This week's five highlights

Straits of Hormuz Scenarios

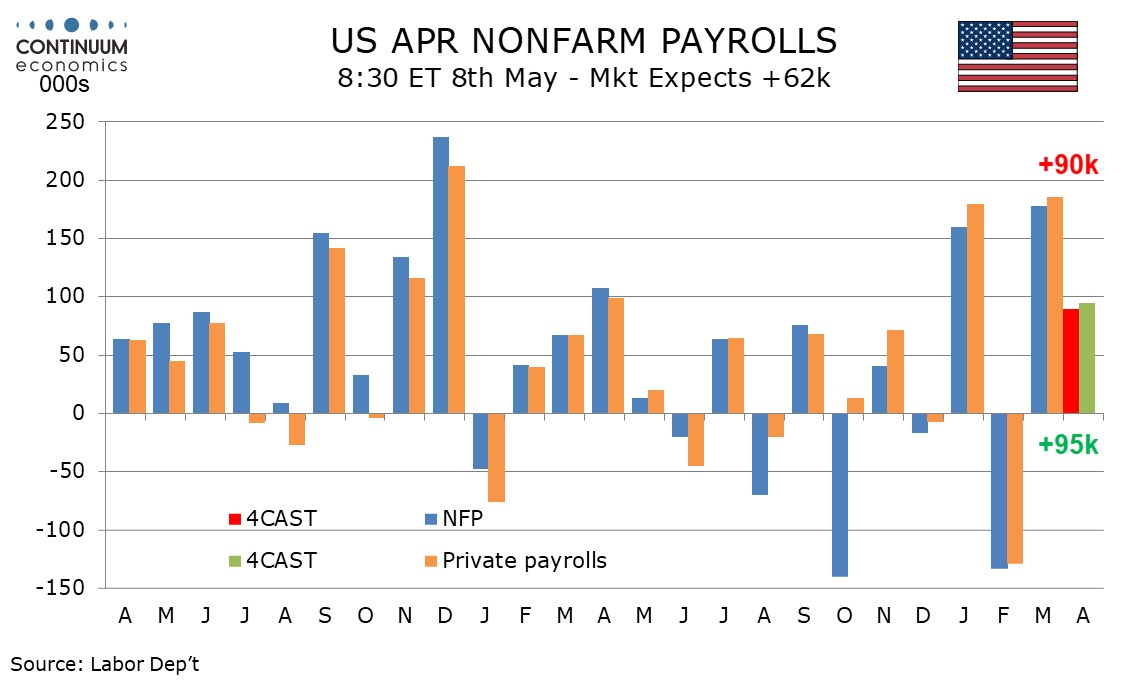

U.S. April Non-Farm Payrolls Not as strong as March

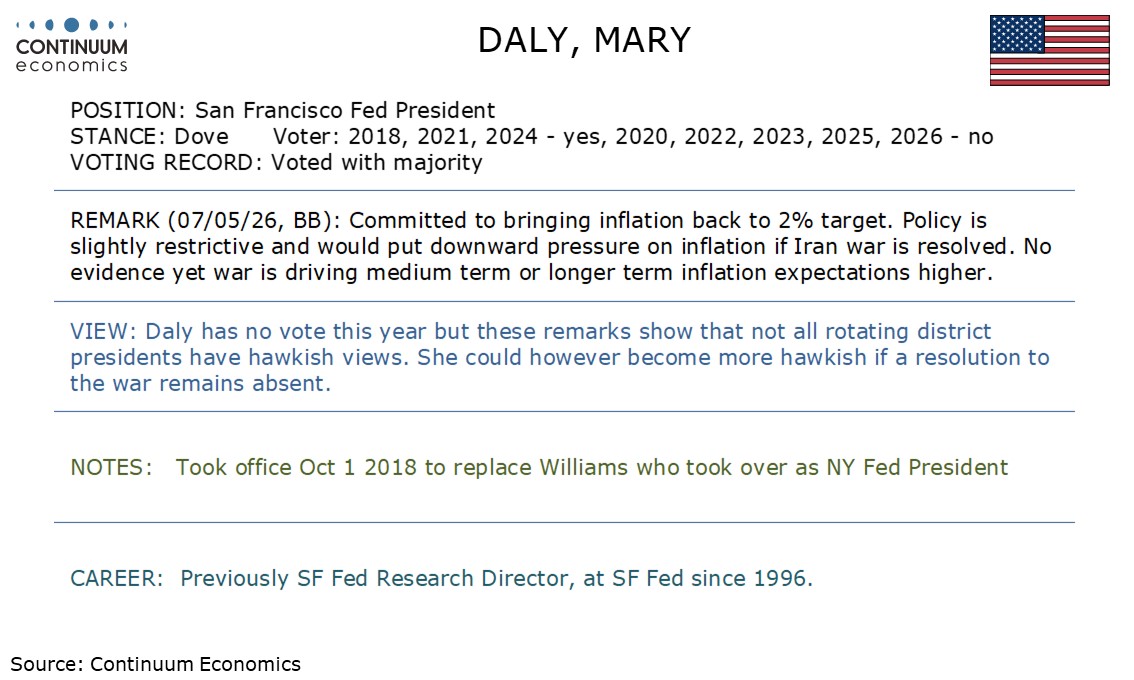

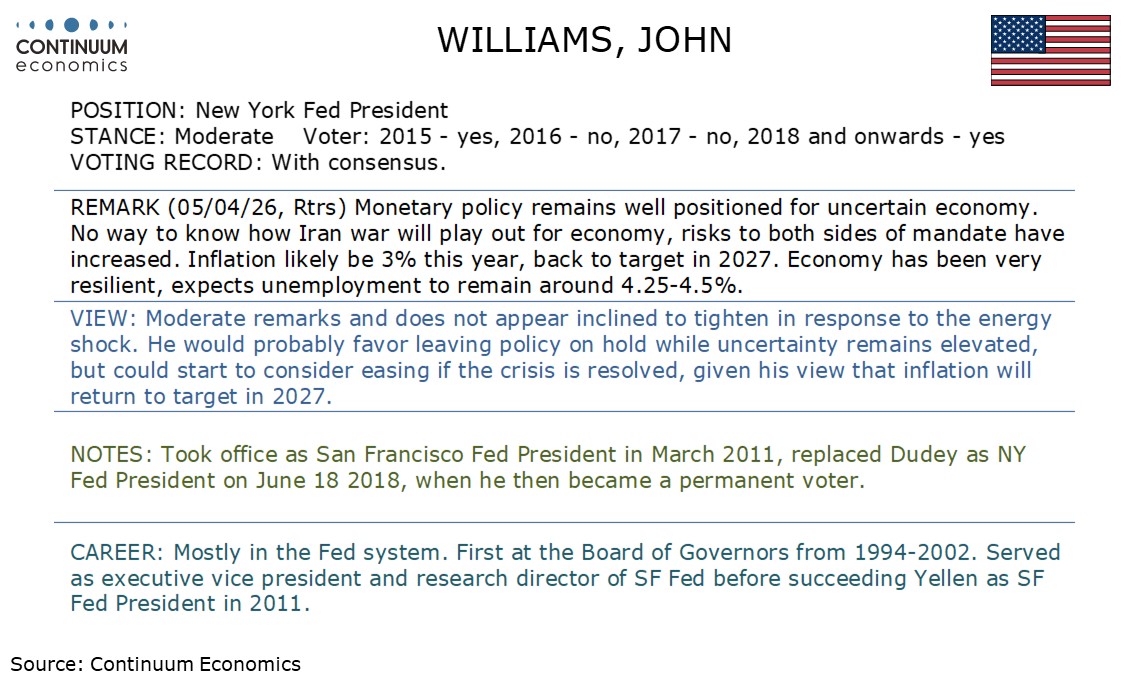

This Week's Fed Speakers

RBA's Last Hike for Now

Fresh Tightening Bias for Sweden Riksbank

Figure: WTI Oil prices

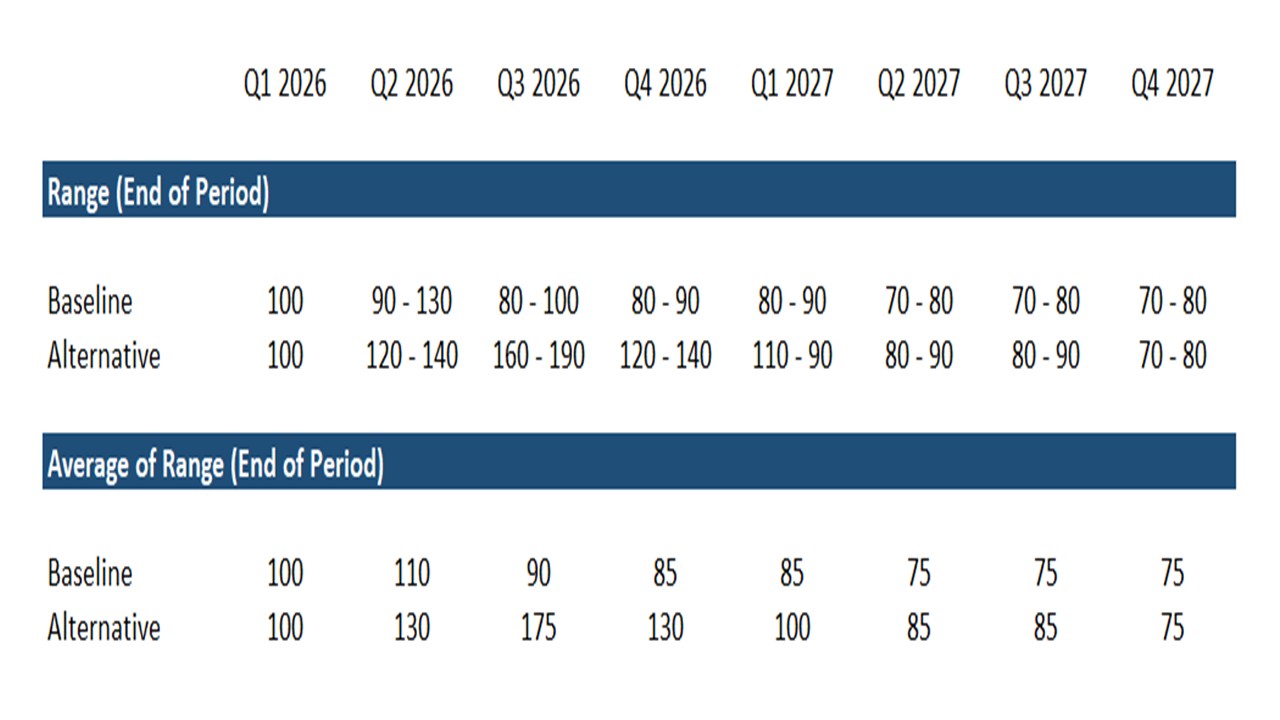

Our new baseline (70% probability) is for the Straits of Hormuz to start to partially reopen by June/July based on a framework deal between Iran and the U.S. This means more elevated oil prices in Q2, but then a gradual reduction in WTI to USD85 end-2026 and USD75 end 2027. The alternative scenario (30%) is that negotiations fail to produce a deal to reopen the Straits of Hormuz and we assume the Straits remains effectively closed until end September. This leads to a super spike to USD160-190, as oil has to price for demand destruction.

The U.S. and Iran are reluctant to restart the war, with President Trump’s threats having been followed by a ceasefire and Iran wishing to negotiate to avoid major infrastructure damages. Still, the ceasefire is fragile, and negotiations have not progressed on a number of occasions. We highlight two main scenarios re the Straits of Hormuz, which are shaped by the objectives of both sides.

