Financial Markets/Policymakers and the Strait of Hormuz Question

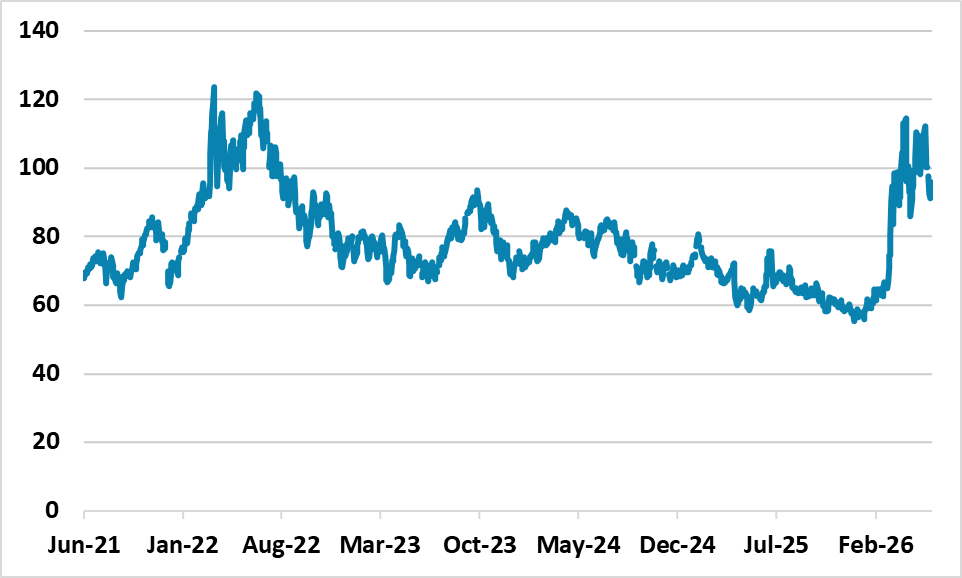

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD10 off oil prices but still leaving them at USD85 for WTO by end 2026. If this is not delivered by late summer/early autumn then oil prices could spike to USD120-150 by upset financial markets.

Oil prices have been elevated but controlled since the end of Iran/U.S. hostilities, but the oil market remains watchful of stockpile rundowns.

Figure 1: WTI Oil Prices (USD)

Source: FRED

Financial markets remain divergent, with equities focused on the AI and wider corporate earnings story (with intermittent profit-taking), but bond markets apprehensive of 2nd round effects from existing energy prices and the risk of DM rate hikes. Financial markets relative calm reflects central bank communications that they do not need to overreact to higher energy prices. Of the major DM central banks, the ECB will kick off with a widely expected 25bps hike (here). However, the forward guidance will likely be that this could be followed by a further hike, but that the situation differs from 2022 when domestic demand was more buoyant/labor market tighter. The BOE, on June 18, will likely still signal risks of higher policy rates, but not guaranteed for July. The BOJ hike will be normalisation on June 16, but the BOJ is unlikely to accelerate the pace of normalisation. The Fed is expected to remain on hold, but the key will be the communication, with some Fed officials likely to highlight the risk of hikes but new Fed chair Warsh likely to maintain the status quo. A hawkish hold could spook the U.S. Treasury market.

The other reason that financial markets are relatively well controlled is that oil prices have not spiked, despite the 3 months plus Strait of Hormuz closure estimated to have cut 10-12mln barrels per day (pipeline diversion has reduced the usual flows). The oil market guidance is that China has cut approximately 5mln barrels per day of demand, which when combined with strategic and commercial stockpile reduction elsewhere has stopped oil prices spiking. However, oil experts worry that the quick stockpile rundown could slow by mid-summer and cause an imbalance between demand and supply that requires further demand destruction i.e., USD120-150 oil prices.

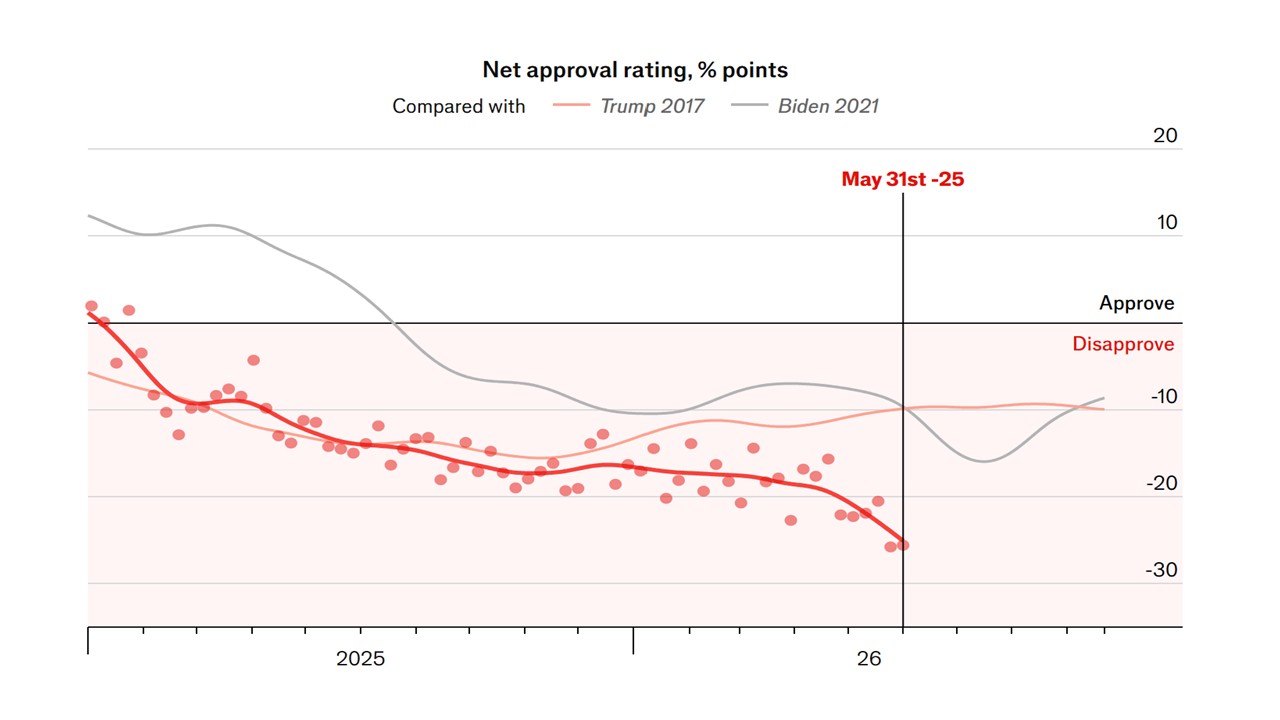

An Iran/U.S. agreement to reopen the Strait of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD10 off oil prices but still leaving them at USD85 for WTO by end 2026. Despite the June 10 U.S. attack and Iran counterattacks, Iran economic interest is to agree an interim deal with the U.S. including the Strait of Hormuz. The ongoing lack of exports due to the U.S. blockade, plus the risk that stopping well production could cause long-term difficulties, are key drivers to reach a deal. The Trump administration are keen to get a reopening that reduces oil prices and help Trump (Figure 2) and the Republican popularity before the November mid-terms. Even so, we previously estimated a 30% risk that distrust could stop a deal. Next week we will reassess the Strait of Hormuz scenarios, but our baseline is a Strait of Hormuz agreement in June or July. The unease calm will continue in financial markets.

Figure 2: Trump’s Approval Rating (%)

Source: The Economist