This week's five highlights

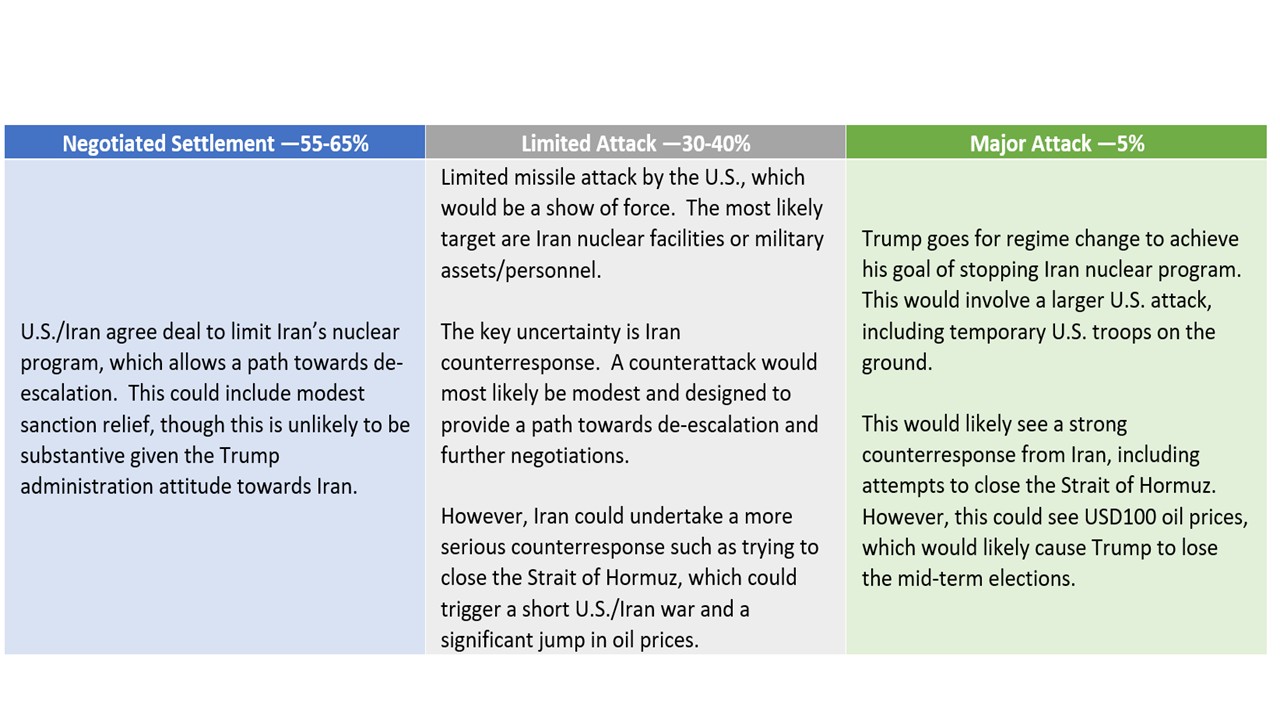

U.S. and Iran

"New" Tariffs From Trump

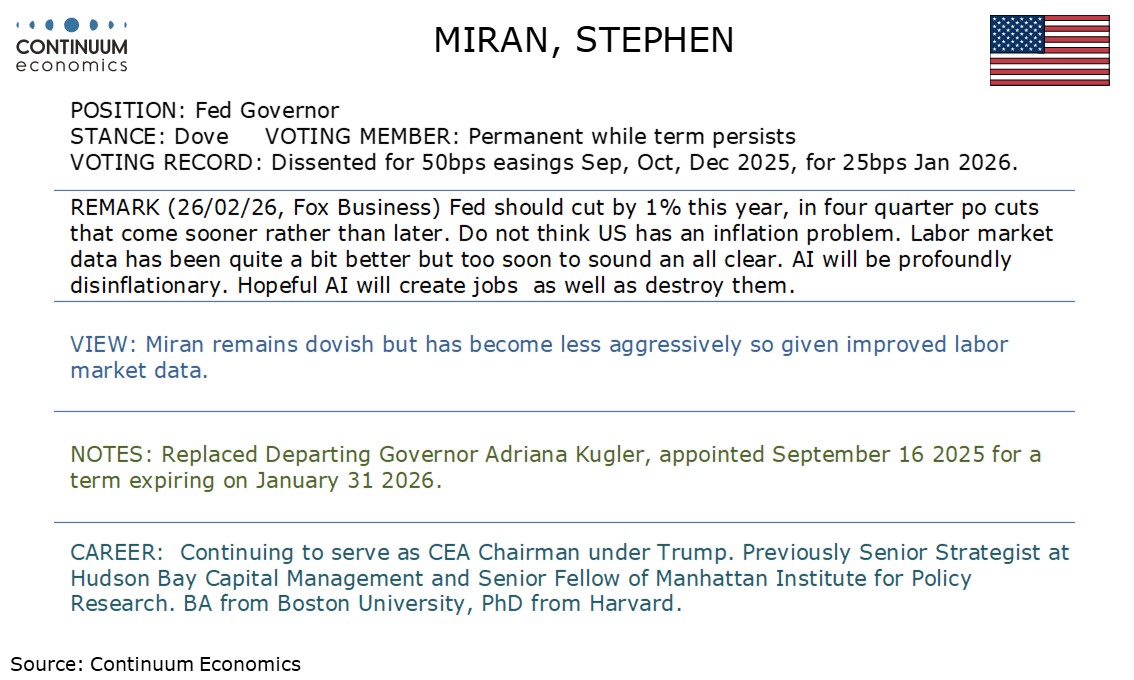

This Week's Fed Speakers

Tokyo CPI Dips Further Below 2%

Canada Q4 GDP a modest correction

Iran authorities appear reluctant to meet the Trump administration’s demand to stop nuclear fuel production for potential weapons. This increases the odds of a limited attack by the U.S. on Iran to 30-40% (Figure), which could occur as soon as this weekend. The most likely Iran counterattack would once again be designed to allow a path towards de-escalation and then better negotiations. However, modest odds exist of Iran trying to close the Strait of Hormuz, which could spike oil prices up to USD100.

The U.S. armada off Iran is designed as a show of force, but Iran has not caved in during the negotiations. Iran authorities appear reluctant to meet the Trump administration’s demand to stop nuclear fuel production for potential weapons. This increases the odds of a limited attack by the U.S. on Iran to 30-40% (Figure 1), which could occur as soon as this weekend. Negotiators are trying to get the two sides to agree on a face saving compromise that Iran could still undertake nuclear research for medical purposes, but it is unclear whether a breakthrough will occur. (Note: Regional actors, including Turkiye and Qatar, remain concerned by the escalating tensions and continue to advocate for a formal negotiation process). The other restraining factor on Trump is that an attack could cause a jump in oil prices, which causes U.S. voter backlash given that cost of living is the number one concern before the November mid-term elections.

Figure: Cumulative Tariff Revenue (USD Blns)

The 6-3 vote by the Supreme court and full ruling against reciprocal tariffs means that the Trump administration will likely resort to other tariffs for negotiating leverage. However, the Trump administration will also pressure to codify existing trade framework deals that have been concluded with most major trading partners excluding China. The ruling could also weaken Trump’s USMCA renegotiations.

Politically this is a big disappointment for the Trump administration and Trump has already voiced his outrage. The Trump playbook will follow through with threats of replacement tariffs; anger and also distraction (e.g. dialing up Iran and/or Cuba tensions). Additionally, it appears that the prospect of a tariff refund could have to be shelved and Congress is unlikely to be in a mood to undertake new tax cuts without rebuilt tariff revenue given the fiscal situation.

The headline Tokyo CPI for February stays low at 1.6%. Ex fresh food is also below target range at 1.8% while ex fresh food and energy arrived at 2.5%. While it eases the pressure for the BoJ to hike immediately, it is worth noting a big part of moderation comes from base effect and latest round of energy stimulus.