We expect April’s non-farm payroll to rise by 90k overall and by 95k in the private sector, less strong than in March but implying some improvement in trend. We expect unemployment to slip to 4.2% from 4.3% and an in line with trend 0.3% increase in average hourly earnings.

March’s 178k increase in non-farm payrolls was flattered by 32k returning strikers, who exaggerated a 133k decline in February. February’s weakness was also in part due to bad weather. March bounces in weather-sensitive sectors such as construction and leisure/hospitality will be difficult to match in April. However our forecast is significantly higher than the average of February’s and March’s payrolls, and also a 4-month average of 47k (57.5k for private payrolls) which includes a strong January and a weak December too.

The RBA underwent a decisive shift in the first half of 2026 as they raised the official cash rate three times, bringing it to 4.35%. While the hawkish pivot origin from strong domestic demand, external energy shock from the Middle East has exacerbated their stance. Headline Q1 CPI shoot past 4% y/y with latest monthly CPI surged to 4.6%. The strong inflationary pressure from both the geopolitical shock and domestic demand seems to have driven the RBA to hike the third time his year.

Such is nothing new as market participants are well aware of the geopolitical risk and RBA's forecast of bring rates to around 4.35% in 2026. The forward guidance "Having raised the cash rate three times, monetary policy is well placed to respond