FX Weekly Strategy: October 21st-25th

Fairly quiet week suggests relatively steady FX markets

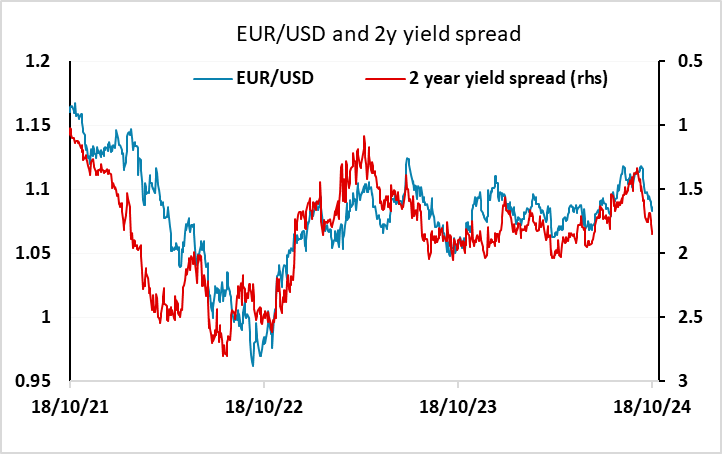

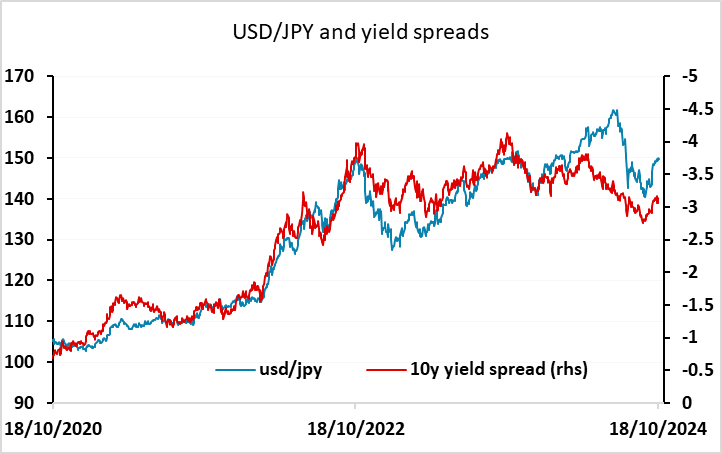

EUR/USD still biased lower and USD/JPY still stretched…

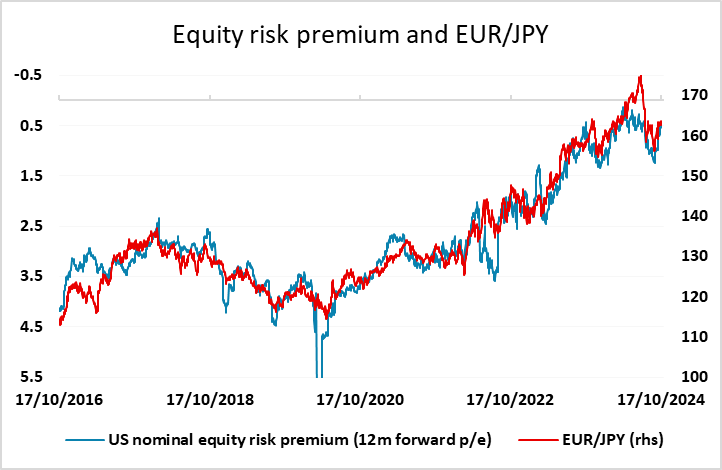

…but a turn lower in EUR/JPY may require weaker equity sentiment

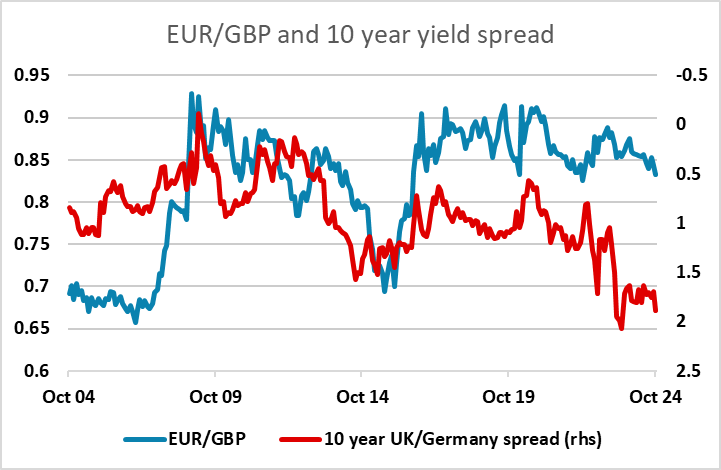

GBP strength likely to be sustained unless PMIs surprise

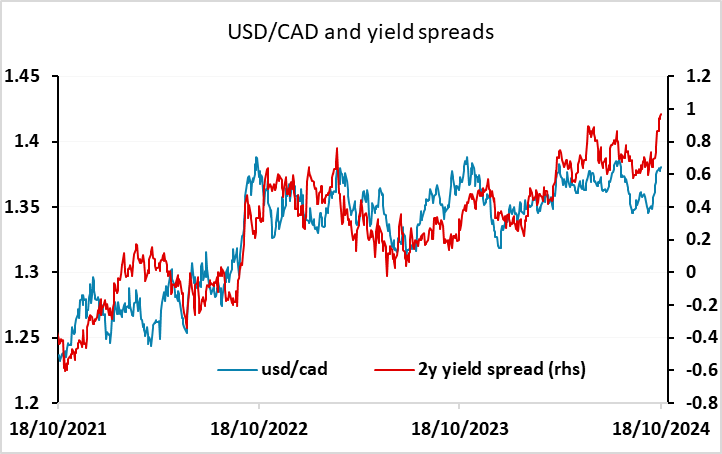

CAD risks on the upside on BoC

Strategy for the week ahead

Fairly quiet week suggests relatively steady FX markets

EUR/USD still biased lower and USD/JPY still stretched…

…but a turn lower in EUR/JPY may require weaker equity sentiment

GBP strength likely to be sustained unless PMIs surprise

CAD risks on the upside on BoC

It looks like a relatively quiet week this week without major data and with the market looking towards the US election and the Fed and BoE central bank meetings in early November. For the moment, the USD remains well bid, with the latest US data on the firm side and the recent comments from Fed officials somewhat less dovish. The market is now no longer pricing the November and December Fed meetings as completely certain to produce rate cuts, with 43bps of easing priced in by year end. This still implies high probabilities of 25bp rate cuts at both meetings, but it wasn’t so long ago that the market was looking at the possibility of 50bp cuts. The rise in front end US yields that has resulted from this, combined with somewhat softer yields in the Eurozone as the ECB has turned more dovish in response to softer data, means that the correlation with yield spreads still points to some downside risks for EUR/USD.

However, 1.08 represents significant technical support, and having failed t break below this level after the ECB meeting, it may now require some further catalyst to produce a break. There is nothing obvious along these lines on this week’s calendar, so for now we may see EUR/USD stabilize in the 1.08-1.09 area.

