FX Daily Strategy: APAC, October 18th

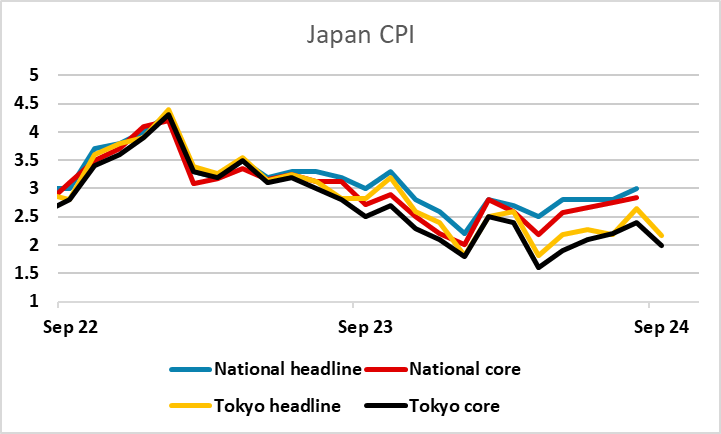

JPY still on the back foot – Japan CPI in focus

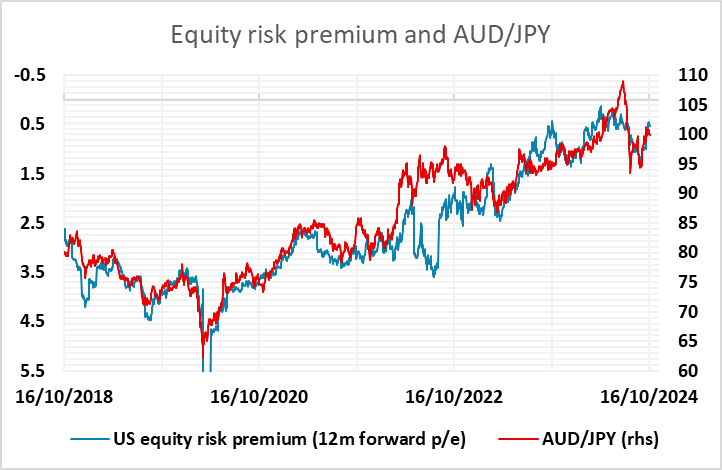

Risk sentiment remains positive after strong US data on Thursday

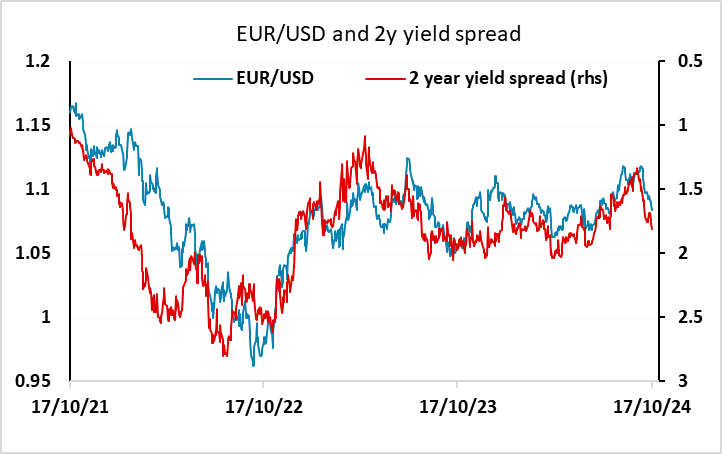

EUR/USD retains a downside bias

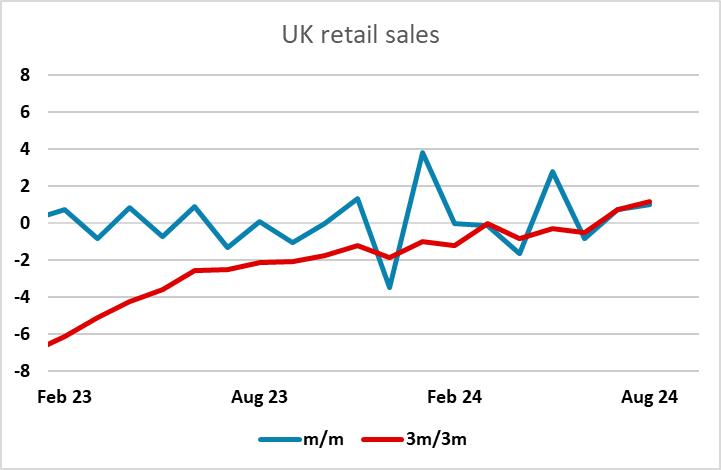

GBP risks on retail sales skewed to the upside

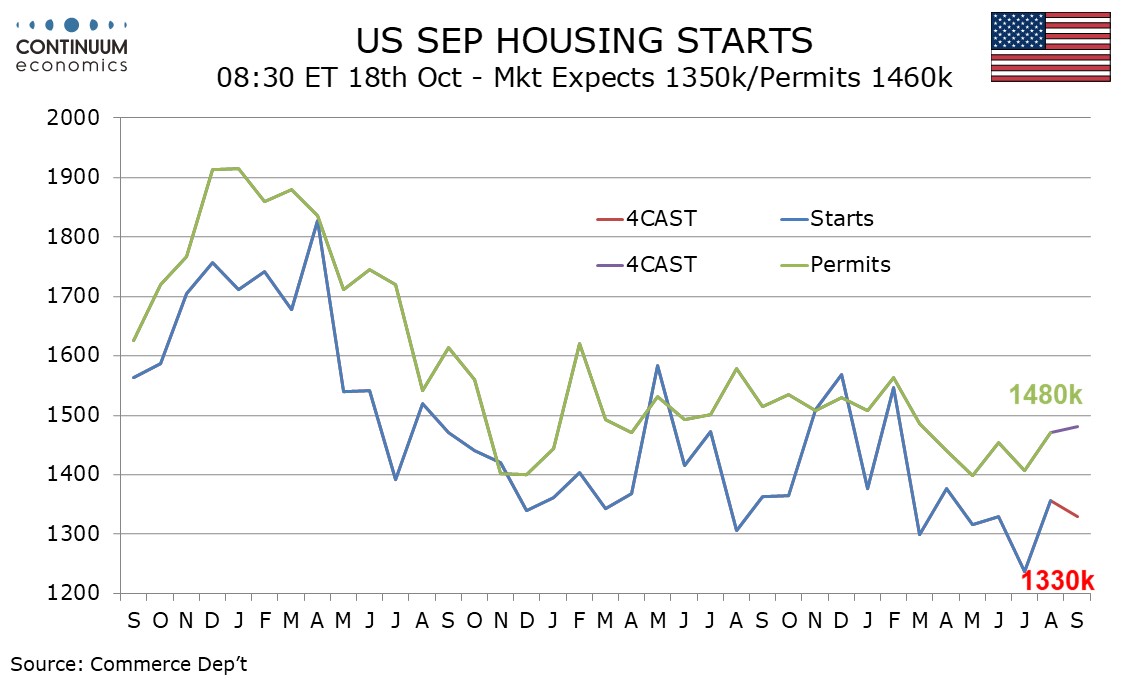

USD could benefit if housing starts robust despite hurricanes

JPY still on the back foot – Japan CPI in focus

Risk sentiment remains positive after strong US data on Thursday

EUR/USD retains a downside bias

GBP risks on retail sales skewed to the upside

USD could benefit if housing starts robust despite hurricanes

Friday kicks off with Japanese CPI data, but as usual the national CPI data is typically well predicted by the Tokyo data already released. Although the national numbers have been a little stronger than the Toky number sof late. Even so, there was a significant dip in the y/y inflation rate in the September Tokyo data, and the market s expecting a similar dip in the national CPI, with the core rate expected to fall to 2.3% from 2.8% in August. Given such a large fall in the y/y rate, it will be hard for the market to interpret the data as JPY positive unless there is a(very unlikely) big upside miss. So the USD/JPY break of 150 may extend to the upside unless we get some statements from Ueda or others suggesting tighter policy is still likely. We may see verbal intervention but this typically has very little impact.