to developments" seems to be providing new clues and suggest the RBA is done for now. They will definitely have their eyes on the inflation picture. Yet, if there is no more hawkish surprise, they are likely indicating three consecutive hike should be enough to curb inflation without severely affecting economic growth.

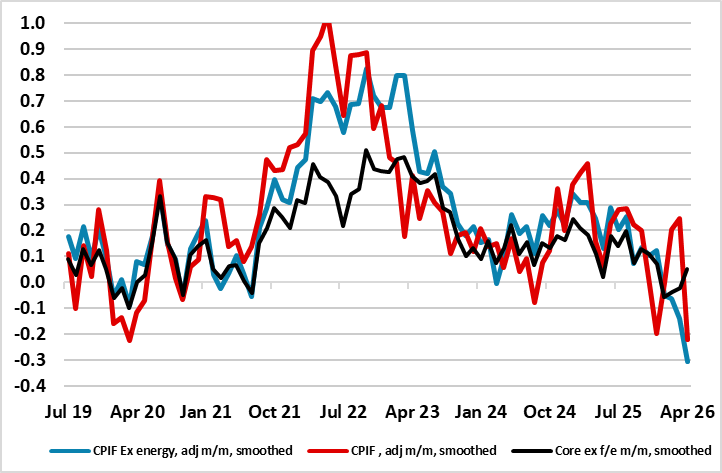

Figure: Core CPI Inflation Again Surprising to the Downside

It is always notable how quickly things can change, especially when it is external events that precipitate a shift in the backdrop and outlook. Notably, with inflation (Figure) and real economy numbers having undershot both the Norges Bank and consensus expectations, the Riksbank might have been contemplating a fresh easing at this juncture if not for events in Middle East. But stable policy seems to be the accepted alternative in current circumstances and this was again the the verdict this month. However, there was a shift in the policy bias, as the Board did not repeat its assertion made in March of no change for some time to come. Instead, it noted that even amid Middle East conflict making the outlook very uncertain, it was in a good initial position to adjust monetary policy if required to safeguard the inflation target. However, we still see stable policy though to end-2027 and will look to minutes of the meeting (May 13) to see the extent to which fresh Board divisions may have (re)surfaced.