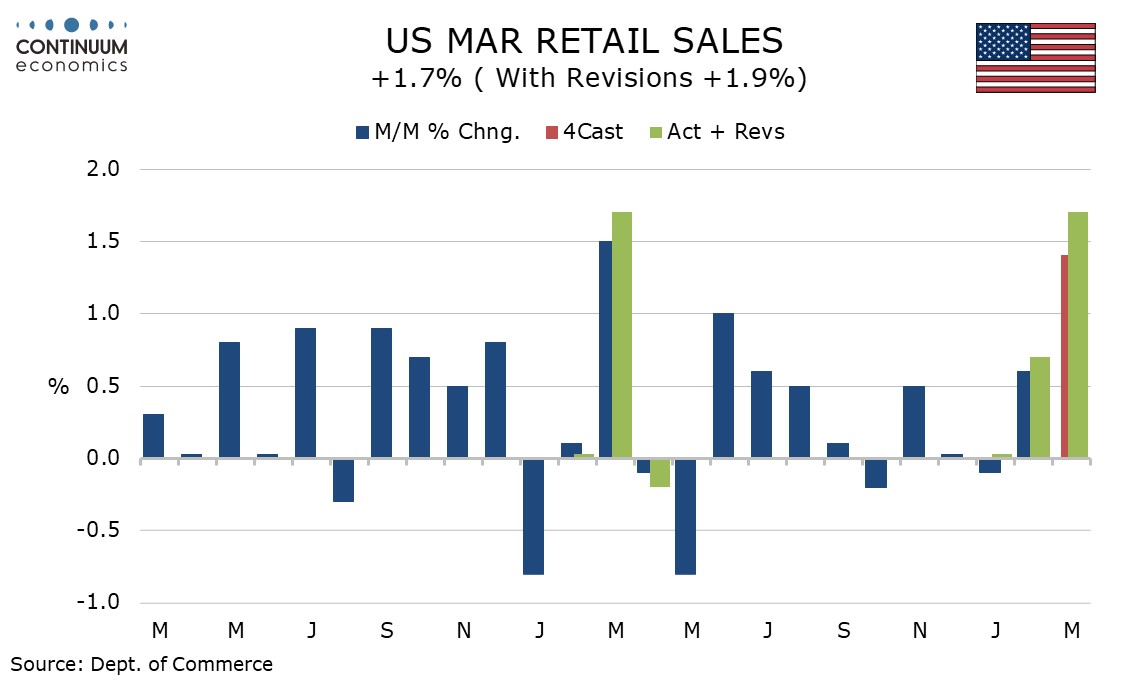

U.S. March Retail Sales Show Underlying resilience

DXY Pushing higher

UK Inflation Being Fuelled But Wages Still on the Wane

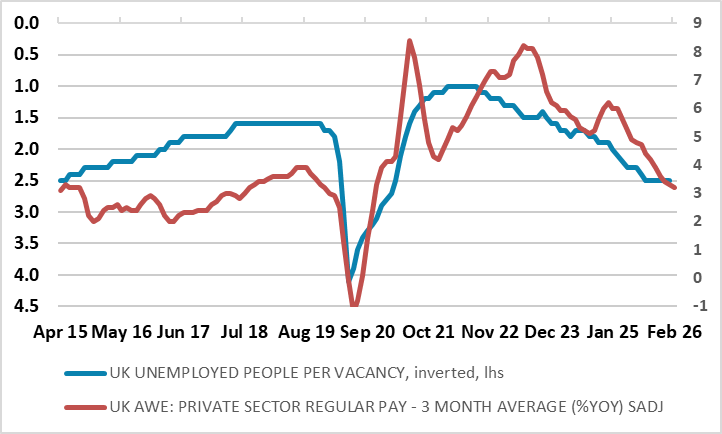

UK Labor market Hemorrhaging

Seemingly the ceasefire has been extended, not surprising given Trump’s repeated about-turns (even on Tuesday alone) and the fact that both Iran and the US want peace, the latter enough to temper any attempt by Israel to resume hostilities ahead of its election due later this year. Each side has an obvious different rationale for this; Iran is exhausted economically and militarily while the U.S knows the growing risks to it and the world economy if the Straits remain effectively closed, blocking off oil and other vital commodities. Meanwhile, the U.S is realising at least implicitly that it has persistently over-estimated its ability to use its undoubted military superiority to reach its goals regarding Iran. But the U.S still seems to be over-estimating Iran’s ability and willingness to reach a so-called ‘deal’ in the very short-term. Iran may re-open the Straits in due course (chiming with our base line scenario) but any peace deal may be far off, if at all; after all Iran and the U.S have been at loggerhead of nearly 50 years!