There is less reason for USD gains against the JPY, with USD/JPY having already outpaced moves in 10 year yield spreads that have tended to drive the pair in recent years. There has also been some verbal intervention from Japan’s currency diplomat Mimura warning against speculative moves as USD/JPY tests 150. Actual intervention still seems unlikely just yet, but speculators are likely to be more wary at these levels. Even so, as was the case in the summer when USD/JPY fell sharply from above 160, we will likely need a turn lower in equity sentiment if USD/JPY is to resume its downtrend. EUR/JPY continues to move with equity risk premia, and currently looks fair based on that metric (although form a fundamental perspective it remains significantly overvalued). So while we would expect to see some substantial JPY gains emerge by year end, it isn’t clear that here is enough going on this week to trigger a significant move.

GBP was particularly strong last week, with EUR/GBP trading at its lowest level since April 2022 following stronger than expected UK retail sales data. We see these levels as overextended from a long term perspective, with the UK growth picture still uncertain and EUR/GBP in real terms at significantly overvalued levels. However, yield spreads levels remain very attractive by historic standards, with UK yields apparently still retaining some of the risk premium that was added under the Truss administration, even though the market has fewer fiscal concerns under the current UK government. If those concerns don’t return after the October 30 budget, GBP could manage further gains, and for now it is hard to see a rigger for the recent strength in GBP to reverse. The main risk this week looks to be the preliminary PMI data, although as we have noted before, these are not a reliable guide to the UK economic picture.