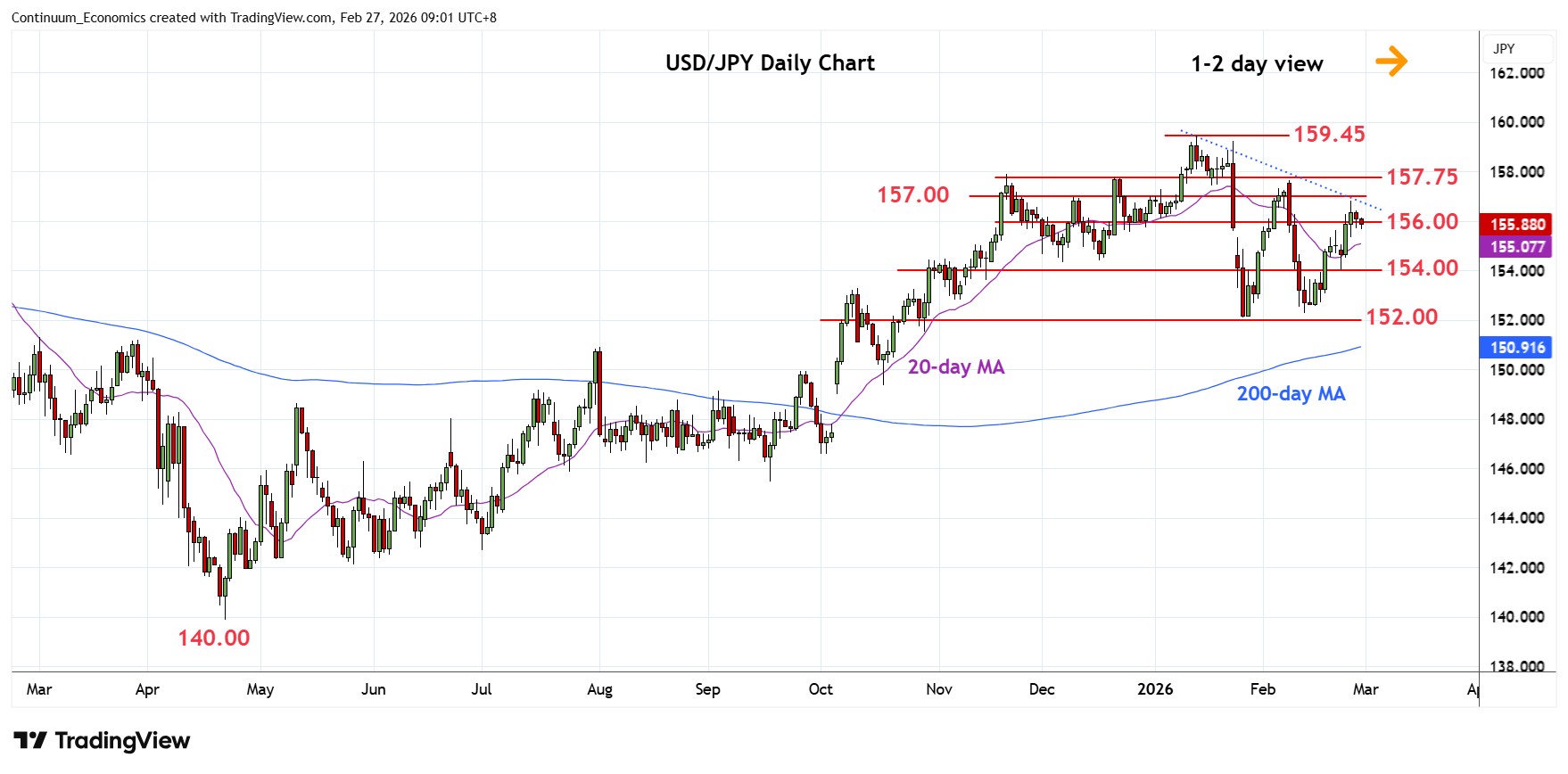

On the chart, the pair settled back to consolidate at the 156.00 level as gains met with selling pressure beneath the 157.00 resistance. Intraday and daily studies are unwinding overbought readings and suggest scope for pullback to retrace recent strong gains from the 152.27, 12 February low. Meanwhile, support remain at the 155.00 congestion and where break will fade the upside pressure and open up room for retest of the 154.00 level. Below this will return focus to the downside for retest of the 152.27 low then the 152.10, January current year low.