This week's five highlights

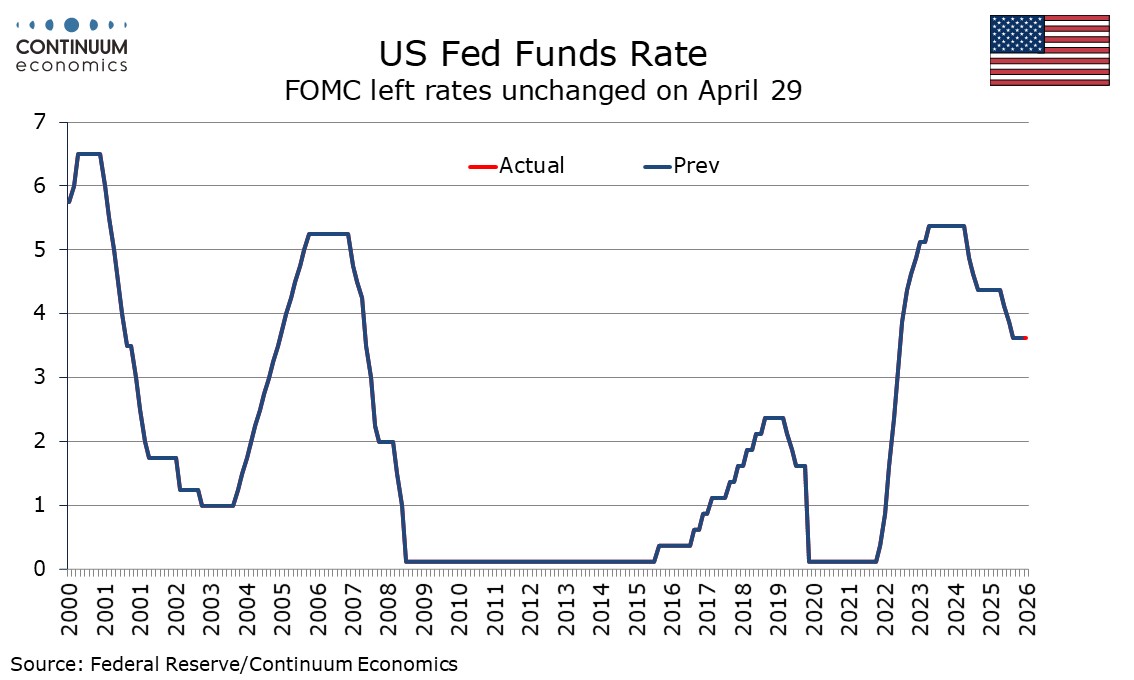

FOMC keeps rates on hold but three of four dissents are hawkish

BoE MPC Playing Its Cards Safe

ECB Mixed Communications

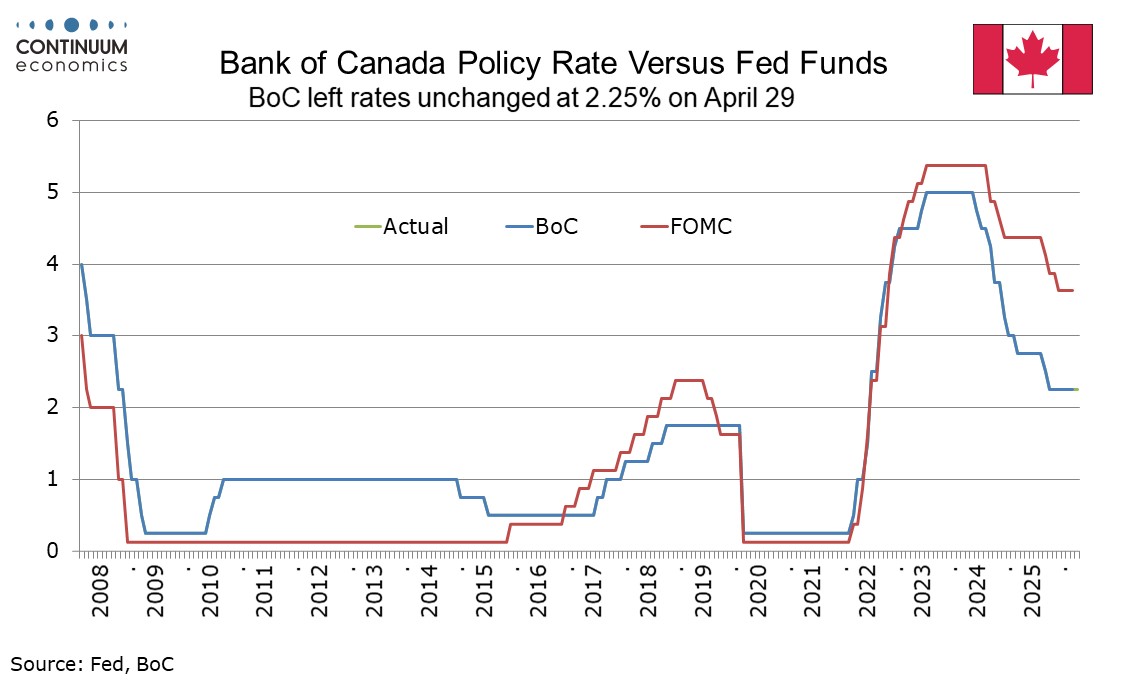

Bank of Canada Policy seen appropriate under baseline assumption

BoJ Slightly Hawkish Hold

The main surprise in the FOMC statement was the number of dissents, one dovish, Miran continuing to call for a 25bps easing, and three hawkish, with Hammack, Kashkari and Logan in agreement with the decision to leave rates unchanged but objecting to the inclusion of an easing bias. This means three of the four rotating regional voters made hawkish dissents, the exception being Philly Fed’s Paulson, and it is likely some of the non-voting regional presidents hold similar views. That none of the permanent voters dissented is however significant, suggesting Warsh, who is likely to Chair the next meeting, may be able to count on a majority of votes, though once Warsh enters Miran will exit.

