This week's five highlights

April FOMC Minutes Hawkish concerns appear broadly felt

Cautious DXY trade

ECB Not the Only Game in Town

UK CPI Falls Broadly

UK Core Wage Pressures hit New Cycle -Low

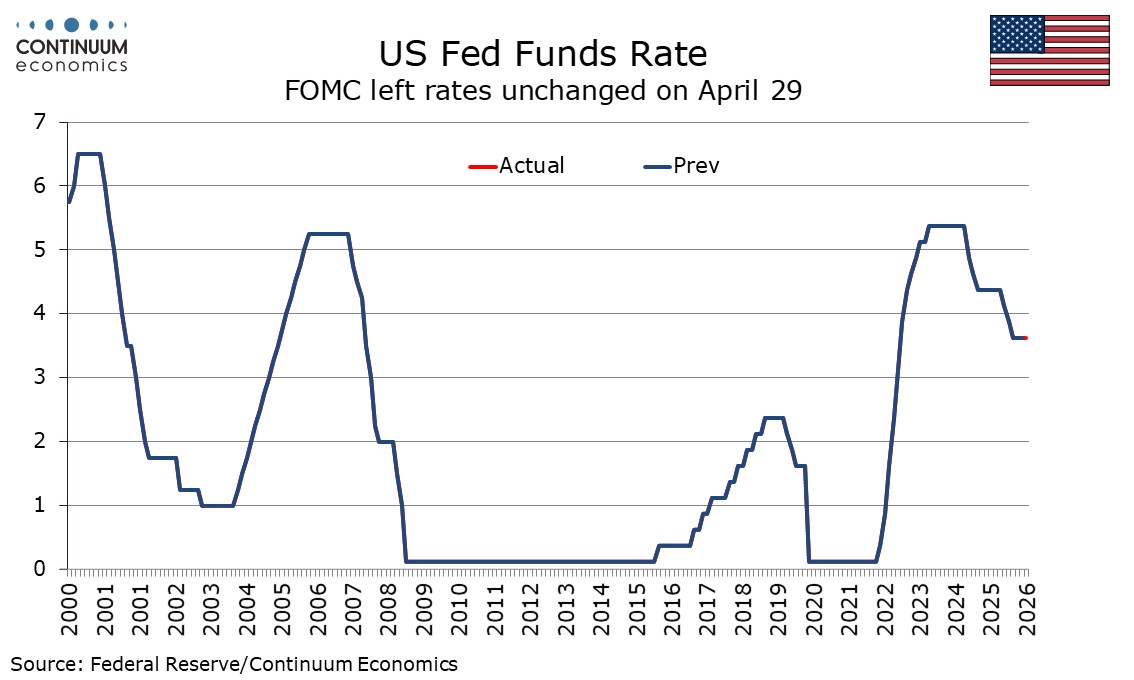

FOMC minutes from April 29 show a hawkish leaning, confirming market perceptions that there was more interest in removing an easing bias from the language than revealed by the three hawkish dissents at the meeting. Should inflation remain persistent, tightening could come onto the agenda, though should the Middle East situation get resolved, talk could still move back towards easing.

Almost all participants supported maintaining the Fed Funds target at 3.5-3.75%, and the one dovish dissenter, Stephen Miran, no longer sits on the FOMC. Several participants highlighted easing would likely be appropriate once there are clear indications that disinflation is firmly back on track or if solid signs emerge of greater weakness in the labor market. Neither of those conditions look likely to be met in the near term, though several looked to a scenario where rate cuts would be warranted later in the year if the Middle East conflict was resolved soon. Soon on April 29 may mean very soon today.

On the chart, prices extend consolidation following the test of congestion support at 99.00. Both daily and weekly readings are improving, suggesting room for further gains. A close above resistance at 99.50 will open up congestion around 100.00, where already overbought daily stochastics could prompt fresh consolidation. Meanwhile, support remains at congestion around 99.00. A test beneath here, if seen, should give way to consolidation above further congestion around 98.50.

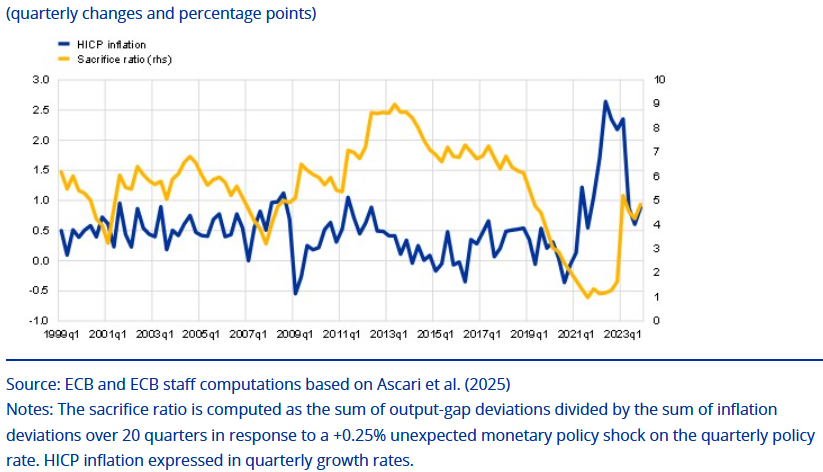

Figure : HICP inflation and Sacrifice Ratio Over Time

The ECB blog basically asserts that monetary policy in the EZ was particularly effective during the 2022-23 tightening episode. It asserts that it achieved rapid disinflation with limited output cost which reflected a stronger transmission to inflation relative to past monetary policy interventions, a more decisive monetary policy response to supply-driven shocks, and the continued anchoring of inflation expectations. We think this is almost arrogant in suggesting that a) the ECB rate hikes were the only factor involved and b) that the analysis does not comment on the extent to which the Council was culpable in allowing inflation to rise in the manner that then precipitated the conventional tightening cycle.

