FX Daily Strategy: Asia, October 16th

Geopolitics Keep Market on Edge,

UK CPI To be Below Target

and may drag Sterling below Support

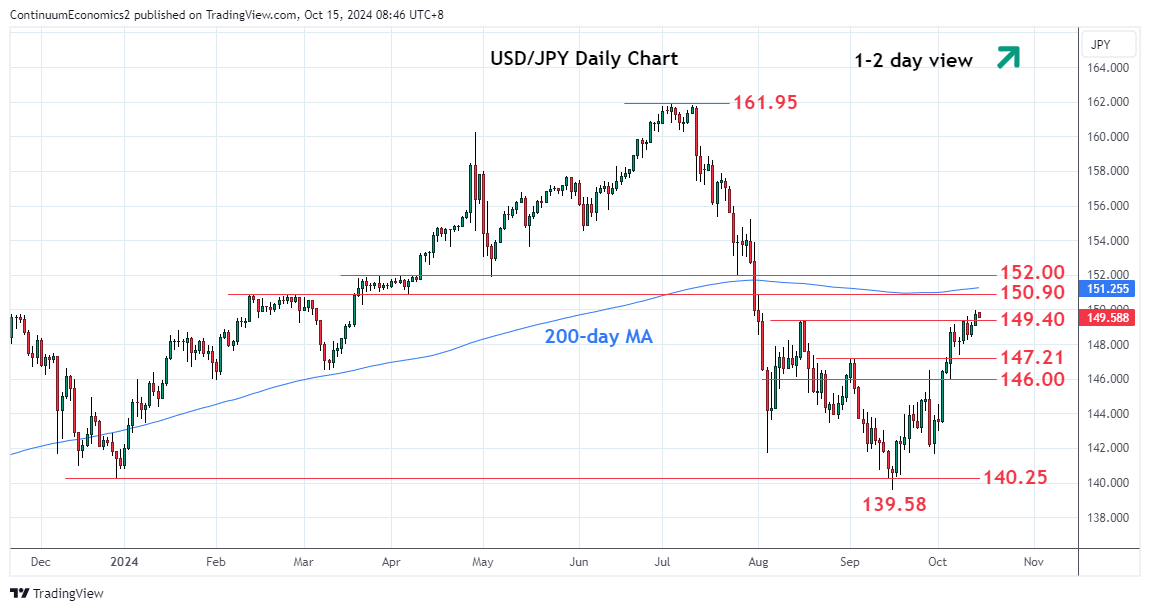

USD/JPY Retreats From 150

The geopolitics tension surrounding Israel continues and will keep market on edge despite PM Netanyahu said he will not strike Iran's oil and nuclear facility. However, this does not rule out a large scale retaliation from Israel as Netanyahu told the U.S. he will only hit military target. With Netanyahu announcing he will decide the form of response alongside Defense Secretary Gallant and Chief of staff Halevi earlier today, seems to suggest another round of operation is inevitable. The prolonged geopolitical tension will keep market participants on its toes despite the front running in oil price' decline.

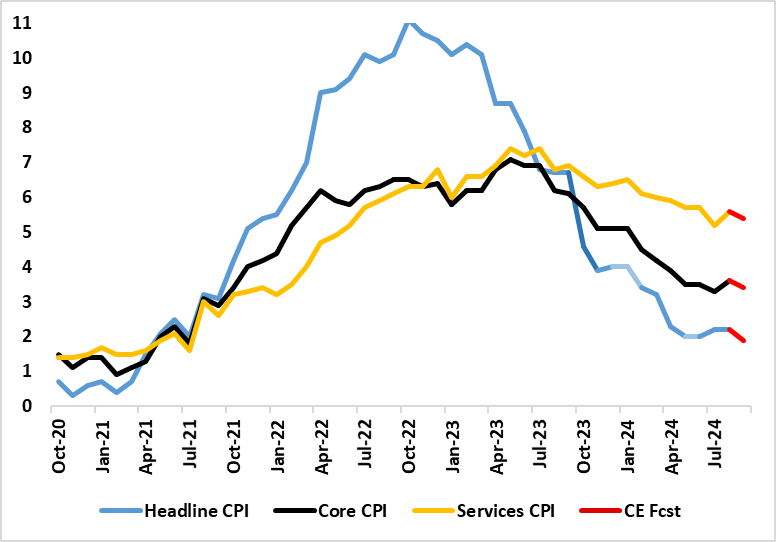

Figure: Broad Inflation Drop Ahead?