March retail sales with a 1.7% rise, 1.9% ex autos are stronger than expected. Most of the rise is on the surging price of gasoline, though sales ex auto and gasoline with a 0.6% increase are on the firm side of expectations, with February revised up to 0.6% from 0.4% and January to 0.4% from 0.2%. Tax cuts passed in 2025 have lifted tax refunds in early 2026 and are in part offsetting the rise in gasoline prices.

Revisions overall were less strong than for ex auto and gasoline sales, with February revised up only marginally to a 0.7% rise from 0.6% and January now unchanged rather than declining by 0.1%.

Anticipated gains have broken above 98.50 to reach 98.74, where unwinding overbought intraday studies are prompting short-term reactions. Daily stochastics continue to rise and the daily Tension Indicator has turned positive, highlighting room for continuation towards resistance at congestion around 99.00 and the 99.18 high of 8 April. However, negative weekly charts should limit any immediate tests of this range in renewed selling interest/consolidation. Meanwhile, a close back below 98.50 would turn sentiment neutral and prompt fresh consolidation above congestion support at 98.00.

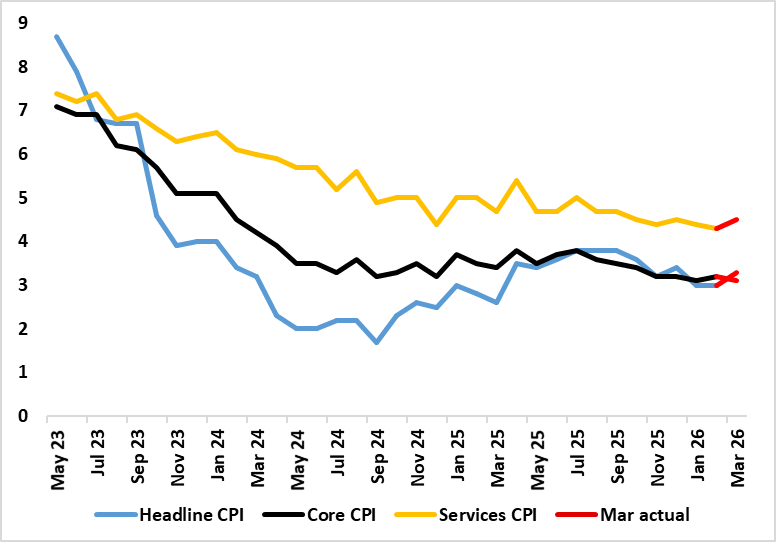

Figure: Headline Stable But Core Higher

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a four-year low (Figure) to .5% on the back if what may have been early Easter induced airfare rises, but the core still edged down a notch due to lower non-energy good inflation (Figure). The markedly and relatively greater surge in diesel relative to unleaded fuel warrants a hardly surprising upgrade to the price outlook for the rest of the year. On the basis of our baseline 4-8 week war thinking, we see the headline CPI falling back for in April before moving back higher in May in Q4 but then dropping back to end the year to 2027 at just over 2.5% but with the 2027 picture little changed, not least as tightening financial condition bite and soft wage pressures persist.

Figure: Labor Market Loosening Taking Toll on Wages

There are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down over 0.5 ppt in y/y terms. Admittedly, headlines may be formed around a surprise fall in the jobless rate to 4.9% but this is in no way any sign of fresh tightening the labor market. Instead, it reflects a rise in in inactivity, possibly reflecting dashed hopes of finding a job, especially among students. This is not surprising given the further fall in vacancies. Indeed, the ratio of vacancies to unemployed – perhaps a better guide of labor market tightness than the jobless rate as it reflects both the supply and demand for labor continues to trend lower (Figure). As a result, it does seem as if this is at least partly behind the further fall in wage pressures. Indeed, private sector regular earnings are now running at below 3%, the lowest since pandemic related pressures softened them in mid-2020.