FX Daily Strategy: N America, October 22nd

Carry trading continues in quiet markets…

…but JPY weakness unlikely to persist without further yield spread moves

CHF looks vulnerable if risk positive tone persists

USD continues to benefit from rising expectation of Trump victory

GBP may still have potential for gains on UK budget

Carry trading continues in quiet markets…

…but JPY weakness unlikely to persist without further yield spread moves

CHF looks vulnerable if risk positive tone persists

USD continues to benefit from rising expectation of Trump victory

GBP may still have potential for gains on UK budget

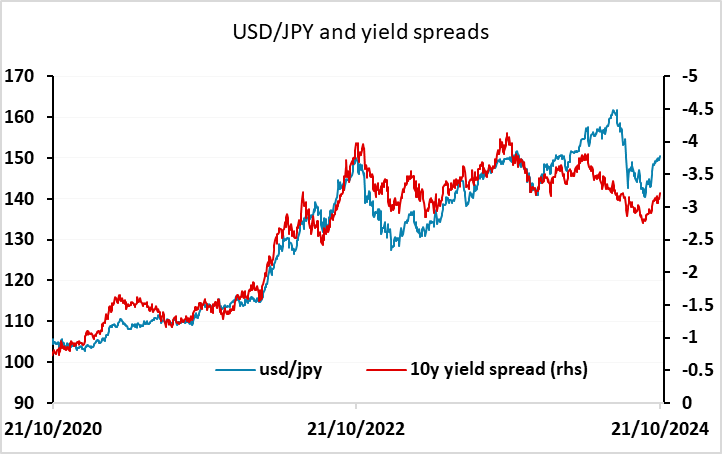

Tuesday is another light data day, with nothing of any real consequence, and this will tend to feed the carry trade. The JPY was the weakest currency through Monday, falling back across the board, with very little other movement of consequence. Some of this relates to the modest move higher in US and European yields, some of it looks like a consequence of the low news and low volatility conditions that tend to favour the higher yielders. However, such gains are typically not sustained. The correlations of levels of currencies with levels of yield spreads are consistent, and if there was a consistent impact from carry trading, there would be a relationship between changes in currencies and yield spreads, which there isn’t on anything other than a very short term basis. This is a long-winded way of saying that carry trades that aren’t based on moves in yield spreads may benefit (minutely) from the carry advantage, but don’t lead to any sustained move in spot. That being the case, USD/JPY can be expected to move back towards the levels suggested by yield spreads over the longer run, and this still suggests a level closer to 140 than 150 even based on current nominal spreads.

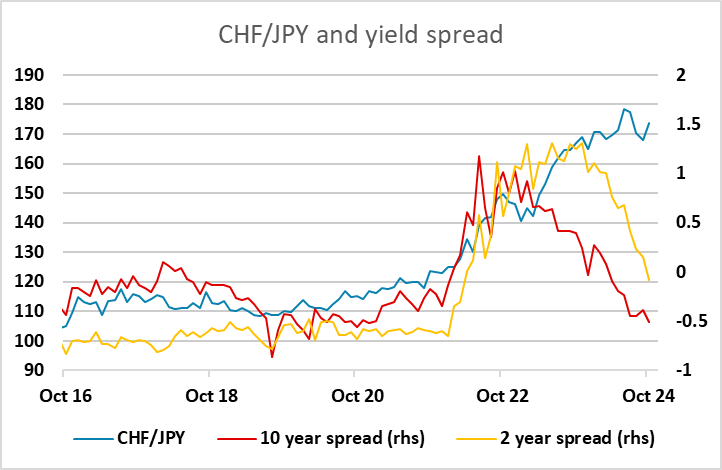

As usual, we would emphasise that the JPY is likely to gain more than this in the longer run because the relatively low Japanese inflation rate has meant that JPY has seen a big real as well as a big nominal depreciation in the last few years. The only currency against which this isn’t the case in the CHF, as Swiss inflation has been similar to inflation in Japan. The comparison of nominal yield spreads and the nominal currency is therefore more valid in CHF/JPY, and continues to suggest substantial JPY gains are overdue. The CHF actually gains slightly against the EUR on Monday in spite of the weakness of the JPY, but looks ripe for some weakness against the higher yielders if the risk positive conditions are sustained.

Some of the JPY weakness was due to higher yields in Europe and the US, which in turn looks to be largely due to rising expectations of a Trump victory in the US presidential election. Trump’s policy of extending tax cuts are likely to lead to less dovish Fed policy, while the imposition of tariffs is expected to benefit the USD against the currencies that are more dependent on world trade. In practice, we would expect these effects to be quite minor, but as long as the market believes in them, the USD can be expected to benefit from rising expectations of a Trump victory. While the polls remain very close, the betting markets have moved significantly in Trump’s favour in the last couple of weeks, and he is now priced as having a better than 60% chance of victory.

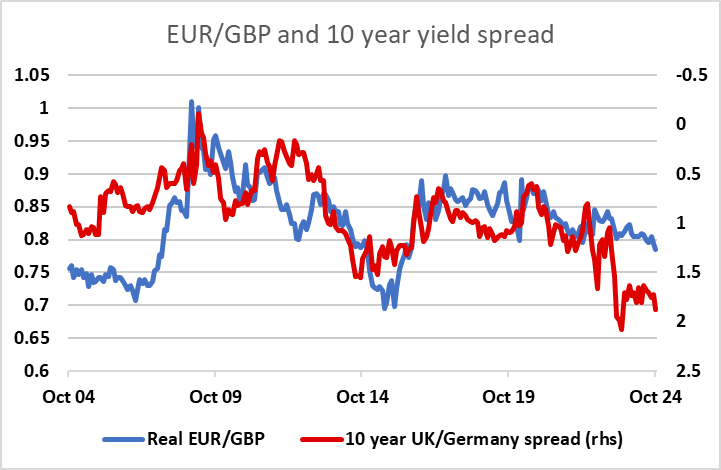

GBP has also generally been a strong performer both this year and in the last few weeks. Much of this relates to the relatively high level of UK yields. Even allowing for the relatively high rate of UK inflation which has meant that GBP has appreciated even more in real terms than in nominal terms in recent years, the pound continues to look relatively cheap given current yields, as the risk premium in UK yields that emerged during the short-lived Truss administration in 2022 has never quite left the market. It may be that the Bank of England eases more than currently priced in, but longer term yields may depend more on the shape of the October 30 budget. There has been much speculation about the detail of this, and there is a memory of the Truss budget leading to both higher UK yields and a lower pound, but a positive reception to this budget could see the reverse, with the pound benefiting even as longer term yields decline.