The BoC meeting is the main central bank focus this week, and the market is near enough fully pricing a 50 bp rate cut. Given that we still slightly favour a 25bp move, there is potential upside for the CAD, and even if there is a 50bp cut, the BoC statement may discourage the market from expecting the further cut in December that is more than fully priced in. Having said this, yield spreads have moved significantly in the USD's favour in recent weeks, so there is limited CAD upside scope even if the BoC turn out to be less dovish than expected.

Data and events for the week ahead

USA

It is a quiet week for US data, though there are plenty of Fed speakers. Monday sees September’s leading indicator while Fed’s Logan and Kashkari will speak. Tuesday sees Fed’s Harker. On Wednesday we expect September existing home sales to rise by 2.3% to 3.95m while Fed’s Bowman and Barkin will speak. The Fed’s Beige Book is also scheduled on Wednesday.

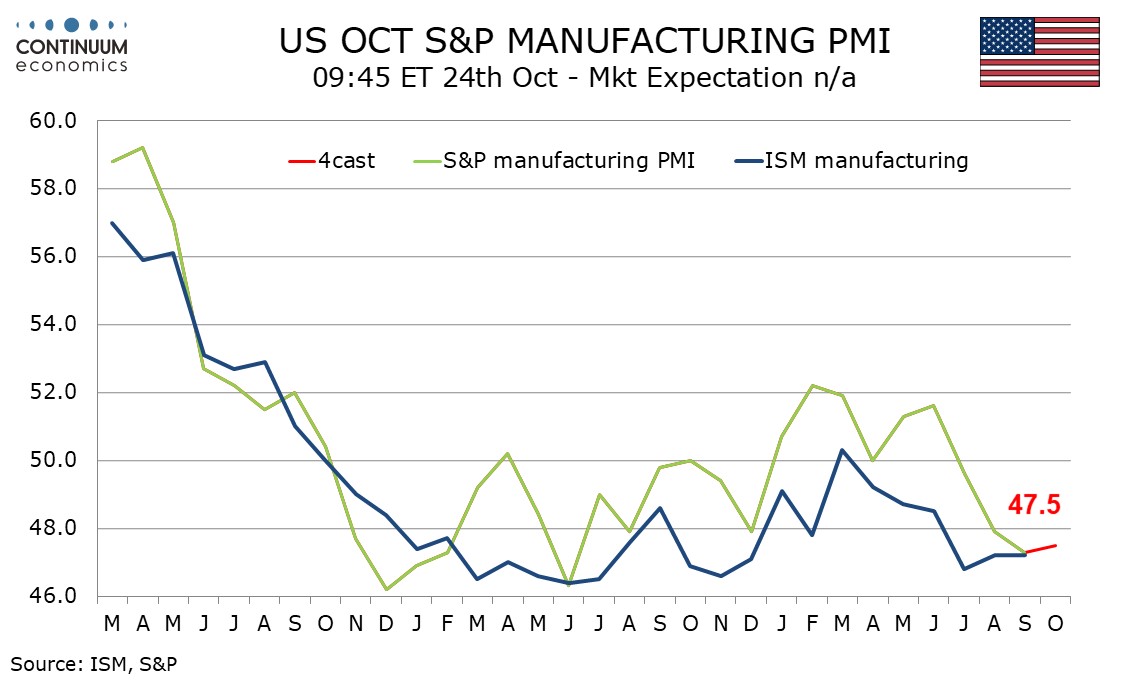

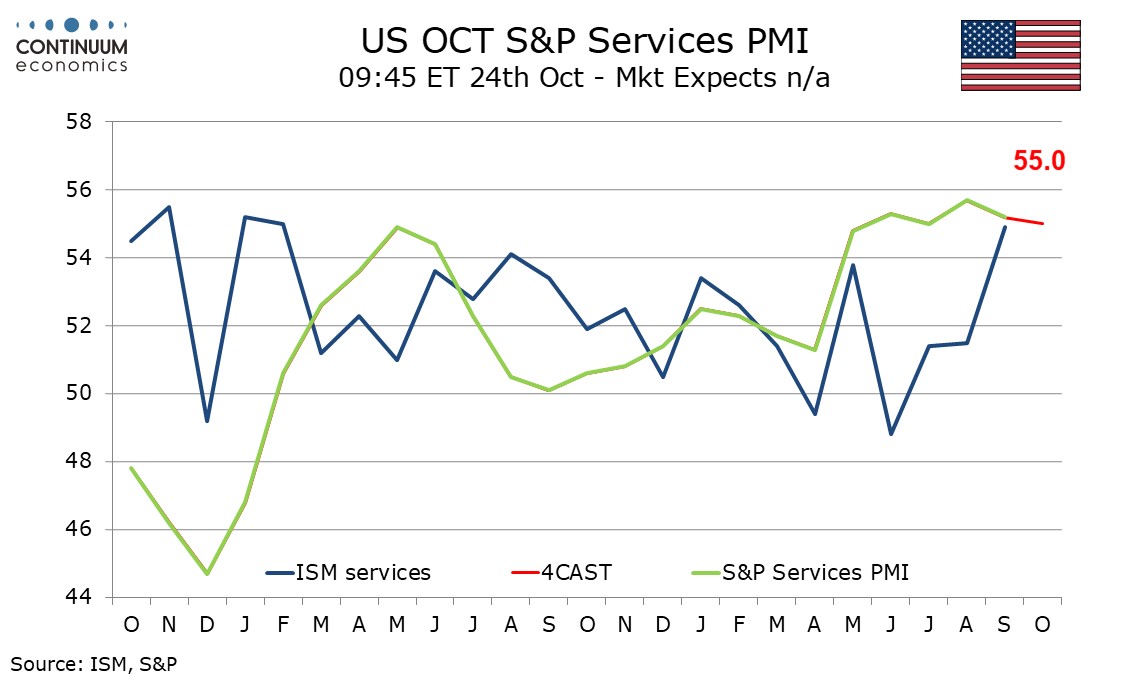

Thursday’s weekly initial claims data could get a boost from Hurricane Milton. October’s S and P PMIs follow, and we expect a marginal gain in manufacturing to 47.5 from 47.3 but a marginal dip in services to 55.0 from 55.2. We also expect September new home sales to slip to 705k from 716k, while Fed’s Hammack is due to speak. On Friday we expect September durable goods orders to rise by 0.6% but with a 0.2% fall ex transport. Final October Michigan CSI data is also due.

Canada

Canada’s key event is the Bank of Canada decision on Wednesday. With inflation having fallen closer to target but activity showing tentative signs of picking up it is a close call between a 25bps or a 50bps easing, though we lean towards a fourth straight 25bps move, to 4.0%. Data due are September’s IPPI and RMPI on Tuesday, and August retail sales on Friday, where the preliminary estimate was for a rise of 0.5%.

UK

