ECB Preview (Jun 11): Words Not Deeds the Focus

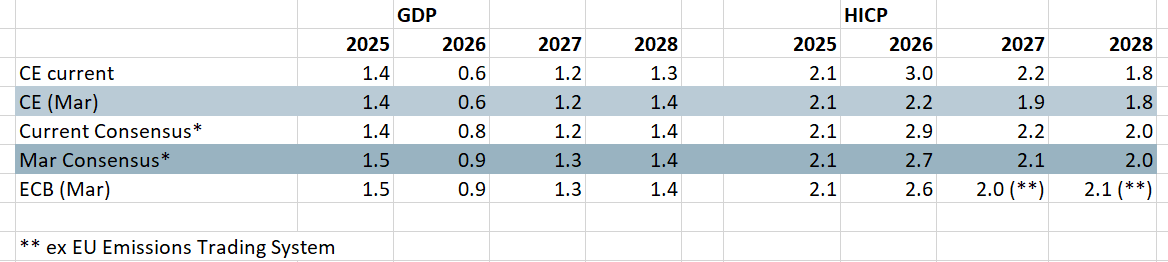

Aware of repeating ourselves (again), it is the case that the next ECB Council meeting will be more important for what is said than what is done. In fact, a 25 bp official rate hike is virtually nailed on irrespective of how events in the Middle East may fare in coming days. But the ECB comments and updates projections will give clear signs as to how fast and further, the Council consider policy rates may have to rise. We think that the looming 25 bp hike is more than enough and that this misplaced move will be more than reversed into 2027 (ie thinking largely siding with the OECD). But the projections are likely to show HICP inflation back in line with target through 2028, this though largely validating the market view of up to three 25 bp hikes that the outlook will be based on. But the projections will also show an even weaker GDP picture, albeit probably still above our below consensus outlook, with the ECB understating the combination of tight(er) financial conditions, banking sector reservations and ill sentiment that should combine to pull HICP inflation back to, if not below, 2% by mid-2027 and thus create both rationale and room for fresh policy easing.

Figure 1: Economic Outlook From Various Perspectives

Source: CE, ECB, Consensus Economics

We still think the ECB is and will remain too pessimistic about inflation and too optimistic about growth. Some energy perspective may be helpful here, not least as the large share of electricity generated from renewables and nuclear provides a buffer for the consumer. Unlike the energy shock of four years ago, there has been relatively little upward pressure on LNG prices, meaning less chance of a repeat of the 30% surge in gas/electricity bills that occurred in the six months after the invasion of the Ukraine. In addition, especially given the marked fall back in diesel prices of late, liquid fuel rises in the HICP may actually start to fall from this month on. Indeed, in stark contrast to the energy price backdrop into the last (April 29-30) Council meeting, oil prices are currently some 20% down while gas prices are line with the 2026 assumption made in March. Of course, this is not the whole story, not least given the Middle East’s conflict impact on fertilizers and supply chains – the latter a clear upside price risk. And these have shown up in business surveys where costs have risen sharply, but nowhere near as much as seen in 2022 and may even have started to reverse, begging the question as to whether Say’s Law (supply creates its own demand) works in reverse.

Indeed, and arguing against any clear wage spiral emergence, an ever-wider array of survey data suggest also that job losses are also starting to become worryingly widespread as business confidence spirals down. Notably, the service sector is being hit especially hard by the cost surges created by the war. Moreover, what is even more notable is that supply shortages not only pose upside risks to prices but can and seem to be constraining real activity already growth already and probably more so in the coming months. With this in mind, how the ECB revises it real economy outlook this month will be as important as how inflation is altered, the former very much helping determine both the size and persistence of any price shock – one that does seem to be increasingly supply related. But these factors explain our below-consensus GDP outlook, one that is very much with downside risks that reflect obvious adverse global factors and real income damage from higher fuel prices, but also ECB policy.

Indeed, ECB policy is biting adversely, either directly or indirectly) through three channels. Firstly, financial conditions have tightened even further, underscoring that the discount rate was and is a poor guide to the policy stance. Secondly, the ECB is still drawing down its balance sheet with excess liquidity (at EUR 2.4 trillion) having halved from its peal and set to fall toward EUR 1.5 trillion by end-2027. Since the ECB’s bond portfolios very well might continue to shrink even then, the idea is that regular liquidity operations would become more used by banks to offset that effect. Then, at some point, the ECB would introduce structural liquidity operations.

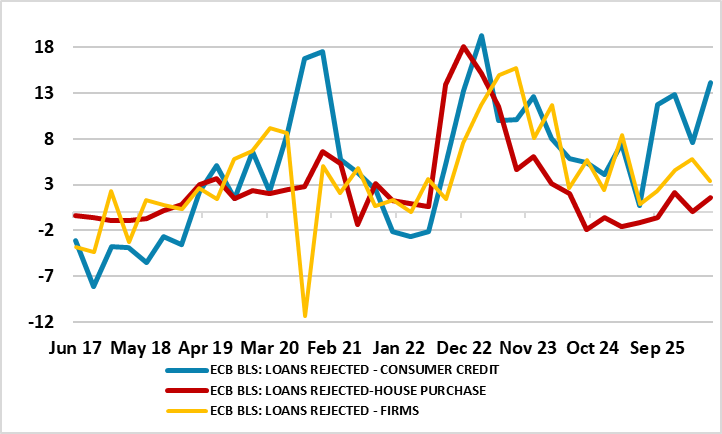

Figure 2: Loan Rejection Rates Rising and Above Long-Term Averages?

Source: ECB, % balance

Thirdly, as lending surveys have reputedly shown, banks are not just more reluctant to lend but are actually rejecting an increasing amount of possible loans, especially those that have less collateral attached (Figure 2).

However, it is the case that the ECB is still reverberating from the 2022 energy shock and criticism it faced of hiking both too late and too slowly. If so, the ECB is getting confused. What is notable is that this energy shock and the ECB’s positioning is very much different to that of 2022, occurring at a point when the EZ economy is operating with a margin of spare capacity as opposed to one reviving from a pandemic induced demand shock. This is accepted clearly by the ECB!

And this assumes that changes in policy rates have been fully passed on by banks to borrowers, something that does not seem to have been the case during the most recent easing cycle. Indeed, while the ECB discount rate (now down to 2%) is some 2 ppt below the peak last seen in mid-2024, the effective cost of borrowing for firms has fallen by only 1.5 ppt while that for household by a puny 40 bp! All which to us suggest that the ECB is about to embark on the kind of policy mistake it presided over in 2008 and 2011. It may be the case that the ECB is once bitten, twice shy but will be thrice wrong!