There is also a bug set of Chinese data due, with the Q3 GDP data expected to show a 1% q/q rise, which would take the y/y rate down slightly to 4.6%. The market may be less sensitive to this than it has been due to the recent Chinese stimulus announcements which may prop growth up a little going forward. But we still don’t expect the new measures to do more than limit the weakness. Risk sentiment in general remains quite solid, helped by the strong US data on Thursday, and this also suggests some downside risk for the JPY, with the AUD likely to be among the most favoured after Thursday’s strong employment data, especially if the Chinese data comes in on the strong side.

EUR/USD fell back after the ECB meeting on Thursday, but the move was due more to the US data and general USD strength than any surprises from the ECB. There may still be some risk of a break below 1.08, but we are expecting EUR/USD to find some support near current levels, with spreads now unlikely to move significantly further in the USD’s favour.

The main European data of the day is UK September retail sales, and we may see some softness in the data, due in large part to weather effects. But after strong numbers in each of the last two months, the market should take a weaker number in its stride. There would be much more sensitivity to another strong number, which could be expected to trigger renewed GBP strength.

The main US data is hosuing starts. We expect September housing starts to see a 1.9% decline to 1330k after a 9.6% August increase though without Hurricane Helene a rise would probably have been seen. We expect permits to rise by 0.7% to 1480k, extending a 4.6% August increase. New home sales surprised on the upside in July and August and housing survey evidence for September is generally stronger with Fed easing starting. Construction details in September’s non-farm payroll, surveyed before Hurricane Helene, were also positive. So while weak data might be dismissed as hurricane affected, stronger data might suggest a housing market recovery due to the recent decline in US yields, which could be expected to provide further USD support.