The easing bias is not strongly explicit, the statement repeating a reference to the extent and timing of additional adjustments, but the three hawkish dissenters appear to want it made clear that adjustments could go in either direction, something that recent minutes have suggested was advocated by some. In the assessment of the economy the statement is a little more hawkish, the qualifier on average added to the view that job gains remain low, and inflation now described as elevated rather than somewhat elevated, with energy prices now noted explicitly as a factor. The statement is also more explicit about the role developments in the Middle East are playing in contributing to high uncertainty.

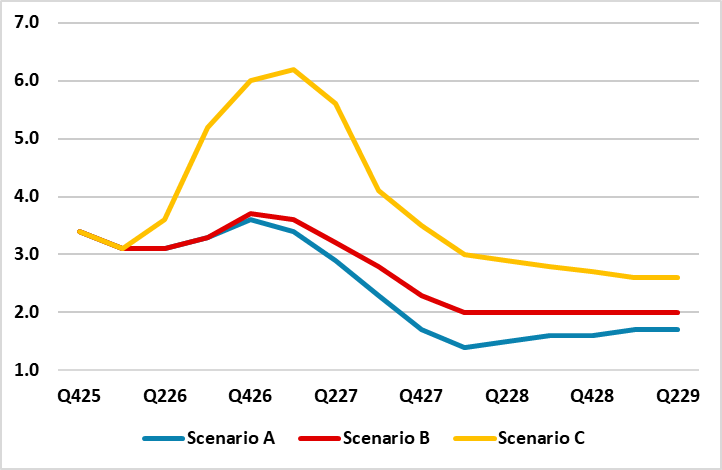

Figure: The BoE’s Three Scenarios

Very clearly, the BoE kept rates on hold with the MPC last month and the same decision was both expected and delivered this time around but with only token fresh dissent, with Chief Economist Pill wanting an immediate hike from the current 3.75%. But splits were more evident in the individual MPC member statements (as expected) where more diverging views in an around the three scenarios that the BoE is now projections all based on modest hiking of around 50 bp over the coming year. We still think that the BoE is offering too much information in these individual views and as a result is confusing markets just as it did in March. But among the key and relatively common themes is that financial conditions have tightened even without actual hikes and that the labor market is loosening. And it this tightening that pulls policy severely back towards conditions when Bank Rate peaked that makes up see a much softer real economy outlook than the strangely similar GDP outlooks in all of the BoE scenarios.

What is notable and as the updated projections do show, is that this energy shock is justifiably viewed by the BoE as being different to that of 2022, occurring at a point when the economy is operating with a margin of spare capacity and where policy is already restrictive. We think this very much reduces the chances of second round effects as does the already loosening labor market where earrings growth have slowed to a rate consistent with the 2% inflation target.

Figure: EZ HICP Including Projections From March Forecasts (%)

Overall, the June and July meetings have live risks that the ECB could undertake a modest 25bps hike. If a partial reopening of the Straits of Hormuz occurs then the ECB will likely keep hawkish, but not actually hike. We feel that the ECB is overestimating natural gas prices, while financial conditions and the economy argue for caution against hiking. Lagarde did note in the Q/A that financial conditions tightening is evident. The odds would then be that the ECB does not hike in 2026. Alternatively, if the Straits of Hormuz is still closed by the June 11 meeting, then the hawks could be able to push a 25bps hike through at the June meeting or commit to a move in July. The doves would counter that 2nd round wage effects are absent meaning a hike would not be guaranteed.

The Bank of Canada left rates unchanged at 2.25% as expected and Governor Macklem sees policy as appropriate under a BoC baseline that assumes oil prices evolves according to market expectations and US tariff rates remaining unchanged. This supports our view for steady BoC policy through 2026, though Macklem added that policy may need to be nimble given unusually elevated uncertainty. The BoC is prepared to move in either direction, but tightening later in the year is probably a greater risk than easing.

Oil prices are assumed to decline to around $75 per barrel by the middle of next year and if that happens CPI, which increased to 2.4% in March from, 1.8% in February, is seen peaking at around 3% in April and easing back to the 2% target by early next year. Independent of the oil shock, CPI is due for an acceleration in April due to the April 2025 abolition of the carbon tax lifting the base.

The BoJ has kept rates unchanged at 0.75% in the April meeting with three votes dissent that is looking for another 25bps hike. There hasn't been any changes to BoJ's stance of more hike but the geopolitical tension in Middle East may have a temporary negative effect on wage growth in Q2. It led the BoJ to revise their economic forecast for 2026 lower before rebounding in 2027. Inflation forecast is revised higher to 2.5-3% in 2026 before rotating lower in 2027 and reaching target at 2028.

The geopolitical disruption is unlikely to derail BoJ's plan to further tighten as the business wage/price setting momentum has gained traction. Their major concern lies on short term wage growth slowdown on lower business margin. Their 2026 GDP forecast is halved from January forecast of 1%. Core CPI0.9% higher while core-core CPI 0.4% higher than earlier expectation.

We suspect Ueda will sound more hawkish than usual in his press conference with no change in forward guidance. They are assessing the situation in Middle East and should hike as early as in the June meeting if energy disruption is eased.