Helped by a fall in fuel prices, amplified by base effects, alongside some belated softening in services costs, UK inflation may drop to 1.9% in the September CPI (from 2.2%), thus falling below target since April 2021. Admittedly, the drop in services may be limited to a notch lower from September’s 5.6%, with the core falling similarly from 3.6% (Figure). Moreover, the drop in the headline is likely to be short-lived as this month’s rise in the energy price cap and a recovery in fuel prices may pull the headline rate back to around 2.3% in October and average a little higher for the whole of Q4. Regardless, the data backdrop is consistent with underlying inflation having fallen, especially when assessed in shorter-term dynamics . As such a CPI picture, now weaker than BoE thinking, should not prevent the much-vaunted Bank Rate cut at the looming November MPC meeting. But as for a possible further mover as soon as the December MPC meeting this is still a possibility rather than probability not least given apparent splits within the BoE hierarchy.

The July CPI was notable for the clear and larger-than-expected fall in services inflation, one driven by a fall in restaurant/hotel inflation, this often seen as a bellwether indicator of price persistence. The August data showed mixed signs on such a basis as the overall CPI headline rate stayed at 2.2%, this chiming with the consensus and two notches under BoE thinking. Indeed, services inflation rose back 0.4 ppt to 5.6%, up from a two-year low but still below the BoE projection and was almost solely driven by a swing in (very volatile) airfares without which services would have fallen below 5% - this also accounting for the rise in the core rate. Moreover, restaurant inflation hit a new cycle low amid generally softer price pressures in which eight (of 12) CPI components fell.