After recent weak data, any insights from the BoE will be all the more interesting and in this regard Governor Bailey speaks three times this week at the IMF meeting (Tue, Wed & Sat) with other MPC members also offering their thoughts. Datawise, the main interest will be in the CBI Industry survey and PMI flashes (Thu). Last time around they pointed to much weak price and cost pressures and where we think a small further drop in the headline index is on the cards - at 52.6 in September, down from 53.8 in August, the PMI Composite Output Index pointed to the slowest rate of growth since June. Otherwise, public borrowing data (Tue) will take on more relevance ahead of the looming Budget.

Eurozone

ECB comments are also expected from Lagarde and Lane (Wed) along with many other Council members, most also from the IMF gathering. But survey data will be important too with the main interest in the PMI flashes (Thu). We see a stable reading but with more disinflationary signals. September survey data revealed another marked easing of cost pressures while the Composite PMI Output Index fell into contraction territory in September for the first time since February, dropping from August’s three-month high of 51.0 to 49.6. There are also key country survey data from the French INSEE numbers (Thu) and the German Ifo (Fri). Consumer surveys are also due both for the European Commission (Wed) and the ECB expectations numbers (Fri)

Rest of Western Europe

There are some events in Sweden, most notable being Riksbank Deputy Governor Jansson discuss monetary policy (Wed). In Norway the Norges Bank releases its latest survey of bank lending (Thu).

Japan

A rather clear calendar next week with Tokyo CPI on Thursday. National CPI this week has shown moderation but ex fresh food and energy rises. We expect the same to continue but the pace maybe slower.

Australia

Only PMI on Wednesday, unlikely to be market moving when they are preliminary.

NZ

Trade data will be released on Monday, RBNZ’s governor speech on Tuesday and Consumer confidence on Thursday. Governor’s speech may carry more weight as more upfront cut maybe signalled instead of steadily cutting.