In terms of assessing how limited were the output costs, we would suggest that GDP may be far from the best measure. GDP growth in the year and two years after the first hike were buoyed by very strong government consumption and a marked fall in imports. As Figure 2 shows, while GDP overall was hit minimally in both the first and then eight quarters after the initial hike, domestic demand ex government fared far worse, this surely as, if not far more, important in shaping domestic price pressures.

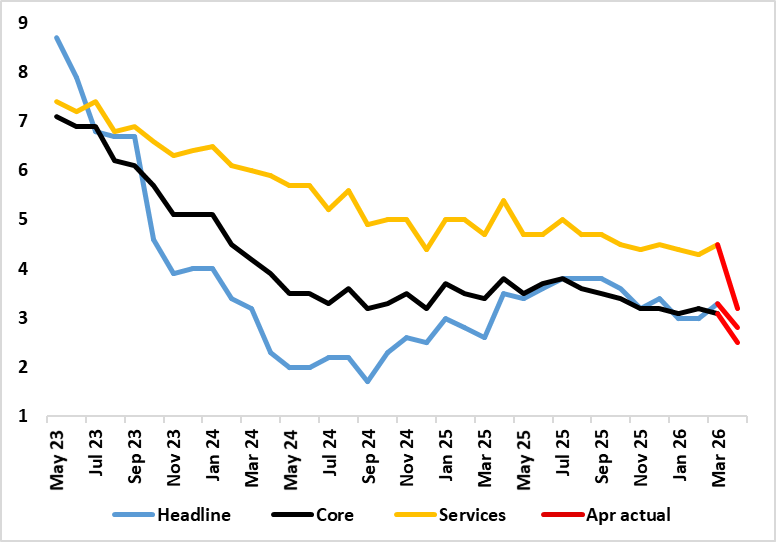

Figure: Headline And Core Much Softer – For Now?

It is noteworthy that without the rise in fuel prices in the last few months, headline UK inflation would actually be just over 2.1%, ie in line with most projections, (inc the BoE) ahead of the breakout of the Middle East conflict. Even so, a current reality of a headline at 2.8% is below BoE thinking and surely reduces the chance of near-term MPC hikes, not least given the lack of second-round effects. As for the policy outlook, the IMF now says in its Concluding Statement of its latest insight into the UK (out this week), monetary policy should remain restrictive to ensure that higher energy prices do not spill over to core inflation and wage growth. It says that the rise in energy prices will lift headline inflation this year while also weighing on output, complicating policy calibration. Staff assesses that holding the policy rate unchanged for the remainder of the year would maintain a sufficiently restrictive monetary stance to limit second-round effects and keep long-term inflation expectations anchored. However, given exceptional uncertainty, the BoE should retain the flexibility to adjust the monetary stance in either direction (ie hikes or cuts), but be prepared to respond forcefully if second-round effects prove stronger than anticipated.

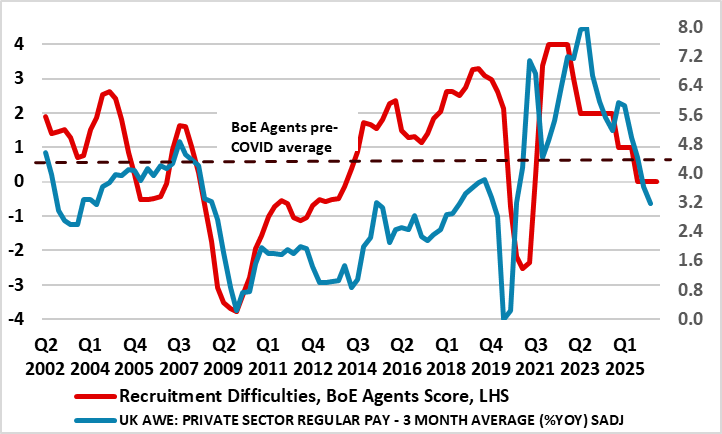

Figure: Labor Market Loosening Taking Toll on Wages

This private and regular measure of earnings is the barometer the BoE use to gauge wage pressures and is now running at a pace (ie about 3% y/y) consistent with the 2% CPI target, this on the assumption of productivity growth of around 1%. Admittedly, the data now reflect post-Iran War dynamics and may not affect what will be divided BoE thinking given the distortions still involved in the numbers. But what is key is that private sector earnings are growing well below the 7%-plus pace seen before the Ukraine War started four years ago. In fact, in terms of short-term dynamics, private sector regular earnings have growth a meagre 0.6% (ann rate) in the last three months.

Regardless, the latest official labor market data (still bereft with reliability questions) are showing more comprehensive signs that the labor market is loosening with activity rates rising further and back to almost pre-pandemic levels. Partly as a result, the jobless rate has risen afresh to 5.0% and, in tandem with what are still weak(er) vacancies, is very much showing that the ratio of the two has hit new highs, also consistent with a looser labor market. This helps explain the clear(er) signs of softer wage pressures with the growth rate of private sector regular pay down to the lowest since end-2021.