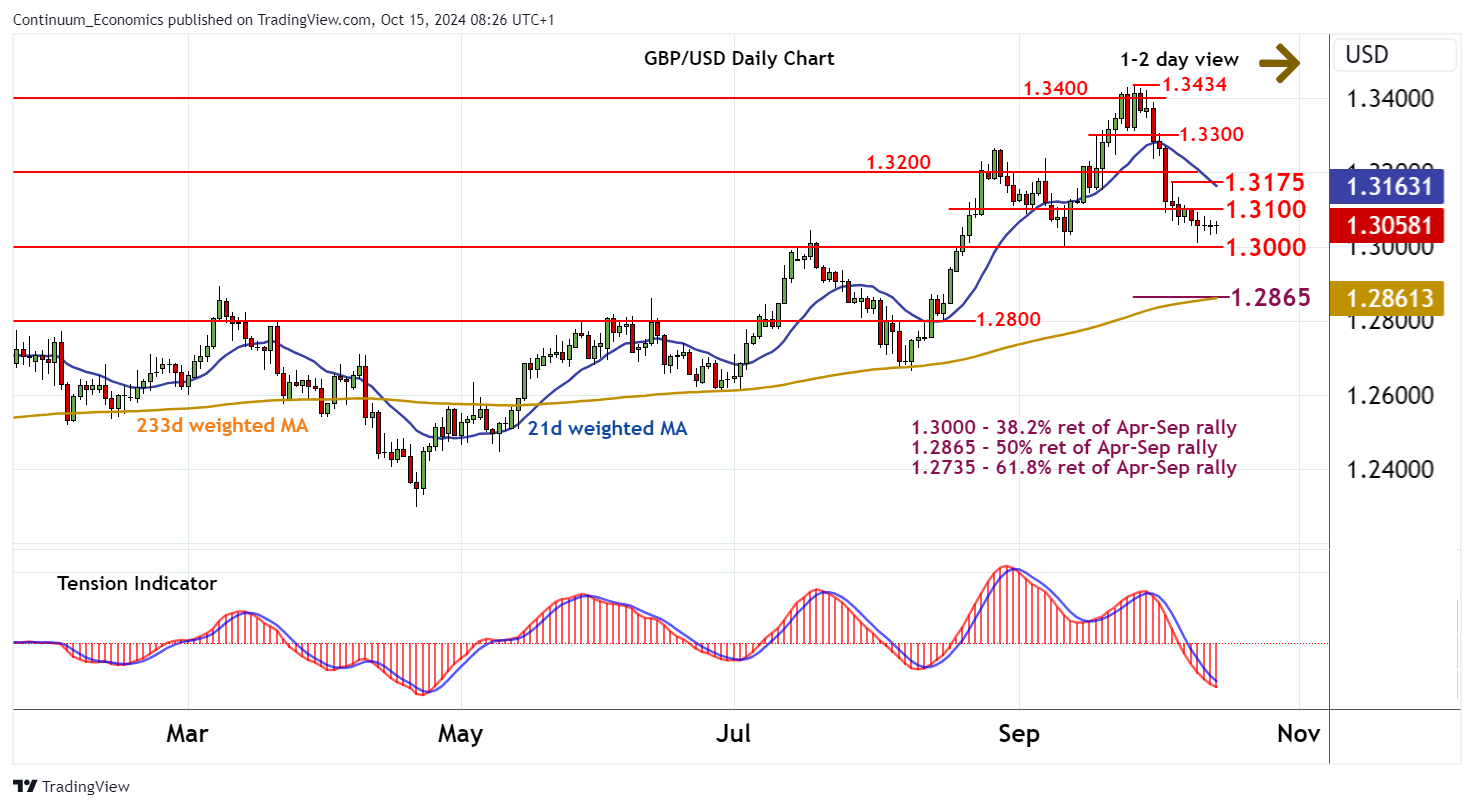

If UK CPI does come in lower than estimate, it may trigger a break below the recent low and the 1.3 figure. The Cable has been under pressure since late September but so far held by the support at 1.3. The lower CPI could trigger market participant's anticipation towards further rate cut changes, which could be accelerated by continuously solid USD and some technical selling.

On the chart, there is still little change as mixed/negative intraday studies keep near-term sentiment cautious and extend consolidation beneath congestion resistance at 1.3100. Oversold daily stochastics are flat and the negative daily Tension Indicator is flattening, suggesting further cautious trade into the coming sessions. However, weekly charts continue to fall, pointing to room for a later pullback. A break below strong support at 1.3000 will add weight to sentiment and extend September losses towards strong support at the 1.2865 Fibonacci retracement. Meanwhile, any immediate tests higher should remain capped beneath 1.3100.

The USD/JPY has retreated from the 150 figure after the first attempt. The political headwind from new PM Ishida seems to be calmed by now as he walk back from his previous comment. The inflationary dynamic also support further BoJ action, unless we see a significant moderation in National CPI this Friday that is unlikely. However, the slow pick up in consumption will remain a thorn by their side because it determines the height of trend inflation and could make the BoJ looks like they have made a policy error in the coming years. The pace of changes in price/wage setting behavior and the willingness of Japanese to consume at higher price will be critical. In a short to medium run, the JPY is likely to strengthen for the BoJ would most likely act before market participants anticipate.

On the chart, the consolidation below the 149.40 resistance has given way to break higher to extend gains from the September YTD low to reach the 150.00 figure. Pause here see prices unwinding the overbought intraday studies but further gains not ruled out. A later break will open up scope to the 150.75/150.90, 50% Fibonacci retracement and February high. Break here, if seen, will see potential to the 152.00 resistance. Meanwhile, support is at the 148.00 level which now underpin. Would take break here to turn focus lower to the 147.21 support then the 146.50/146.00 area.